Börsipäev 10. august

Kommentaari jätmiseks loo konto või logi sisse

-

Täna kell 21.15 teatab Föderaalreserv oma intressimääraotsuse ning turuoosalised saavad lõpuks ometi vastuse küsimusele, kas "kvantitatiivne lõdvendamine vol2" ehk QE2 on tulemas või mitte. Seega kuni 21.15ni võiks oodata võrdlemisi loidu kauplemist ning pärast seda peaks turgudele korralik elu jälle sisse tulema. Kell 15.30 tuleb veel ka 2. kvartali tootlikkuse muutuse näitaja (ootus ca +0.1%), kuid see on vaid eelmäng õhtuse Fedi raporti ees.

Energiasektori guru Matthew Simmons, kelle mõtteid oleme ka LHV foorumites ja finantsportaalis vahendanud, sai oma kodus pühapäeval infarkti ning suri ootamatult. Kuigi tema nägemused energiasektori trendide osas olid väga pikaajalised, siis oli tegu finantsringkondades paljujälgitud mehega. -

Turgudel on hetkel valitsemas negatiivsed meeleolud. Saksamaa indeks DAX on langenud juba pisut üle 1% ning USA indeksite futuurid on eelturul praeguseks hetkeks kukkunud 0.6%-0.7%.

-

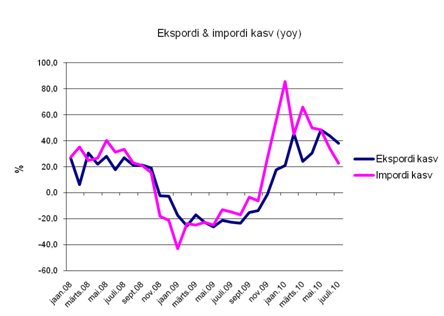

Täna avaldatud Hiina impordi kasvu aeglustumine viitab taas sealse kasvumootori aeglustumisele:

-

Nii m6nigi 45 USD pealt naftat armastama hakanud investor on SImmonsile suure osa oma varandusest v6lgu....

-

USA 10-aastase võlakirja tulususmäär on tänaseks päevaks langenud juba 2.8% peale. Nii madalal olid need viimati 2009. aasta märtsis. Madalad võlakirja tulususmäärad peaksid meelitama raha võlakirjainvesteeringute tegemise asemel aktsiaturgudele ning osa sellest rahast on sinna viimasel ajal Q2 korraliku tulemuste toel ka liikunud, kuid investorid suhtuvad aktsiaturgu tervikuna jätkuvalt skeptiliselt. Võlakirjade tulususmäärade langus viitab oodatust aeglasemale majanduskasvule ning pole siis ka ime, et Fedilt oodatakse vihjeid QE vol 2 kohta.

Aga mida on siis investorid rahaga teinud, kui aktsiaturgudele seda keerulisema eesootava makropildi pärast eriti panna ei ole juletud/tahetud ning võlakirjadesse raha parkides oleks oodatav aastane tulusus järgmise 10 aasta jooksul võrdlemisi nutune? Parima alternatiivina on seni nähtud suuri ja konservatiivse ärimudeliga ning stabiilse rahavooga suurt dividenditootlust pakkuvaid ettevõtteid. Siinkohal võib vaadata tubakasektori ettevõtteid nagu Altria (MO) või Reynolds (RAI), mis on tõusnud mitme aasta tippudele ja ammuilma läbinud aprilli tasemed, mil aktsiaturud tervikuna hakkasid alla tulema ja millest S&P500 on praegu veel ca 7% madalamal. Nii MO kui RAI pakuvad ca 6.3%list dividenditootlust (ja seda hoolimata sellest, et viimase aastaga on mõlemad aktsiad tõusnud ca 35%-40%!), mida on üle 2 korra rohkem võrreldes 10-aastase võlakirja tulususega. Samuti on tõusnud uute aasta tippude lähistele ka kommunaalteenuseid pakkuvad ettevõtteid, mida on hea jälgida sektorit koondava XLU kaudu. Lisaks võib siia nimekirja panna veel telekomid, mis on samuti viimasel ajal tuule tiibadesse saanud. Ehk stabiilne ärimudel, püsivad rahavood ja kõrge dividendimäär on see, mis on ebamäärase majanduskeskkonna ja madalate riigivõlakirjade tulususmäärade tingimustes praegu "in". -

Suurbritannia juunikuu kaubandusbilansi (v.a teenused) puudujääk tuli oodatud £7,8 miljardi asemel £7,4 miljardit ja ühtlasi langes eelmise kuu £8,03 miljardi pealt. Täielik kaubandusbilansi puudujääk oli samuti oodatust madalam: £3,26 miljardit vs oodatud £3.65 miljardit. Uudistest naelsterlingile erilist tuge ei olnud ja kaupleb hetkel dollari ja euro vastu madalamal.

