Börsipäev 13. september

Kommentaari jätmiseks loo konto või logi sisse

-

Nädalavahetuse kaks uudist on täna hommikul toetamas Aasia turge ning vedanud USA indeksid juba 0,8% kõrgemale võrreldes reedese sulgumisega. Esiteks rõõmustas pangandussektor, kui globaalsed regulatiivorganid jõudsid kokkuleppele uutes kapitaliadekvaatsuse nõuetes, mis ei osutunud nii karmiks kui paljud olid oodanud ning lisaks annab sektorile kaheksa aastat aega, et minimaalset tuumik tier-1 suhtarvu praeguse 2% pealt 4,5% peale tõsta (sellele lisandub veel täiendava puhvrina 2.5%, alla mille hakkavad pangale kehtima piirangud boonuste ja dividendimaksete tegemisel).

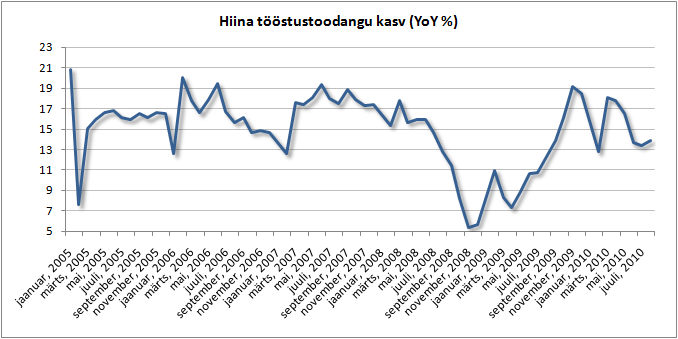

Lisaks Basel III nõuetele külvas turgudel optimismi Hiina prognoositust parem tööstustoodangu kasv augustis, paranedes aastaga 13,9% versus 13,4% juulis, tõestades et valitsuse senised pangandussektorile seatud piirangud pole majanduskasvu rõhumas. Bloombergi küsitletud analüütikud olid oodanud 13%list tõusu. Sisemaise nõudluse tugevust näitas ka jaemüügi 18.4%-line tõus, kiirenedes juuli 17.9% pealt.

Olulist makrot pole täna oodata ei USAs ega ka Euroopas.

-

Et saada paremat aimu Hiina tööstussektori võimsast kasvust viimaste aastate jooksul....

-

Niipea kui taastub isu riskantsemate varade vastu, hakatakse dollari ja jeeni positsioone ümber mängima euro kasuks, mida ilmestab tänane põrge 1,2680 pealt 1,2720 peale, kui Euroopa futuurid on indikeerimas avanemist ca 1% jagu kõrgemal võrreldes reedese sulgumisega.

-

Wall Street Journal kirjutab, et Hewlett-Packard (HPQ) on läbirääkimistes järjekordse ülevõtmise läbiviimiseks. Ülevõetavaks on turvatarkvara tootev ArcSight (ARST). HP pakub ettevõtte eest $1.5 miljardit, mis tähendab ca 25% suurust preemiat võrreldes reedese turukapitalisatsiooniga. ArcSight toodab tarkvara, mis jälgib ebatavalist tegevust arvutivõrkudes, näiteks häkkerite katseid süsteemi sissemurdmiseks. Ettevõtte tooteid kasutab rohkem kui 1000 klienti, et vältida küberrünnakuid. Siiski pole asjaosaliste sõnul tehingu toimumine veel kindel.

