Börsipäev 29. juuli

Kommentaari jätmiseks loo konto või logi sisse

-

USA börsipäeva dikteeris eile teises pooles negatiivsem meeleolu, mida tekitas FED-i beež raamat. Kuigi viimase kohaselt majandusaktiivsuse kasv jätkus, täheldati läinud kahe kuu jooksul mitmetes valdkondades (näiteks jaemüük, kinnisvara ja ehitus) kas tagasihoidlikku paranemist või koguni nõrkust. Föderaalreservi sõnumite peale lõpetas turg nädala jooksul esimest korda kerges miinuses. Aasia indeksid kauplevad samuti valdavalt madalamal, olles päeva põhjadest pisut taastunud. USA futuurid liiguvad hetkel 0.3% kõrgemal ja Euroopa omad indikeerivad avanemist 0.2% kuni 0.4% plussis.

Euroopas on makromajanduslikest sõnumitest tähelepanu all Saksaama juulikuu töötuse näitajad (kl 10.55) ja eurotsooni mitmed usaldusindeksid (kell 12.00). USA-s seevastu jälgitakse möödunud nädala esmaskordselt töötuabiraha taotlenute arvu (konsensus ootab samaks jäämist 464 000-le) ning jooksvat taotlejate arvu (konsensus prognoosib kasvu 4 478 000 pealt 4 550 000 peale.

-

EUR on vimased kolm päeva 1,3050 piiriga flirtinud ning jäänud ebaõnnestunud läbimurdmise tõttu suhteliselt kitsasse koridori kauplema. Tänane makro võiks olla üheks võimalikuks katalüsaatoriks, mis aitaks piiri ületada ning sellisel juhul juba järgmiste tasemeteni upside'i pakuks.

-

Saksamaa töötuse näitajad tulid täpselt ootustesse. Juulikuuga vähenes töötute armee 20 000 inimese võrra ja tööpuuduse määraks registreeriti 7.6%, mis on madalaim alates 2008.a novembrist.

-

Saksamaa ootuspärased tööturu tulemused viisid euro dollari vastu rallima: EUR/USD tegi uue päevasisese ja ühtlasi paari kuu tipu 1,3077 juures.

Dollar on seevastu korralikus languses: dollari indeks on kukkunud täna 0,55% 81,80 tasemele, kus ta oli viimati aprilli lõpus. -

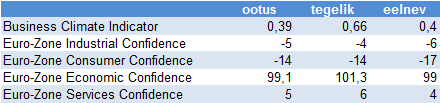

Teen siia väikese kokkuvõtte ka eurotsooni juulikuu usaldusindeksitest, mille tegelikud näidud osutusid peaaegu kõik ootustest paremaks. Euroopa indeksitele see erilist mõju ei avaldanud ning tänast börsipäeva jätkatakse ca 0.5%lises plussis, USA futuurid liiguvad aga nüüdseks juba 0.4% kuni 0.5% kõrgemal.

-

Hiljuti USAs vastu võetud tervet finantssüsteemi põhjalikult reformiv seadus pidi Obama ja rahvaesindajate sõnul suurendama terve süsteemi läbipaistvust. Ilmselt pidasid ametnikud läbipaistvuse all hoopis midagi muud silmas, sest ülimahukasse seadusesse on sisse pistetud säte, millega antakse USA finantsinspektsioonile (SEC) immuunsus avalikusse poolt tehtud infopäringutele.

Vastavalt Freedom of Information Act'ile on kodanikel õigus saada ligipääs valitsuse poolt kontrollitavale ja hallatavale informatsioonile, mille alla kuuluvad ka kõik regulatoorsed riiklikud agentuurid.

SEC väidab nüüd, et uus vastuvõetud seadus vabastab nad infopäringutele reageerimise kohustusest - vahend, millega kodanikud ja meedia saavad heita valgust võimukoridoride tegemistesse.

Under a little-noticed provision of the recently passed financial-reform legislation, the Securities and Exchange Commission no longer has to comply with virtually all requests for information releases from the public, including those filed under the Freedom of Information Act.

The law, signed last week by President Obama, exempts the SEC from disclosing records or information derived from “surveillance, risk assessments, or other regulatory and oversight activities.” Given that the SEC is a regulatory body, the provision covers almost every action by the agency, lawyers say. Congress and federal agencies can request information, but the public cannot.

That argument comes despite the President saying that one of the cornerstones of the sweeping new legislation was more transparent financial markets. Indeed, in touting the new law, Obama specifically said it would “increase transparency in financial dealings.”

The SEC cited the new law Tuesday in a FOIA action brought by FOX Business Network. Steven Mintz, founding partner of law firm Mintz & Gold LLC in New York, lamented what he described as “the backroom deal that was cut between Congress and the SEC to keep the SEC’s failures secret. The only losers here are the American public.”

