Börsipäev 26. juuli

Kommentaari jätmiseks loo konto või logi sisse

-

Kui USA-s kulus pankade stresstesti plaani avalikustamisest kuni lõpptulemuste teatavaks tegemiseni vaid mõni kuu, siis Euroopas mõlgutati mõtteid sel teemal tegelikult juba rohkem kui aasta tagasi. Sestap oleks arvanud, et pikemaajalisem ettevalmistuse pool oleks toonud kredibiilsema tulemuse, ent nii nagu FED oskas tulemusi veidi soodsamas valguses näidata, tegid seda ka ECB ja CEBS Euroopa pangandussektori puhul. Wolfgang Münchau on FT-s kirjutanud päris hea artikli, kus ta toob välja testi kolm põhilist fundamentaalset probleemi. A test cynically calibrated to fix the result

-

Tallinna börsil on suurimat aktiivsust näidanud Tallink, kus esimese tunniga sõideti 100k valdavalt EVList koosnevast müügipakist (0.59) üle ning kauplemine jätkub 0.60€ peal.

-

"One of those is KfW, the German state-owned institution that is legally not a bank but carries out bank-like functions – such as accumulating lots of toxic assets."

:D -

Ka euri liikumisest on näha, et esimene reaktsioon reede avalikustatud tulemustele oli siiski negatiivne, vaatamata sellele oodatust vähem pankasid põrus ning kapitali puudujääk kõikide osalejate peale arvatust kordades väiksemaks osutus. Praeguseks on EUR tagasi 1,29 juures ning meeleolu Euroopa turgudel ja USA eelturul suhteliselt neutraalne. Kuna taetud skepsist see stressitest osades siiski tekitas, otsitakse tõnäoliselt järgmiseid indikaatoreid, mis aitasid sentimenti edasi kujundada. Euroopas täna olulisi majandusuudiseid oodata ei ole, USA-s koondub tähelepanu juunikuu uute majade müüginumbrile kell 17.00

-

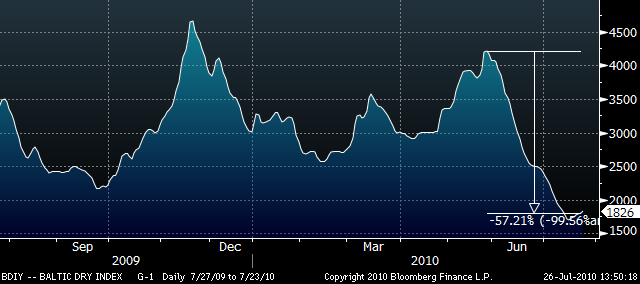

Baltic Dry indeks suutis eelmise nädala lõpetada plussis esimest korda pea kahe kuu jooksul tänu mitmete põllumajandustoodete suurenenud transpordile kuumalaine all kannatavasse Euroopasse. Ühtlasi on viimastel nädalatel toimunud ka mõningane taastumine Hiina terase- ja rauamaagihindades, mis võiks anda signaali paranevast nõudlusest.

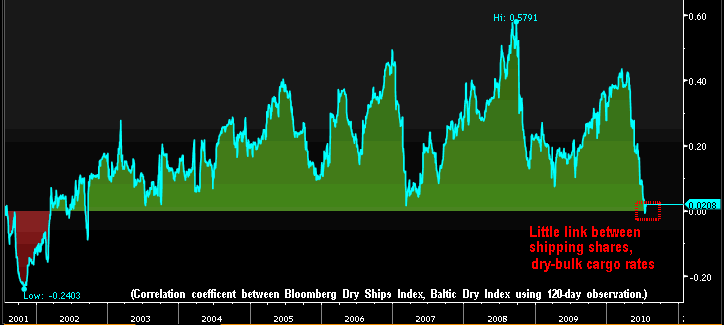

Eelmisel nädalal jäi silma üks huvitav graafik, mis kajastab BDI ja erinevate laevatamisega tegelevate ettevõtete aktsiate (neid esindab Bloomberg Dry Ships Index) vahelist korrelatsiooni. Kui 2008.a ulatus 120 päeva korrelatsioonikoefitsient pea 0,6ni, siis tänaseks on need kaks gruppi üksteisest lahti haakinud ning vaatamata BDI pea 60% langusele mai lõpust, mil Hiina valitsus hakkas jõulisemalt kinnisvaraspekulatsooni vähendama, on Bloomberg Dry Ships Index tõusnud veidi üle 4%. Põhjuseks on investorite lootus, et aasta teises pooles hakkavad laevatamise tasud taas tõusma ning igasugune võimalik leevendus Hiina kinnisvarapoliitikas oleks täiendavaks katalüsaatoriks nõudlusele.

