Börsipäev 8. september

Kommentaari jätmiseks loo konto või logi sisse

-

Euroopa pankade stressitesti küsitav usaldusväärsus ning jätkuv mure riikide võlaprobleemide pärast (pikemalt saab lugeda WSJ eilsest artiklist) kahjustas sentimenti eile USA-s ning täna hommikul ka Aasias. Langejate eesotsas on teist päeva Jaapan, kus tugevnev jeen kahjustab eksportijate majanduslikke väljavaateid. Nikkei -2,18%, Hang Seng -1,24%, CSI 300 -0,07%. USA futuurid kauplevad 0,1% plussis, tehes mõni hetk tagasi -0,1% pealt kerge spike'i.

USD/JPY graafik

Makrost on täna Euroopas oodata Saksamaa ning Suurbritannia juulikuu tööstustoodangu numbreid (vastavalt kell 13.00 ja 11.30). USA-s seevastu võib volatiilsemaks kujuneda just päeva lõpp, mil avalikustatakse FED-i Beige Book (kl 21.00) ja tarbijakrediidi näit (kl 22.00). Kanada keskpank langetab intressimäära otsuse kell 16.00 ning 19-st Bloombergi analüütikust 13 ootab tõstmist 0.75%-lt 1.00%le.

-

UBS dailyst paar märkust kasvuootustest:

+ German factory orders were weaker than expected yesterday. Today we get more information with industrial production and export data. There is likely to be some softening in exports (albeit limited), which may moderate the production figure.

+ We have already seen weakness in the export figures of Korea and Taiwan. It is worthwhile remembering that exporters do not sell to consumers (generally speaking) but instead sell into inventory. If the (weak) inventory restocking process is over, export led growth must moderate.

-

Marc Faber on oma viimases GBD raportis üsna veendunud, et lähikuudel on USA-s oodata uut stiimulpaketti ning täiendavat rahatrükki, mis paneb raha voolama võlakirjadest uuesti aktsiatesse. Siin on mõned mõtted:

So, no matter how good or, more likely how bad the economy turns out to be over the next 12-24 months and beyond, liquidity will flow somewhere and provide investors with money-making opportunities. The big question for large asset allocators is when to exit the US Treasury and the Japanese Yen and move back into equities. Obviously, Treasury bonds and the Yen won’t continue to appreciate forever. My humble view is that we are getting very close to major inflection points. On the highly likely announcement of further stimulus measures and more quantitative easing (or other gross government interventions into the free market) within the next three months, I expect to see the Treasury bond market implode and money flow into precious metals and equities. Moreover, once the S&P declines to between 870 and 950, the Obama administration will implement even more irresponsible economic policy measures, which will be Treasury bond unfriendly but are likely to boost precious metal prices and support equities.

-

Patsiga onu track on viimasel ajal päris hea olnud! ;)

-

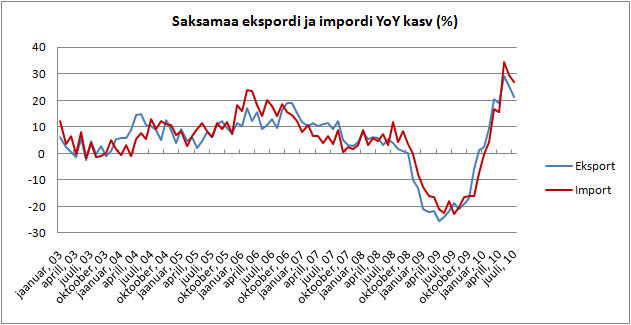

Täna avaldatud makromajanduse näitajatest langes Saksamaa eksport juulis 1.5% MoM, mis on esimene kord kolme kuu jooksul ning import kahanes 2.2% MoM. Suurbritannia juulikuu tööstustoodangu näitaja jäi ootustele alla, kasvades 0.3% vs oodatud 0.4% MoM ning 1.9% vs 2.0% YoY. Sesoonselt korrigeeritud Jaapani (tuum) masinate tellimused ületasid ootusi ning kasvasid 8.8% vs oodatud 2.0% MoM.

-

Normaliseerumine, millele Kristo UBS-i kommentaarides tähelepanu juhtis on näha hommikul avaldatud Saksamaa kaubandusbilansi andmetest, kus sarnaselt eilsetele tehaste tellimustele on oodatust suurem kukkumine toimunud ka ekspordis. Müük välismaale vähenes juulis -1,5% võrreldes juuniga, mil see kasvas 3,7%, samas kui Bloombergi analüütikud olid oodanud 0.0%-list muutust. Juuli import vähenes -2,2% võrreldes juuniga (samuti prognoositust enam), kaubandusbilansi ülejääk suurenes aga 12,4 miljardilt eurolt 12,7 miljardile.