-

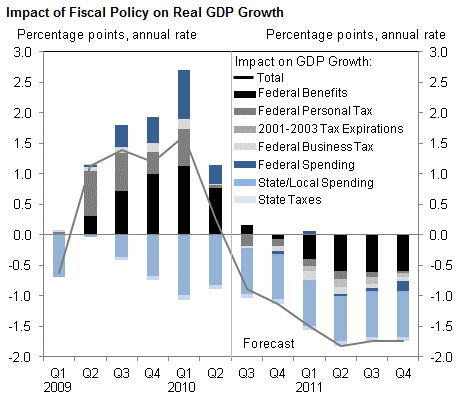

Goldman Sachs avaldas eile õhtul taas arvamust USA fiskaalpoliitika kohta – analüüsimaja hinnangul langeb fiskaalpoliitika osatähtsus ameeriklaste majanduskasvus 2009. aasta lõpu ja 2010. aasta alguses nähtud 1.3 protsendipunkti pealt 2011. aastaks -1.7 protsendipunktile.

Allpool näha olev graafik on aga joonistatud mõne oletusega: 1) kongress ei vii pikendatud töötuabiraha stiimulit veel kaugemasse tulevikku (mäletatavasti lükati hiljuti nende aegumine juba mitmendat korda edasi 2010. aasta novembrisse), 2) föderaalvalitsus ei mõtle peale ARRA välja uut programmi osariikide eelarvete täitmiseks.

Ei ole vist vaja mainida, et pilt on võrdlemisi kole.

-

Esmaskordsete taotlejate number oli ootustest madalam, ent eelnevat näitajat revideeriti jällegi kõrgemale. Jooksev number samuti arvatust kõrgem, mille peale eelturg suuremat liikumist ei tee ning S&P 500 futuur jätkab 0.5%lises plussis kauplemist.

Initial Claims 457K vs 464K Briefing.com consensus, prior revised to 468K from 464K

Continuing Claims rises to 4.565 mln from 4.484 mln

-

USA indeksfutuurid enne avanemist plussis - NQ +0.60% ja ES +0.70%

Euroopa turud:

Saksamaa DAX +0.66%

Pantsusmaa CAC 40 +0.58%

Suurbritannia FTSE100 +0.72%

Hispaania IBEX 35 +0.66%

Rootsi OMX 30 +0.61%

Venemaa MICEX +1.61%

Poola WIG +0.37%Aasia turud:

Jaapani Nikkei 225 -0.59%

Hong Kongi Hang Seng +0.01%

Hiina Shanghai A (kodumaine) +0.55%

Hiina Shanghai B (välismaine) +0.32%

Lõuna-Korea Kosdaq -0.86%

Tai Set 50 0.00%

India Sensex 30 +0.19% -

The Bulls Look Ready to Run

By Rev Shark

RealMoney.com Contributor

07/29/2010 7:16 AM

The trouble with the future is that is usually arrives before we're ready for it.-- Arnold H. Glasgow

After two days of flat to slightly negative action, the market is rested and looking to spring back to life this morning. Overseas markets are mostly positive on some good earnings news, but the main positive is a comment from a top analyst at Moody's, that European sovereign credit risk, as measured by swaps, is declining.

The market mood was mixed yesterday, as both the durable goods report and the beige book held few positives, but the bears were never really able to dig their claws into the market. We had relative weakness in small caps and the Nasdaq, but volume was quite light, and the S&P 500 and the DJIA held up fairly well. There wasn't any major panic and, overall, it looked like nothing more than a second day of healthy consolidation after a good run.

With some good earnings reports and some upbeat sentiment out of Europe, we are set this morning for an attempt at another leg up. We have the weekly unemployment numbers coming up, but it is the end of the month, and the bulls have the winds of positive seasonality at their backs.

Technically, the S&P 500 is back slightly under the 200-day simple moving average, at 1114, which remains a key level, but the June highs around 1131 are the next major hurdle for the bulls. At that point, we complete an inverse head-and-shoulders pattern that will likely garner some attention. If nothing else, it puts a bottoming pattern in place and provides a foundation the bulls can build on.

One of the most interesting things about the market lately is the rather peculiar state of sentiment. The sentiment polls have shown an unusually high level of bearishness, but the recent selling pressure was quite mild and seemed to reflect a rather high level of complacency.

The contrarians will tell us that the high level of bearishness in the sentiment polls means that a lot of market players have already sold and are on the sidelines. That creates upside pressure when they have to rush to add back long exposure when the market starts to run. The move last week definitely had the feel of market players being out of position, and I wouldn't be surprised to see that occur once again as we wind down the month.

