Börsipäev 2. juuli

Kommentaari jätmiseks loo konto või logi sisse

-

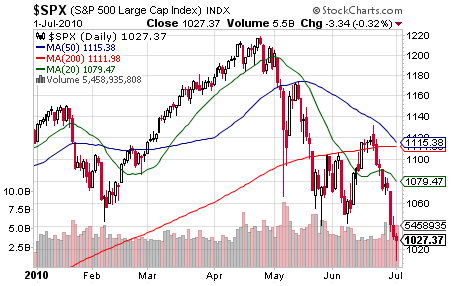

Eilne kauplemissessioon möödus turgudel taas võrdlemisi kesiselt – makronäitajad olid prognoositust halvemad. Töötuabirahale taotlejate koguarv ületas konsensuse ootusi ja veel lõpule viimata kinnisvaratehingute raport ehk „pending home sales“ viitas sellele, et maksusoodustuste efekt on kinnisvarasektorile olnud päris suur ning ka tulevatel kuudel võib oodata tagasihoidlikke tulemusi. Võlakirjad kallinesid, mis tingis 10-aastase ja 30-aastase võlakirja tulususe määrade languse 2009. aasta aprillikuu tasemele. NYSE’l oli langejate ja tõusjate vahekord 2/1.

Täna on aga makrouudiste koha pealt kuu üks tähtsamaid päevi. Kell 15:30 avaldatakse USA töötusmäär (konsensus 9.8%), töökohtade arv (va põllumajandussektor, konsensus -100,000), tunnipalga muutus (konsensus +0.1%) ja keskmise töönädala pikkus (konsensus 34.2). Kell 17:00 avaldatakse ka tööstustellimused (konsensus -0.6%).

Allikas: stockcharts.com

-

Eilses börsipäeva foorumis oli juttu Hiina majanduskasvust.

Täna hommikul tuli Goldman Sachs välja oma nägemusega – Hiina 2010. aasta SKP kasvuprognoosi langetati 11.4% pealt 10.1%le ehk sarnaselt teiste analüüsimajadega oodatakse "pehmet maandumist". Q2 ja Q3 q-o-q kasvuks nähakse ca 8%, mis on aga alla konsensuse prognooside. 2011. aasta SKP prognoos jäeti endise 10% peale.

Paar rida võõrkeelset teksti:

„The FCI, which uses mom M2 growth, has tightened by as much as 479 bp since the recent trough in February. Just as we revised up our 2009 GDP forecast sharply in March 2009 because of the dramatic FCI easing, the notable tightening in FCI in recent months led us to lower our short-term forecast.“

„We also revise down our CPI inflation forecasts to 2.4% for 2010 from 3.5% previously, and to 1.3% in 2011 down from 2.8% previously.“

-

Meeldetuletuseks, et USA turud on esmaspäeval (5. juulil) iseseisvuspäeva tõttu suletud.

-

Baltic Dry Index, mis näitab laevadega veetava kuivlasti (peamiselt kivisöe ja rauamaagi) tariife, langes juunis ca 40%, näidates globaalse tööstustegevuse aeglustumist. Tavaliselt tähendab BDI langus ka kukkuvaid hindu toorainete turul. Väga suurt rolli indeksi kujunemisel mängib Hiina nõudlus toorainete järele. Silmas tuleb aga pidada, et Hiina nõudluse langus ei tulene mitte ainult reaalse tööstustoodangu langusest. Nimelt täiendas Hiina aprillis riigi toorainevarusid, millel kindlasti oli oma mõju indeksi väärtusele. Üks lõik siia Marketoracle'i vahendusel:

Integrating the China factor into the BDI equation, we recall that the April peak in copper coincided with reports that Chinas surging demand may have reflected stockpiling than actual integration into the building cycle.

Hoolimata Hiina võimude otsuste poolt tingitud indeksi volatiilsusest tuleks investoritel BDI’l silma peal hoida, sest tariifide edasine langus võib negatiivselt mõjuda toorainehindadele.