-

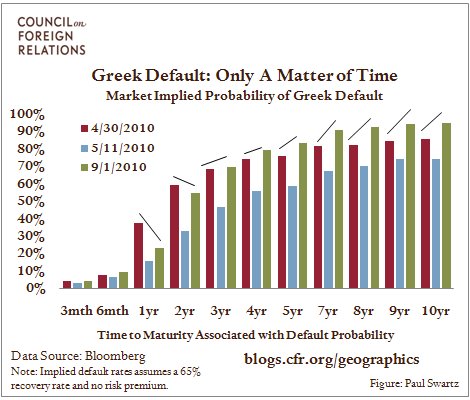

Council on Foreign Relations on oma graafiku peal võtnud hästi kokku arengud Kreeka valitsuse võlakirjaturul, kus näeme et pärast mais teatavaks tehtud EL-i ja IMF-i abipaketti toimus erinevate aegumistähtaegadega võlakirjade tulusustes kohene langus (Saksamaa vastavate võlakirjadega võrreldes), kuid sellest hetkest alates hakkasid need taas vaikselt kerkima ning pikema perioodi võlakirjade puhul on intresside erinevused tänaseks juba suuremad kui aprillis. Seega, mida pikem perspektiiv Kreeka majanduse osas võetakse, seda suuremaks hinnatakse makseraskustesse sattumise tõenäosust.

-

Euroopa Komisjon on tõstis täna eurotsooni 2010.a SKT kasvuootuse maikuu prognoosidega võrreldes 0,9% pealt 1,7% peale, ent sarnaselt paljudele turuosalistele nähakse tempo aeglustumist nii kolmandas kui neljandas kvartalis.

-

Kreeka uute ehituslubade arv langes juunis yoy 13% ning 2010. aasta esimeses pooles langes vastava näitaja 8.6%. Ehitusmahud vähenesid 24.4% ning ehitatavat pindala oli poolaastal 18.7% vähem võrreldes eelmise aasta sama perioodiga. Eelmisel aastal vähenes ehituslubade arv 14.2%.

-

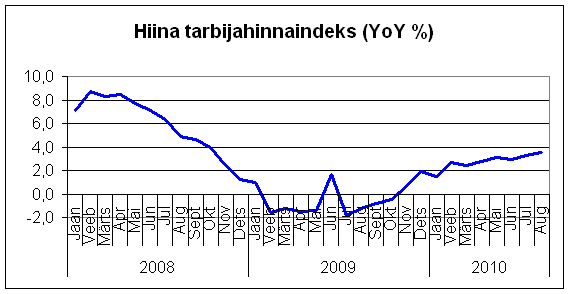

Hiina tarbijahinnaindeks kasvas augustis 22 kuu kiiremais tempos, tõustes 3.5% yoy. Kasv põhines üleujutuste tagajärjel 7.5% yoy kerkinud toidukaupade hindadel, mis moodustavad 1/3 indeksi väärtusest.

-

Bank of International Settlement of Basel III kohta ka ülemineku tabeli koostanud:

http://www.bis.org/press/p100912b.pdf

Samuti mainis Goldman Sachs, et nende poolt analüüsitavatest Euroopa pankadest, et täida ainutl 4 praeguses seisuse Basel III nõudeid.

-

Gapping down

In reaction to disappointing earnings/guidance: NTSC -7.1%.Other news: SCOK -23.0% (continued weakness; still checking for anything new), MTRX -3.3% (files an extension of time to file its 10-K for FY10 and Q4 earnings release due to recently discovered alleged fraudulent activities), PCX -2.8% (provides update for Q3: expected volume -10% from earlier est. to 7.5-7.7 mln tons ), VMW -1.9% (weakness attributed to negative mention in finance newspaper), SGEN -0.7% (phase IIb clinical trial of lintuzumab in older patients with acute myeloid leukemia did not meet its primary endpoint of extending overall survival; co will discontinue its development program for lintuzuma).

Analyst comments: AZO -1.3% (downgraded to Sell from Neutral at Goldman).

Gapping up

M&A news: GTSI +33.2% (Eyak Technology announces cash offer of $7.00/Share for GTSI), ARST +25.2% (ArcSight confirms it will be acquired by HPQ for $43.50 per share, or an enterprise value of $1.5 bln), DTG +5.0% (Dollar Thrifty and Hertz agree to $50/share offer).Select financial related names showing strength: ING +3.6%, IRE +3.4%, RF +3.0% (upgraded to Outperform from Market Perform at Bernstein ), CS +3.0%, DB +3.0% (approves takeover offer for Postbank ), HBC +2.8%, PUK +2.8%, LYG +2.8%, AEG +2.7%, HBAN +2.6% (upgraded to Outperform from Market Perform at Bernstein), BAC +2.5%, UBS +2.1%, STD +1.7%, BCS +1.3%, .