We'll see what the weekly unemployment claims bring, but the bulls are looking ready to run a bit. With positive seasonality helping, quite a few good earnings reports, upbeat overseas action and a lot of folks poorly positioned for more upside, I don't expect the bears to put up too much of a fight.

-

Briefing.com vahendusel:

Ülespoole avanevad:

In reaction to strong earnings/guidance: NEWP +17.5%, IRBT +13.4%, SKX +10.8%, WIRE +9.4%, ITRI +8.8%, QLTY +8.2% (light volume), LOGI +8.0%, TER +7.7%, ENTR +7.3% (also upgraded to Buy at The Benchmark Company), CTXS +6.9% (also upgraded to Buy from Hold at Deutsche Bank, upgraded to Outperform at Robert W. Baird, upgraded to Neutral from Underperform at Cowen), IMAX +6.8% (light volume), OII +6.6%, CML +6.4% (also upgraded to Hold from Sell at Canaccord), TEF +5.2%, BT +4.3%, CLRT +4.0%, DRYS +2.4%, NUS +2.4% (light volume), GT +2.3%, MOT +2.2%, GMCR +2.2%, CTHR +2.1% (light volume), AZN +1.9% (also the FDA Advisory Committee recommends US FDA approval of Brilinta (Ticagrelor) for acute coronary syndromes), MPWR +1.8% (also upgraded to Strong Buy from Buy at Needham), XOM +0.7%.

M&A news: HTZ +1.0% (ticking higher after Avis Budget submits bid for Dollar Thrifty Automotive Group of $46.50 per share).

Select financial related names showing strength: ING +3.8%, UBS +3.0%, CS +2.6%, IRE +2.5%, DB +2.3%, BCS +1.8%, HBC +1.5%.

Select metals/mining stocks trading higher: RTP +2.1%, BBL +1.9%, BHP +1.8%, GOLD +1.2%, ACH +0.7%.

Select oil/gas related names showing strength: SDRL +2.2% (ticking higher), LLEN +2.2%, TOT +2.0%, CHK +1.3%, RIG +1.0%, BP +0.9%.

Other news: VCBI +17.2% (announces withdrawal of common stock offering ), ATHX +12.3% (announces positive results from Phase I study of Multistem in heart attack patients), CLNE +5.8%, FSYS +4.6% and WPRT +4.3% (Cramer makes positive comments on MadMoney), GENZ +3.4% (Genzyme trades to $70.65 in extended trading after WSJ reports on its website that Sanofi is "increasingly likely" to make a formal takeover bid to GENZ's board), SNN +2.2% (still checking), DNDN +1.8% (announces Provenge demonstrated a statistically significant improvement in overall survival compared to control in men with asymptomatic or minimally symptomatic metastatic castration resistant prostate cancer).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: VPRT -27.4%(also downgraded to Hold from Buy at Citigroup, downgraded to Mkt Perform at Barrington Research, downgraded to Neutral from Buy at Janney Montgomery Scott), CVD -14.7%, CTV -11.4%, PMI -10.2%, ARRS -9.5%, BG -9.2%, NENG -9.0%, GSIC -8.1%, SYMC -7.8%(also downgraded by multiple analysts), LOGM -7.7%, AKAM -7.1%, CRI -6.2%, NVDA -6.2%, GMR -5.9%, NETL -5.5%, LSI -5.3%, CNQR -5.0%, ASIA -4.4%, CL -4.0%, K -3.8%, DRIV -3.5%, ESRX -3.4%, NLY -3.1%, FLS -2.9%, ANH -2.8%(also downgraded to Neutral from Buy at Sterne Agee), CMO -2.3%(also downgraded to Hold from Buy at Deutsche Bank), PSSI -2.2%(light volume), CLF -2.1%, STO -1.3%.

Other news: DSTI -13.2%(discloses several investors entered into Purchase Agreements), RDN -3.3% (ticking lower following PMI results).

Analyst cldomments: AMD -1.1%(downgraded to Market Perform from Outperform at FBR Capital).

-

Millal IMAXI II kvartali tulemustele LHV PRO alla analüüs tuleb?

-

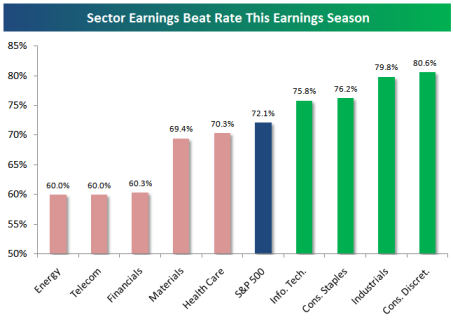

Bespoke'ilt üks hea graafik Q2 tulemuste hooajast.

-

lauri61, üritame järgmisel nädalal Imaxi analüüsi valmis saada

-

Mis kell peaks GDP tulema?

-

JP76, USA GDP tuleb välja homme kell 15.30