-

paidContentUK vahendusel saab teada, et Skype'il on probleeme oma kaubamärgi registreerimisega, sest sõna "sky" sisaldub ühe teise ettevõtte nimes. Väljavõte artiklist:

In particular, in the European Union, India, Norway and Brazil, our applications in respect of the Skype name are being opposed by BSkyB plc., a British satellite broadcaster, Internet service and telephony service provider, or by one of its affiliates. These oppositions are based on BSkyB’s claimed rights with respect to the mark “SKY".

To date, we have successfully defended these oppositions in Switzerland and Turkey and to date have received a positive decision in Brazil. However, on July 6, 2010, we received a negative first instance decision from the European Union trademark registry (OHIM) on BSkyB’s opposition proceeding against the Skype bubble logo trademark application.

-

Q2 tootlikkuse muutus oli USA majanduses oodatust kehvem (esimest korda negatiivne alates 2008a viimasest kvartalist). Vähemalt Q1 osutus esialgsest hinnangust märgatavalt paremaks:

Q2 Productivity- prelim -0.9% vs +0.1% Briefing.com consensus, prior revised to +3.9% from +2.8%

Q2 Unit Labor Costs +0.2% vs +1.4% Briefing.com consensus, prior revised to -3.7% from -1.3%

-

Gapping up

In reaction to strong earnings/guidance: QNST +14% (light volume), ZOLT +8.5%, FOSL +7.1%, CSKI +6.5%, CXDC +6.4%, MBI +5.5%, DEER +5.2%, JASO +3.3%, TTM +3.2%, ERES +3.2% (also upgraded to Buy from Hold at Duncan Williams), TTM +2.7%, SYUT +2.5%, PRGN +2.1%, IRDM +1.2%, GNK +0.9%, GEOY +0.4%.Other news: ROYL +8.7% (has tested and completed the LoneStar Northeast Parks well and the Victor Ranch 3-9), SGMO +6.6% (still checking), VLTR +6.3% (will replace Phase Forward IN S&P600), YMI +4.5% (granted Orphan Drug Designation for CYT387), ORN +4.2% (will replace Odyssey HealthCare in S&P600), KIRK +4.2% (light volume; will replace Stanley in S&P600), ELN +3.1% (Elan And Transition Therapeutics announce topline summary results Of Phase 2 study and plans for Phase 3 for ELND005; provides update on initiatives to further enhance balance sheet and operating performance), ESRX +1.5% (Cramer makes positive comments on MadMoney).

Analyst comments: AKAM +1.2% (upgraded to Buy from Neutral at Goldman), WFMI +0.8% (upgraded to Buy from Neutral at UBS).

Gapping down

In reaction to strong earnings/guidance: ABK -22.2%, AGM -13.0%, MR -11.5% (also downgraded to Hold from Buy at Soleil), RTK -9.8%, MPG -9.0%, SCLN -8.5%, VSAT -7.7%, FEED -7.6%, NUAN -7.0%, ASEI -6.6%, BBBB -6.4%, IHG -5.9%, CWCO -5.4% (also downgraded to Hold from Buy at Brean Murray), RAX -5.0%, AVII -4.0% (light volume), QGEN -3.6%, SLXP -2.1% (light volume).Select financial related names showing weakness: RBS -5.4% (downgraded to Neutral from Outperform at Credit Suisse), AIB -4.4%, IRE -3.6%, LYG -2.5%, ING -3.5%, CS -2.9%, UBS -2.5%, RF -2.4%, DB -2.3%.

Select metals/mining stocks trading lower: GSS -4.7%, RTP -3.8%, BHP -3.7%, HL -2.7%, IAG -2.5%, GFI -2.3%, VALE -2.3%, HMY -2.2%, SLW -2.2%, NGD -2.0%.

Select oil/gas related names showing weakness: SD -3.3% (also hearing weakness attributed to tier 1 firm downgrade), COP -2.6%, ATPG -2.2%, APC -2.1%, E -2.1%, BP -2.0%, SU -1.8%, MEE -1.7%.

Other news: HQS -8.2% (continued weakness following earnings), NFBK -3.8% (to commence stock offering), CPLP -3.6% (announces offering of 5,500,000 common units and Intention to Acquire MR Tanker M/T Assos), NGLS -3.4% (announces a 6.5 mln share common unit offering), JCP -2.5% (weakness attributed to tier 1 firm downgrade before the open), SCG -1.9% (South Carolina Supreme Court issues ruling on base load review order, SCE&G nuclear project to continue as planned), JNJ -1.1% (weakness attributed to tier 1 firm downgrade before the open), .

Analyst comments: LOPE -5.8% (downgraded to Outperform from Top Pick at RBC Capital), ASCA -5.0% (initiated with a Sell at Merriman), NTLS -3.0% (downgraded to Market Perform from Outperform at Wells Fargo), INTC -2.2% (downgraded to Neutral at Baird ), ALV -1.5% (downgraded to Hold from Buy at Deutsche Bank).