Select metals/mining stocks trading higher: RTP +2.7%, TCK +2.4%, MT +2.3%, BBL +2.3%, BHP +2.1%, FCX +2.0%, AKS +1.9%, SVM +1.8%, AA +1.7%, MTL +1.7%, GFI +1.4%.

Select oil/gas related names showing strength: LNG +12.4% (continued momentum), CRZO +3.7%, CEO +3.6%, APC +3.2% (announces successful Owo-1 Sidetrack), STO +2.5%, RIG +2.4%, LLEN +2.2%, WLT +2.1%, RDS.A +1.6%, PBR +1.6%, BEXP +1.1% (announced a $250 mln sr notes offering).

Select European drug names trading higher: AZN +1.9%, SNY +1.4%.

Other news: OXGN +81.5% (ZYBRESTAT improves overall survival in a Phase 2/3 Trial of patients with Anaplastic Thyroid Cancer), INO +17.1% (achieves unprecedented T-Cell immune responses in human trial of DNA Vaccine for Cervical Dysplasia and Cancer caused by HPV ), ASTI +12.4% (signs distribution agreement with Radiant Holding, of China), XRX +5.4% (strength attributed to positive mention in finance newspaper), CGNX +4.7% (Cramer makes positive comments on MadMoney), VICL +4.2% (TransVax CMV Vaccine achieves statistical significance on key clinical endpoints in Phase 2 Trial), WSM +1.9% (ticking higher; authorizes a new $65 mln stock repurchase program), .

Analyst comments: MSFT +1.5% (initiated with a Buy at Standpoint Research), PXP +0.9% (upgraded to Buy from Hold at Hapoalim).

-

Rev Shark: A Promising Setup

09/13/2010 7:25 AMA positive attitude may not solve all your problems, but it will annoy enough people to make it worth the effort.

-- Herm AlbrightWe are kicking off the week with another Monday-morning gap. Since the bottom in March 2009, a huge portion of the overall gains in the market have come on these Monday-morning gaps. If you missed them, you have missed out on the "easy" gains in the market -- if there is such a thing. This tendency is just one of the aspects of this market that has made it so tough in past year or two.

Chasing the Monday-morning strength has worked at times, but generally aggressive traders look to fade strong opens. The key is to see where we are an hour or so after the open. If the dip-buyers jump in aggressively on early weakness, then the chances of a "trend" day increase quite a bit.

Monday-morning gaps are always tricky, but overall the technical condition of the major indices is promising. As I discussed last week, we are in a trading range with the S&P 500 sitting safely between its 200-day and 50-day simple moving averages. The downside support is at 1085, while the upside resistance is at 1115 and then at the August highs around 1125. Volume has been light and we are a little overbought, especially with this gap-up open, but it is a constructive pattern with good support and there is no reason to be unduly bearish. Some rest or even a pullback would be quite healthy.

I've also found the aggressive pockets of momentum quite positive lately. Part of that momentum is due to takeovers (as in ArcSight (ARST - commentary - Trade Now) and 3Par (PAR) - commentary - Trade Now), but there has been quite a bit of hot money looking for a place to go, and it has persistently chased some stocks like Salesforce.com (CRM - commentary - Trade Now). Apple (AAPL - commentary - Trade Now), Netflix (NFLX - commentary - Trade Now), etc.

Although the Nasdaq has been up six of the last seven days, I was a bit surprised to find a fair number of attractive chart setups this weekend. It has been a much better market for individual stock-picking lately, which is a very nice change. For most of last year and early this year, the market was all about macroeconomics. Stocks as a group would move together, and you couldn't really gain much of an edge by focusing on individual stocks. In fact, you were often better off just sticking with the ETFs and focusing on market timing. Finding good stocks has always been the fun part of trading, so it is a relief to see a somewhat better environment for that this morning.