-

defitsiii? ülejääk vist ikka seal? vahe neil kahel mõistel suhteliselt oluline ju.

-

ELSTATi esialgsel hinnangul vähenes Kreeka SKP teises kvartalis yoy 3.7%. Kvartalite võrdluses langus kiirenes, esimeses kvartalis oli qoq langus 0.8% ning teises kvartalis oli vastav näitaja -1.8%. Eratarbimine vähenes aastataguse ajaga võrreldes 4.2%, Q1 2010 oli kasv yoy 1.5%.

-

randy, ....jah, muidugi suurenes ülejääk 12,4 pealt 12,7 peale, mitte defitsiit. tänud.

-

Täna pärast päikeseloojangut tähistatakse heebrea kalendri järgi Rosh Hashanahi (10 päeva enne Yom Kippuri) ehk tavakõnes tuntud kui juutide uusaasta algust. Finantssektoris on juutide esindajaid üldiselt palju, mistõttu on järgnevatel päevadel ilmselt nii mõnigi suur turuosaline eemal.

-

Hava nagila, hava nagila

Hava nagila venis'mecha

Hava neranena, hava neranena

Hava neranena venis'mecha

Uru, uru achim

Uru achim belev same'ach

:-)))

/Tervitan ka Sommi... -

Germany's industrial production edged up 0.1% in July from the previous month, the economics ministry in Berlin reported on Wednesday. The result was below market expectations for a monthly rise of 1%.

Indeksid, nafta ja EUR liikusid selle peale hetkeks alla, kuid nüüd kaubeldakse juba kõrgemal. DAX -0,42%, ES -0,11%, EUR/USD +0,2% @ 1,270.

-

Veidi pikemat lugemist Kreeka teemal Michael Lewiselt, kes käis ise kohapeal eluolu uurimas. Link

-

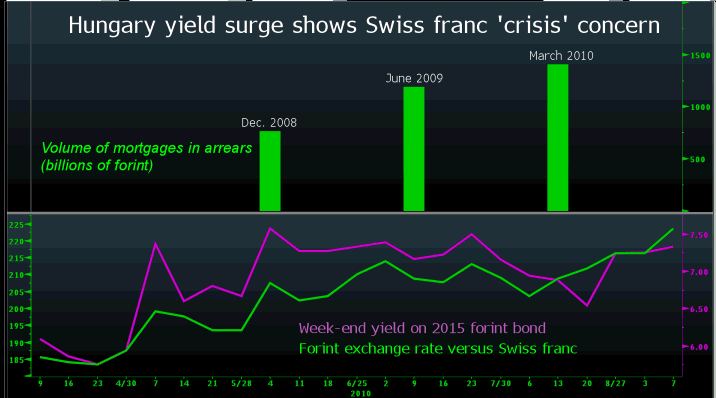

Vaesed ungarlased, kes laenubuumi ajal madalamaid intresse jahtisid ja laenusid valdavalt välisvaluutas välja võtsid, tunnevad nüüd kuidas valu on rekordkalli CHF tõttu deebitoride jaoks (ja sealt ka kreeditoride jaoks) väljakannatamatuks muutumas. Ungari keskpanga andmetel ulatub elanike välisvaluutas võetud laenukoormus 7,3 triljoni forintini ehk ligi 70% majapidamiste kogukrediidist. Sellest omakorda 82% on Šveitsi frankides, mille kallinemine forinti suhtes on muutnud tagasimakse kohustuse paljude jaoks ülejõukäivaks. Allolevalt graafikult on näha, et tähtajaks tasumata laenude maht ulatus 2010.a esimeses kvartalis 1.4 triljoni forintini, olles 2008.a detsembris olnud 765 miljardit forinti. Kohaliku pangandusassotsiatsiooni presidendi sõnul võib ebatõenäoliselt laekuvate laenude maht pankade bilanssides kasvada aasta lõpuks 10%-ni. (7,8% 2009.a lõpus), mistõttu võivad sellised nimed nagu OTP, Erste Group ja Foldhitel es Jelzalogbank Nyrt mingil hetkel täiendavat kapitali vajada.

-

Gapping down

In reaction to disappointing earnings/guidance: SLAB -11.6%, TLB -10.0%, CIEN -1.7%.M&A news: CPII -8.6% (Comtech and CPI International Announce Termination of Merger Agreement).