-

USA futuurid indikeerimas avanemist ca protsendi jagu madalamal eilsest sulgumistasemest

Euroopa turud:

Saksamaa DAX -1,17%

Pantsusmaa CAC 40 -1,14%

Suurbritannia FTSE100 -0,72%

Hispaania IBEX 35 -0,75%

Rootsi OMX 30 -0,66%

Venemaa MICEX -1,87%

Poola WIG -1,34%Aasia turud:

Jaapani Nikkei 225 -0,22%

Hong Kongi Hang Seng -1,50%

Hiina Shanghai A (kodumaine) -2,90%

Hiina Shanghai B (välismaine) -1,88%

Lõuna-Korea Kosdaq -0,35%

Tai Set 50 -1,65%

India Sensex 30 -0,37% -

Rev Shark: Don't Fight the Fed

08/10/2010 7:47 AMThus it is that in war the victorious strategist only seeks battle after the victory has been won, whereas he who is destined to defeat first fights and afterwards looks for victory.

-- Sun Tzu

Market players often toss around trite little sayings like "buy low and sell high", "never short a dull market" and "buy the rumor, sell the news". They all contain an element of truth, but there is one aphorism that is probably more accurate than most: Don't fight the Fed.

The idea behind that saying isn't difficult to understand. The Fed controls the money supply, and the money supply drives the stock market. When interest rates are low and there is lots of cheap money, much of it will flow into the market and drive up prices.

The action in the market since the low in March 2009 is a particularly good example of how the Fed can drive the market. What drove the rally wasn't major economic recovery or bullish sentiment -- it was a flood of cheap dollars that had few good investment alternatives. That money was parked in the market and just kept us running higher, often in a technically unusual fashion.

So the question for us to ponder later today, when the FOMC issues its latest interest-rate decision, is whether there is a new market driver that we need to embrace. It is a particularly important decision this time, because there has been much speculation lately that continued softness in unemployment and the danger of deflation supports further monetary easing by the Fed.

Critics of another round of quantitative easing believe that the Fed doesn't have room to do much, as interest rates are already effectively zero. In addition, the problem doesn't seem to be the availability of cheap capital, but the lack of confidence of both potential borrows and lenders. The economic future is too uncertain, especially with taxes rising, the federal deficit growing and the impact of costly new programs like the health-care bill. It isn't the supply of cheap capital that is a problem, but the demand for it, so the Fed will not help the economy by perpetuating an endless flood of cheap money.

Most economists don't expect the Fed to make a major move today. At best, it may hint that it is ready, willing and able to produce more accommodative monetary policy as needed. The bulls are going to react favorably to any such hints, not because it is good for the economy, but because it is good for the stock market when there is more cash looking for some sort of return.

As we can see this morning, the market is already quite nervous over what we may see from the central bank. I suspect the policy statement will be quite vague and leave the door open for anything. That will probably disappoint bulls, who are looking for more decisive action by the Fed in reaction to continued weakness in employment.

My style is to not bet on this news, but to play the reaction once it is out. I think there is substantial danger that the market will be disappointed, and I don't want to carry much inventory into the news. Once the announcement is made, we can assess the situation and act accordingly. The way the market is acting right now suggests the bulls may be losing some of the optimism that helped prop us up over the past couple of weeks.

-

$34 bln 3-year Note Auction Results: Yield 0.844% (expected 0.862%); Bid/Cover: 3.31x (Prior 3.20x, 12-auction avg 3.06x); Indirect Bidders: 40.5% (Prior 40.6%, 12-auction avg 52.2%)

-

Nõrk QE

-

FOMC leaves benchmark Fed Funds rate at 0.00-0.25%, as expected

Fed to reinvest maturing agency and MBS securities in treasuries

To help support the economic recovery in a context of price stability, the Committee will keep constant the Federal Reserve's holdings of securities at their current level by reinvesting principal payments from agency debt and agency mortgage-backed securities in longer-term Treasury securities. The Committee will continue to roll over the Federal Reserve's holdings of Treasury securities as they mature.

Ten-year Treasury yield sees initial drop to 2.79% from 2.82% following FOMC announcement, then a sharp rally back to 2.81% -

To help support the economic recovery in a context of price stability, the Committee will keep constant the Federal Reserve's holdings of securities at their current level by reinvesting principal payments from agency debt and agency mortgage-backed securities in longer-term Treasury securities.

-

See siiski tähendab seda, et balance sheet ei laiene vaid seda hoitakse stabiilsena, st ei lasta väheneda

-

see ka

The Committee will continue to roll over the Federal Reserve's holdings of Treasury securities as they mature.

Väike küsimus oli mõnedel, et mis saab kui paberid aeguma hakkavad. Nüüd siis selgus: maht säilitatakse. -

Pimco's Bill Gross, on CNBC, says he would buy govt owned enterprises, whether it be AIG, GMAC, or Citi -calls them high yield plays

-

pace of economic recovery is likely to be more modest in the near term than had been anticipated

-

Ilusad Q2'10 tulemused ja Fedi QE vol2 nüüd selja taga ning tõenäoliselt veidi nõrgemad makronäitajad ees ootamas. Mis võiks olla see katalüsaator, mis siis Q2'10 tulemuste ajal tugevalt tõusnud turgu võiks siis siit veel edasi lükata? Kas pole nüüd mitte karudel pisut jämedam ots käes...

-

VOl 2 see siiski veel pole. Pigem 1.1

-

The House passes the $26 bln State Aid bill, as expected