Today we have a strong open that's being caused by two things. First, banks in Europe rose sharply following the news that they will have to hold more capital in reserve. That sounds like a negative, but the positive part was that the transition will continue through January 2019, giving banks plenty of time to find ways to deal with these new rules.

The second positive this morning is good economic news from China. Factory production was well above expectations. There is a little less concern that this is just a very strong economy rather than an overheated one. The strength in China is helping to drive up energy and mining shares this morning.

So we have a Monday-morning gap and slightly overbought conditions that we have to be a little wary of, but this is also a generally positive market environment with good momentum and technical setups. I'll probably do a little selling into early strength, but we'll see how well we hold and then go from there.

No positions.

-

USA turud on suutnud hoida börsipäeva alguses välja toodud plussi. ES +0,83%, YN +0,73%, NQ +0,71%. Nafta kaupleb +1,1% @ 77,3 USD ja ja kuld -0,21% @1241,8 USD.

Euroopa turud:

Saksamaa DAX +0,82%

Pantsusmaa CAC 40 +1,07%

Suurbritannia FTSE100 +1,02%

Hispaania IBEX 35 +0,68%

Rootsi OMX 30 +0,87%

Venemaa MICEX +0,59%

Poola WIG +1,28%Aasia turud:

Jaapani Nikkei 225 +0,89%

Hong Kongi Hang Seng +1,89%

Hiina Shanghai A (kodumaine) +0,94%

Hiina Shanghai B (välismaine) +0,85%

Lõuna-Korea Kosdaq -0,20%

Tai Set 50 +1,60%

India Sensex 30 +2,17% -

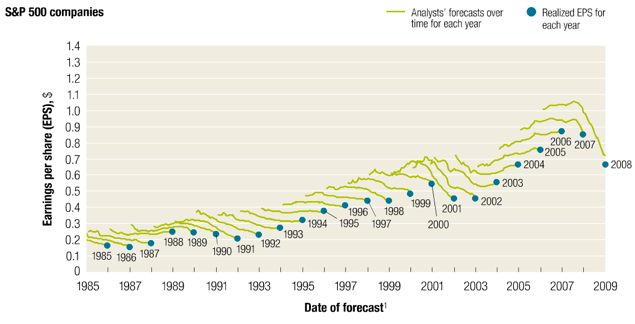

McKinsey & Company on koostanud huvitava graafiku. Ettevõte väidab, et ajalooliselt vaadatuna on analüütikute EPSi prognoosid olnud liialt optimistlikud. Muutustele majanduses reageeritakse aegsasti ehk analüüsimajad kohandavad oma EPS prognoosid majanduskeskkonnaga üldiselt viitega. Kui majandus kasvab oodatust kiiremini, siis nii-öelda hälve väheneb, kuid kui majandus langeb, siis hälve kasvab. Viimase 25 aasta jooksul on keskmiseks EPS kasvuks prognoositud ca 10-12%. Seevastu on McKinsey sõnul tegelik kasv jäänud ca 6% piiridesse.

-

LHV

Kas Läti firmadest ,kus külas käisite on plaanis varsti kirjutada? -

Netflix Stock Going To $180+ As Company Keeps Killing It -- Analyst

http://www.businessinsider.com/netflix-jp-morgan-note-2010-9 -

krookus, juba see nädal saab lugeda :)