Select European financial names under pressure: IRE -4.3%, UBS -1.3%, BCS -1.1%, CS -1.0%

Other news: EXLP -3.9% (Exterran Partners and Exterran Holdings announce secondary offering of common units), NRGY -3.5% (announces Public Offering of 8.5 mln Common Units), UDR -3.1% (to sell 13.5 mln shares of common stock in underwritten public offering; net proceeds to fund potential and recent acquisitions, pay down debt and for general corp purposes), MAPP -2.6% (reports no difference in pulmonary artery pressure between LEVADEX and placebo in Pharmacodynamics Trial; complete treatment of 2 LEVADEX clinical programs), NI -2.2% (commences public offering of up to $400 mln of its common stock; to use to use any net proceeds for general corporate purposes), FMCN -1.4% (files for ADS shelf offering; announced the underwritten public offering of 8.1 mln of its American depositary shares held by JJ Media Investment Holding Limited ), V -1.0% (attributed to tier 1 firm downgrade).

Analyst comments: WDC -2.4% (downgraded to Neutral from Buy at UBS), BAX -2.0% (trading ex dividend; downgraded to Sell from Hold at Citigroup), HPQ -0.7% (downgraded to Neutral from Buy at UBS),

Gapping up

In reaction to strong earnings/guidance: NTWK +10.2%, ALTR +2.6%, PVH +2.0% (also upgraded to Overweight from Neutral at Piper Jaffray).M&A news: ZGEN +65.1% (Bristol-Myers Squibb to Acquire ZymoGenetics for $9.75 in cash; dilutive for BMY in 2010 and 2011), QXM +31.8% (Qiao Xing Universal announces proposal to acquire all outstanding shares of Qiao Xing Mobile for 1.9 shares of its common stock plus US$0.80 in cash per share), TUNE +17.0% (Microtune to be acquired for $2.92 per share in cash by Zoran Corp or ~$166 mln).

Select metals/mining stocks trading higher: GOLD +2.0%, NG +1.8%, SLW +1.8%, IAG +1.7%, HL +1.5%, CDE +1.5%, CLF +1.4%, BBL +1.4%, AUY +1.2%, SLV +1.2% (positive comment on MadMoney).

Select European drug names trading higher: SNY +2.6%, AZN +1.4%.

Other news: SKH +36.7% (agrees to settle Humboldt County Class Action), HTM +23.7% (announces strategic investment by Enbridge in Neal Hot Springs ), ARMH +6.2% (strength attributed to RBS comments related to Samsung order), BP +3.4% (report on causes of Gulf of Mexico tragedy; investigation found that no single factor caused the Macondo well tragedy.... Also Fitch ugrades BP plc to 'A' from 'BBB'; Outlook Stable), VRTX +2.9% (announces Telaprevir phase III study results; 65% of people whose prior treatment for Hepatitis C was unsuccessful achieved SVR with Telaprevir-based therapy).

Analyst comments: MGM +3.4% (upgraded to Buy from Hold at Soleil), SPLS +2.3% (upgraded to Buy from Neutral at Goldman), COST +1.4% (upgraded to Buy from Neutral at Goldman), SLB +0.6% (initiated with Outperform at Wells Fargo).

-

Bank of Canada raises rates 25 bps to 1.00%, as expected

-

USA turud alustamas kerges plussis: ES +0,16%, YN +0,15%, NQ +0,32%. Nafta kaupleb -0,16% @ 73,98 ja ja kuld flat @1257.

Euroopa turud:

Saksamaa DAX +0,31%

Pantsusmaa CAC 40 +0,52%

Suurbritannia FTSE100 +0,15%

Hispaania IBEX 35 +0,60%

Rootsi OMX 30 +0,30%

Venemaa MICEX +1,49%

Poola WIG +1,04%Aasia turud:

Jaapani Nikkei 225 -2,18%

Hong Kongi Hang Seng -1,46%

Hiina Shanghai A (kodumaine) -0,11%

Hiina Shanghai B (välismaine) -0,10%

Lõuna-Korea Kosdaq -0.33%

Tai Set 50 -0.05%

India Sensex 30 +0,12% -

Moody's reports that although U.S. rated bank asset quality continues to improve, the credit outlook for the U.S. banking industry continues to be negative

-

Rev Shark: Reacting, Not Predicting

09/08/2010 8:08 AM"Success always comes when preparation meets opportunity"

-- Henry Hartman

Success in the market is primarily a function of being prepared to act as conditions change. If you have an open mind, a plan of attack and you move aggressively at the right time, you will do very well, no matter which way the market evolves.

Unfortunately, too many market players think that market success is all about grand predictions. They position themselves based upon carefully thought-out macroeconomic theories and then just wait for the money to roll in. Occasionally, it actually does work, but more often than not, the market does not immediately cooperate, and when it finally does act as anticipated, the original positioning is so stale that there is barely a profit to be made.