Kui vaadata, millest täpsemalt Bloombergi indeks koosneb, näeme et 12 ettevõtet seal on ning tugevalt mõjutatud teatud üksikutest liikmetest nagu näiteks 1), 3) ja 4), mille osakaalud kokku moodustavad üle 51%.

-

Fedexi uus Q1 guidance'i vahemik algab eelmise prognoosi ülemisest otsast, mis on aktsiat eelturul ca 5% plussi upitanud ning miinuses ES futuuri tagasi nulli tõstnud.

FedEx raises Q1, FY11 EPS guidance (78.96)Co raises guidance for Q1 (Aug), sees EPS of $1.05-1.25 vs. $1.01 Thomson Reuters consensus, up from $0.85-1.05 previously. Co raises guidance for FY11 (May), sees EPS of $4.60-5.20 vs. $4.98 Thomson Reuters consensus, up from $4.60-5.20 previously. "Our revenue and earnings growth are exceeding original expectations, primarily due to better-than-anticipated growth in FedEx Express and FedEx Ground volumes. Our package volume growth rates in our first quarter are continuing at a pace similar to our fourth quarter. Of particular benefit to our earnings is the continued strong demand for our higher-margin FedEx International Priority package and freight services, with IP package volumes expected to grow more than 20% again this quarter."

-

Briefingus väike viga....FDX-i eelmine FY EPS prognoos oli 4,40-5,00 USD

-

USA indeksfutuurid vahetult enne turgude avanemist kergelt plussis. ES +0.05% ja NQ +0.03%.

Euroopa turud:

Saksamaa DAX -0.38%

Pantsusmaa CAC 40 -0.30%

Suurbritannia FTSE100 -0.10%

Hispaania IBEX 35 -0.27%

Rootsi OMX 30 -0.20%

Venemaa MICEX +0.37%

Poola WIG +0.34%Aasia turud:

Jaapani Nikkei 225 +0.77%

Hong Kongi Hang Seng +0.12%

Hiina Shanghai A (kodumaine) +0.65%

Hiina Shanghai B (välismaine) +0.80%

Lõuna-Korea Kosdaq +0.92%

Tai Set 50 +1.11%

India Sensex 30 -0.61% -

Are More Surprises in Store?

By Rev Shark

RealMoney.com Contributor

07/26/2010 8:08 AM

"I am a man of fixed and unbending principles, the first of which is to be flexible at all times."-- Everett Dirksen

The market surprised a lot of people last week with a sudden gap up on Thursday and some strong follow-through on Friday. On Wednesday, the mood was particularly negative after a downbeat appearance before Congress by Ben Bernanke, but on Thursday, some stronger-than-expected European economic news hit and caused a sizable gap up, and the chase began. Benign results from the European bank stress test on Friday kept it going.The main reason for the strength was that sentiment has been particularly negative lately, with far more skepticism than usual, so market players weren't positioned, and when we had a sudden reversal on Thursday, there was a mad scramble to cover shorts and to find some long exposure. When we didn't reverse early on Friday, the hunt for long exposure continued, and we ended up going out at the highs.

The net result of this action was that the S&P 500 managed to close above key technical resistance at 1,100 and the Nasdaq made it through its 200-day simple moving average at 2,259.

So now what? The big picture now looks much better than it did on Wednesday, when many folks were ready to conclude that the market was dead and that a fast trip to the July lows was on the horizon.

The bulls now have a slight advantage on which they can build. The trend is turning up, and if the S&P 500 and Nasdaq can hold the key technical levels mentioned above for a few days, it bodes well. A quick failure would again surprise many, however, and some of the newly minted bulls who are struggling to deal with last week's surprise would likely hit the sell button quickly.