-

Briefing.com vahendusel:

June Nonfarm Payrolls -125K vs -100K Briefing.com consensus, prior revised to 433K from 431K

June Unemployment Rate 9.5% vs 9.8% Briefing.com consensus, prior 9.7%

June Average Workweek 34.1 vs 34.2 Briefing.com consensus

June Private Payrolls 83K, prior 33K; lower than expected

June Hourly Earnings M/M -0.1% vs +0.1% Briefing.com consensus, prior revised to +0.2% from +0.3%

-

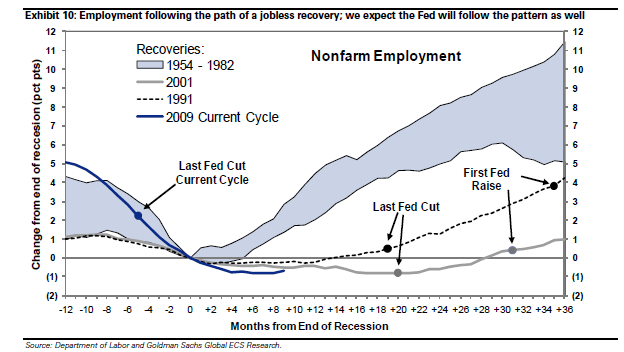

Ning nende numbrite põhjal tundub taaskord, et seekordne majanduslangusest taastumine ei erine viimastest - s.t näeme taas ühte jobless recovery'it:

-----

Futuurid, mis alguses tegid põrke, liiguvad tööjõuraporti peale nüüd viimase 24h põhjadesse.

-

Euroopa turud on pärast tööjõuraporti järgset kukkumist kosunud endisele tasemele ning USA futuurid indikeerivad avanemist nulli lähedal.

Euroopa turud:

Saksamaa DAX 0,55%

Pantsusmaa CAC 40 0,87%

Suurbritannia FTSE100 1,07%

Hispaania IBEX 35 1,83%

Rootsi OMX 30 0,98%

Venemaa MICEX 2,03%

Poola WIG 0,57%Aasia turud:

Jaapani Nikkei 225 0,13%

Hong Kongi Hang Seng -1,11%

Hiina Shanghai A (kodumaine) 0,38%

Hiina Shanghai B (välismaine) 0,78%

Lõuna-Korea Kosdaq -0,8%

Tai Set 50 0,59%

India Sensex 30 -0,28% -

Rev Shark: Trade the Trend

07/02/2010 7:00 AM"Never awake me when you have good news to announce, because with good news nothing presses; but when you have bad news, arouse me immediately, for then there is not an instant to be lost."

-- Napoleon Bonaparte

The million-dollar question this morning is to what degree has the market priced in a bad jobs report. The report is due out at 8:30 a.m. EDT, and it is expected to show a loss of about 150,000 jobs. With weekly unemployment claims and the ADP employment report coming in worse than expected, however, many market players are expecting worse.

The good news is that this market has undergone a significant correction over the past two weeks. If there is bad news out there, much of it has already been priced in, which makes the chances of a rally on a poor jobs report fairly good.

Once we are past the initial emotional response to the jobs news, trading becomes very tricky very fast. If we do have a relief rally on the news, we run into the first technical overhead resistance at around 1,050 of the S&P 500. If we can cut through that level, then the next area of chart congestion is around 1,067-1,070.

The No. 1 thing to keep in mind is that the market is in a downtrend. There is a good setup for an oversold bounce on the jobs news, but it would be a mistake to conclude that the worst is over and that the market is going to go straight back up. A significant number of trapped bulls have been riding this move down and would love to escape some positions if they can sell into strength and reduce their losses. Also, plenty of emboldened bears will be looking to aggressively remount shorts as we bounce into technical resistance. If you go through charts of individual stocks, you'll find a lot of stocks ready for dead-cat bounces, which will offer excellent short setups once they are not quite so oversold.