-

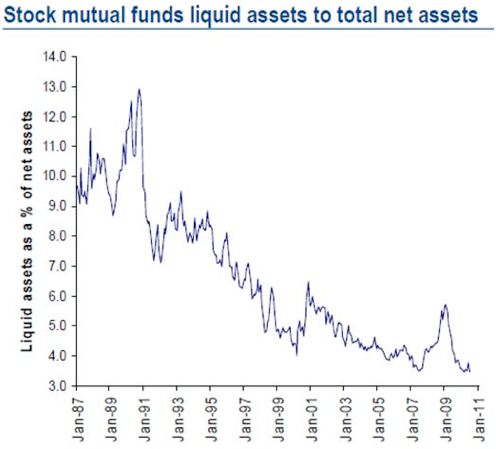

Hea graafik BofA/Merrill Lynch’ilt, mis näitab investeerimisfondide likviidsete varade (ehk vabade vahendite) osakaalu koguvaradest. Käimasoleva aasta juulis oli likviidsete varade osakaal vaid 3.4% - viimati nägime sellist tulemust 2007. aastal ehk ajal, kui turgudel moodustati uusi tippe. Kui investeerimisfondide nii-öelda investeerimistaktikaid üldse indikaatoriks lugeda saab, siis ajalooliselt ei ole tegemist mitte hea signaaliga.

-

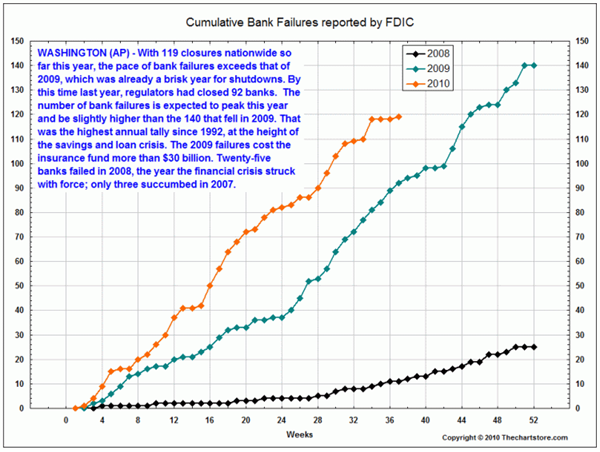

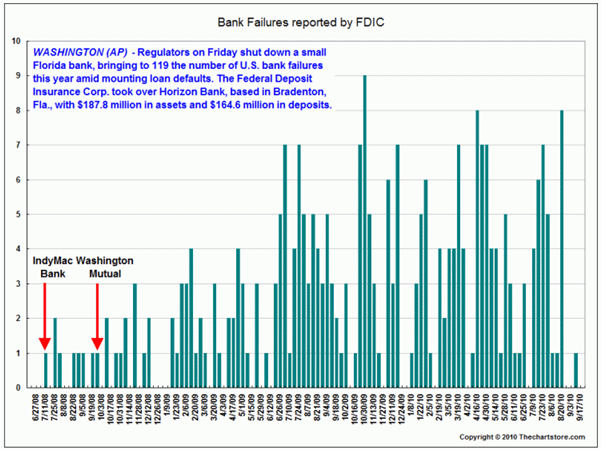

Finantsettevõtete pankrotistumine lõppes 2008. ja 2009. aastaga? Nädalavahetusel avaldas FDIC raporti pankrotistumiste kohta - 2010. aasta on olnud igatahes vägagi tormiline.

August Treasury Budget -$90.5 bln vs. -$95.0 bln Briefing.com consensusKummaga siis tegu on? Finantsettevõtted või konkreetselt pangad? FDIC peaks datat siiski koguma peamiselt pankade kohta.

August Treasury Budget -$90.5 bln vs. -$95.0 bln Briefing.com consensusKummaga siis tegu on? Finantsettevõtted või konkreetselt pangad? FDIC peaks datat siiski koguma peamiselt pankade kohta.momentum, tegu on konkreetselt pankadega. Lisan veel ühe graafiku, mis näitab pankrotistumisi kuupäevade kaupa.

Microsoft jumps on spike in volume; strength attributed to Bloomberg headline that co is planning debt sale to pay dividends and buyback

Microsoft jumps on spike in volume; strength attributed to Bloomberg headline that co is planning debt sale to pay dividends and buyback

MSFT juba +6%Douglas Kass twitteris - reported last week that i had taken a market neutral position - i can report now that i am slightly net short $$

Tutvu tingimustega, konsulteeri asjatundjaga.