I have to admit that I was one of those market players that was caught by surprise by the sudden turn at the end of the week, but that is just the nature of the trading game. It happens all the time, and if you actively trade the market, you will be caught by surprise quite often. The market is extremely adept at making sure you stay humble and respect its power.

The perennial challenge of the market is to have a viewpoint and approach but to be flexible enough to change your mind should it prove wrong. While you don't want to be dogmatic, if the market is moving against you, you also don't want to be so devoid of conviction that you change your position too quickly or easily.

Perma-bulls and perma-bears are the best example of dogmatic investors who stick with a viewpoint no matter what the market is actually doing. It's nice that you never have to question your viewpoint, but it sure can be costly when the market is moving against you.

At the other end of the spectrum are the ultra-short-term traders who change their viewpoint with every tick in the market. They are unlikely to be on the wrong side of the market for very long, but they are also unlikely to be well-positioned as the market constantly shakes them out with spikes, dips and reversals.

We are at the point right now where we need to seriously contemplate whether the action at the end of last week is sufficient to have us embrace a more bullish view. It was strong action and we breached some key resistance, but is it sufficient to think that we have clear sailing to the upside from here?

My thesis, which I discussed several times last week, is that I'm expecting the S&P 500 to break the 1,100 level but to not make it through the next level of resistance at 1,113 without considerable effort. In fact, I believe we have a good chance of the breakout at 1,100 failing.

Given the strength of the action last week, I'm not feeling as confident about my thesis, but I'm not going to give up on it quite yet. I want to see what the bulls can do as we kick off the new week. I'm ready to adjust should last week's level of strength continue, but for now, I'm maintaining a fairly high level of skepticism.

Overseas markets were mixed, and we are starting off about flat. There are plenty of earnings reports to come this week, but most of the big market movers have already reported, so economic news will likely be the key catalysts.

-

Briefing.com vahendusel:

Ülespoole avanevad:

In reaction to strong earnings/guidance: CSR +5.3%, EEP +2.6% (light volume).

Other news: ONXX +14.4% (announces positive top-line Carfilzomib data from Phase 2b study), GAP +3.1% (modestly rebounding from Friday's drop following earnings), ARNA +6.6% (still checking), AONE +4.0% (Hearing early strength attributed to analyst upgrade), ONP +4.0% (continued momemtun from Friday's 15%+ jump), GENZ +4.0% (ticking higher in early trade following increased speculation that the company is a takeover target), WFR +3.9% (Hearing early strength attributed to analyst upgrade), TEVA +3.3% (rebounding from Friday's 4 point drop), SOMX +3.3% (still checking), BP +2.6% (confirms passing of Tropical Storm Bonnie weather system; reports out that the co will replace CEO Hayward in the next 24 hrs), MLNX +2.3% (continuing to rebound from Thursday's 6 point drop), BX +2.2% (Hearing early strength attributed to analyst upgrade).

Analyst comments: PTEN +7.5% (upgraded to Buy from Hold at Jefferies ), SNY +0.9% (upgraded to Buy from Hold at Jefferies), T +0.7% (upgraded to Buy from Hold at Deutsche Bank).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: NED -17.3% (thinly traded, light volume), BWP -3.1% (light volume).

Select financial related names showing weakness: AIB -3.1%, DB -2.6%, STD -2.2%, IRE -2.0%, CS -1.0%.

Other news: CGA -3.9% (filed for a $200 mln mixed shelf offering), QGEN -1.9% (still checking for anything specific).

Analyst comments: AMMD -3.7% (downgraded to Market Perform from Outperform at Wells Fargo), CHS -2.3% (added to Conviction Sell List at Goldman), LPS -1.6% (downgraded to Perform from Outperform at Oppenheimer), STM -1.4% (downgraded to Neutral from Buy at Natixis Bleichoeder), EL -1.3% (downgraded to Underperform from Perform at Oppenheimer).

-

makro oodatust veidi parem, turg paneb 20 000 maja peale päris jõudsalt ülespoole

June New Home Sales 330K vs 310K Briefing.com consensus; M/M +23.6%