I believe the best way to approach this market is to require the bulls to prove themselves before you trust them. Many market players prefer to try to call the bottom, but my experience has been that it is far safer and more profitable to wait until there is some good evidence that the trend is changing. You can play oversold bounces and bear market spikes if that is your style, but just make sure you have the appropriate time frames and are using good money management to control risk.

The way to make money in the market is to trade in the direction of the trend. It can be more difficult than it sounds, especially when we have a constant chorus of voices telling us why conditions are about to shift. If you block the noise, stay open minded and aren't overly anticipatory, however, it can mean more for your investment returns than anything.

We'll see what is in the jobs news and then we'll go from there. Good luck and go get 'em.

-

Gapping down

In reaction to disappointing earnings/guidance: WIBC -15.0%.Select European drug names trading lower: SNY -2.3% (preparing a major acquisition in the U.S., potentially worth $20 bln), AZN -1.7%, GSK -0.5%.

Other news: MIPI -13.4% (receives fourth extension of waiver agreement with bond holders), LNCR -9.9% (trading lower; weakness attributed to reimbursement for oxygen equipment), VZ -4.9% (trading post spinoff), SNN -4.5% (still checking for anything specific; Hearing weakness attributed to CMS Round 1 Competitive Bidding rates for Durable Medical Equipment products), HLX -4.2% (announced the engagement of advisors to evaluate strategic alternatives for a potential divestment of its oil and gas business; co expects significant downward revision in proved reserves), RIG -2.3% (still checking), HITK -1.7% (temporarily and voluntarily suspends sales of certain products; co received a warning letter from the FDA).

Analyst comments: IRET -1.1% (downgraded to Sell from Neutral at Janney Montgomery Scott).

Gapping up

In reaction to strong earnings/guidance: DMAN +3.0%, FLOW +2.2% (light volume).Select European financial related names ticking higher: AIB +5.7%, LYG +3.1%, BCS +2.9%.

Select metals/mining stocks trading higher boosted by news that the Australian govt dropped the "super profits" tax on miners: BBL +2.8%, RTP +1.8%, VALE +1.6%, BHP +1.5%, GOLD +1.4%, KGC +1.4%, GLD +1.3%, GDX +1.2%, FCX +1.1%, AU +1.1%, EGO +1.0%, AUY +0.9%.

Other news: ONP +4.8% (rebounding from this week's 40% drop), NOK +2.2% (Mobile TeleSystems secured a credit facility to buy equipment and services from Nokia Siemens Networks), BP +2.1% (modestly higher in the pre-mkt on reports that the first intercept well is progressing ahead of schedule), QGEN +1.7% (reports that the co said it expects 10% sales growth annually), MEND +1.6% (will replace CKE Restaurants in the S&P SmallCap 600 index), .

Analyst comments: ARNA +3.9% (upgraded to Outperform from Market Perform at Leerink Swann).

-

Võiks öelda et majanduslangusest taastumine oli juba ära. Ja nüüd selgub et valitsustel on rahadega probleeme mis viib uuele majanduslangusele. Varsti oleme eelmiste põhjade juures tagasi.

Kui nüüd kevadel ja suvel töökohtade arv eriti ei kasva ja tarbimine samuti siis vaevalt et seda juhtub sügisel ja talvel.

Puhtalt minu arvamus. -

Kui nüüd veel juuli keskel lumi maha tuleb, siis kukub S&P500 kindlasti läbi 2009 alguse põhja (666).

-

teoreetiliselt võimalik, praktikas ei kasutata

-

Morgan Stanley FX Pulse analüütikute nägemus valuutaturust (horisont 1 nädal).

USD – Bullish. USD to Garner Support from Market Uncertainty. With global growth concerns deepening amid slowing activity data, we expect USD to gain as investors seek out the relatively safety and liquidity of USTreasuries. Though much of the concern about a global slowdown stems from weaker US data, our sense is that the US recovery will prove moredurable than what markets are expecting. Nonetheless, the USD should continue to perform well under both environments.

We hold long USD positions against EUR, JPY, and GBP and ZAR.