My approach to the market is to be reactive rather than anticipatory. I don't want to make predictions and hope. I want to see how the market is acting and then move quickly to capitalize on emerging themes and trends. I'll be the first to admit that I have little interest in making the sort of grand market predictions that are so popular in the media. Those predictions are always entertaining, but I bet the majority of people who act on them lose money, because even when they do have it right, the timing is off. If you don't have the timing right, it is almost as bad as being wrong.

Right now the market is at a particular point where good preparation is extremely important. You don't need to be bullish or bearish; you just need to be aware of the conditions in place and be ready to act as things develop. Maybe we'll be big buyers, but maybe we won't. The market will be the guide.

First let's consider the big picture. We had a good rally last week that cut through some resistance levels, but we gave back a chunk yesterday during a slow and uninteresting session. We didn't do any major technical damage, so we are in pretty good shape for another attempt at those August highs, which are the key levels to the upside.

The most interesting thing about the action yesterday was that, although breadth was poor and plenty of stocks pulled back, many of the recent momentum leaders held up fairly well. It is a positive that they have relative strength but a negative because it doesn't offer easy entry points.

Speaking of winning stocks, the most important thing we can do at a point like this is make sure we have a good watch list of stocks that we want to buy if the market is cooperative. Being ready to act quickly is the real key to effectively trading. I've mentioned quite a few names here recently, and many of them remain on my watch list, including Ameresco (AMRC - commentary - Trade Now), China New Borun (BORN - commentary - Trade Now), Nanometrics (NANO - commentary - Trade Now), Entropic Communications (ENTR - commentary - Trade Now), Rare Element Resources (REE - commentary - Trade Now) and Amtech Systems (ASYS - commentary - Trade Now).

If the market finds some momentum, these are the first names I'll be looking to buy. If things soften further and it looks like we are going to test support at the 50-day simple moving average on the S&P 500 (around 1,080), then I'll keep stops tight and cut back my positions.

I don't have to know which way the market is going to move; I just have to be ready to act as things develop. It requires vigilance and fast action, but I prefer that over the prognostication that most market players think is the road to riches.

We have a positive start on the way, but it is very quiet out there and we have little news. The Beige Book report is due out later today, but I'm looking for another day of light volume.

At the time of publication, Rev Shark was long AMRC, BORN, NANO, ENTR and REE, although positions may change at any time.

-

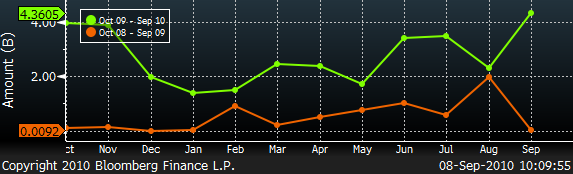

Huvitavat informatiooni Bloombergi vahendusel:

Nimelt on NASDAQ’i IPO’de tootlus on esimest korda viimase kümnendi jooksul S&P 500 indeksi tootlusest madalam. Kui investor oleks osalenud kõikidel käesoleval aastal toimunud 43 IPO’l, siis oleks tema porfelli tootlus langenud ca 5.2%. S&P 500 indeks on aga käesoleval aastal langenud vaid 1.5%. Bloombergi andmetel oli NASDAQ’i IPO’de tootlus vahemikus 1999 kuni 2000 keskmiselt 42% S&P 500 indeksi tootlusest kõrgem – trend on selgelt muutunud. All on ka graafik toimunud IPO’de väärtusest (ajaperiood oktoober 2009 – september 2010).

-

$21 bln 10-year Auction Results: Yield 2.670% (expected 2.685%); Bid/Cover 3.21x (Prior 3.04x, 12-auction avg 3.03x); Indirect Bidders 54.7% (Prior 45.8%, 12-auction avg 41.2%)

Kommentaar oksjonile järgmine:

The reopened $21 bln 10-yrs draw 2.670%, well below the yield anticipated, with a 3.21 cover, well above average with $3.21 submitted for each $1 on offer. The indirect bidder participation take of 54.7% was also solid, best since No 2005 -

July Consumer Credit -$3.6 bln vs -$5.2 bln Briefing.com consensus; prior revised to -$1.0 bln from -$1.3 bln

-

Kas lisatõlgendust trsry oksjonile ka on või? Miks nii hea tulemus? Kas mingi flight to safety ilming?

-

To: momentum

Hetkel paistab crowded trade, kuigi võlakirjaturg peaks olema suurte poiste mängumaa.