EUR – Bearish. Prolonged Negative Sentiment. Market jitters around the expirations of the ECB LTRO and new tenders led to choppier price action than usual. Our sense is that the negativesentiment will prove longer-lasting, given that the persistent uncertainty around the fiscal situation. As EUR is viewed as a less attractive reservecurrency, we should see more sovereigns diversify away from EUR, as this week’s new IMF COFER data suggest.

We remain short EUR against USD. We would use rallies in EUR/USD as opportunities to add to shorts.

-

Makrouudiseid briefing.com vahendusel:

May Factory Orders -1.4% vs -0.6% Briefing.com consensus, prior revised to +1.0% from +1.2%

-

Peab nentima, et 2008.a. näitas Baltik Dry väga hästi majanduse jahtumist. Tegemist on ka väga loogilise early warning indikaatoriga. Veetakse toorainet, mis on kogu tootmisprotsessi algus. Kui tooraine vedu väheneb, siis vabaneb rohkem laevu ja veohindu lüüakse alla. Samas viimasel ajal ei ole see indikaator väga hästi käitunud. Mõtlesin veidi selle peale ja pakun välja teooria: Paljud laevad telliti buumi tipus. Nende tellimuste täitmine võttis aega mitu aastat. Ja nüüdseks on uued laevad valmis saanud ja sisenenud already crowded turule. Mis põhjustab veohindade langust.

USAs rongivedude hindadel küll midagi viga pole

Buffetti raudtee ost tuli küll parimal võimalikul hetkel. -

Ilmselt siin ühest vastust/põhjust ei ole, aga kui ajas tagasi vaadata, siis paljud shipping firmad tellisid buumi ajal uusi laevu, mis kriisi ajal aga osaliselt canceldati. Dry Shipping tegi seda mitme laevaga, seega osa nõudlusest kustutati.

BDI suur langus ja teatud tasemetelt läbi murdmine näitab selgelt majanduse ja transpordisektori jahtumise märke. Hiina enam niivõrd palju tooret ei vaja, kuhjati ju end madalatest hindadest täis, nüüd mõneks ajaks vaikus. -

Hiina eksport kasvas mais 40%, millestki peab neid asju tootma (Hiina on suurim maavarade ostja maailmaturul). Siin ongi disconnect - Hiinas ostab suures koguses tooret ja ekspordib palju, kuid Baltic Dry langeb. How come? Mina pakun ikka, et on liiga palju laevu.

-

Uute laevade kohta siin üks väike artikkel, mis pärineb 25. märtsist. Nimelt kasvas perioodil 2004-2009 kuivlastilaevade maht 6.6% p.a. ning laevade arv 1.9% p.a. ehk telliti suuremaid laevu. Üks huvitav lause, mis silma jäi – 2010. aastal on laevade arv hüppeliselt kasvamas, ületades prognoositud toorainete kaubandusmahtude kasvu:

Deliveries to the dry bulk fleet are expected to grow by 21 percent in 2010, from 47 million dwt last year to 57 million dwt. As a result, bulk fleet capacity is calculated to grow by 7.5 percent this year, by 10 percent next year and by the same amount during 2012. This is higher than the forecast increase for global commodity trade volumes.

-

STX-i Soome äsjavallandatud juht kommenteeris samuti, et laevaehitusäri on praegu väga vaikne.

-

Tõenäoliselt on BDI languse taga nii üht kui teist. Ühest küljest on tõesti suurenenud pakkumine laevade osas. Samas metallide ja metalliaktsiate langenud hinnad näitavad, et ka nõudlus on langenud.

-

Hiina eksport kasvas juunis 43,9%

http://www.ap3.ee/?PublicationId=aad338a9-ed31-4123-b85b-727c3fdf5f57 -

Samal ajal langes Baltic Dry 4050 pealt 2350 peale.

-

A Reminder Of Why The Baltic Dry Index Is A Useless Leading Economic Indicator

http://www.businessinsider.com/a-reminder-of-why-the-baltic-dry-index-is-a-useless-leading-economic-indicator-2010-7