Börsipäev 16. september

Kommentaari jätmiseks loo konto või logi sisse

-

.

-

Uus-Meremaa keskpank jättis intressimäära vastavalt ootustele 3% peale. Uus-Meremaa dollar on USA dollari vastu kukkunud ööga 0,9%.

Olulisematest makronäitajatest avaldatakse täna kell 10.15 Šveitsi II kvartali tööstustoodang, kust oodatakse kvartaalses lõikes 6,1% ja aastases lõikes 8,0% kasvu. Kell 15.00 teeb Šveitsi keskpank teatavaks oma intressimäära otsuse ja turgudel eeldatakse, et intressimäär jääb püsima 0,25% peale.

Kell 11.30 ilmuvad Suurbritannia augustikuu jaemüügi tulemused (v.a kütus), mis peaks ootuste kohaselt näitama 0,2% kasvu võrreldes eelmise kuuga ning aastases lõikes 2,8% kasvu.

USAst tulevad kell 15.30 töötuabiraha taotlejate andmed ning esmaste taotlejate puhul oodatakse tõusu eelmise kuu 451 tuhande pealt 458 tuhande peale. Jätkuvate abiraha taotlejate puhul oodatakse marginaalset langust 4,478 miljoni inimese pealt 4,465 miljonini. -

Mäletatavasti olid läinud nädala töötuabiraha taotluste numbrid oodatust selgelt paremad (470000 asemel 451000), kuid seal oli kaks olulist „aga“. Mitmed osariigid jätsid Labour Day tõttu statistika avaldamata ja Tööjõubürool tuli need hinnangute põhjal leida. Teine oluline mõjutaja võis olla koondatud inimeste viitsimatus enne püha töötuabiraha taotlust sisse anda, lükates seda edasi eelmisele nädalale. Seega korralik üllatus võib tulla nii eelmise nädala numbris kui ka sellele eelnenud statistika korrigeerimises. Kui erinevate konsensuste ootused jäävad sinna 460K juurde, siis Briefing prognoosib hoopis langust 440K peale.

-

India keskpank tõstis baasintressimäära 0.25 baaspunkti võrra 6.0% peale, et võidelda jätkuvalt kõrge inflatsiooni vastu.

-

Lisaks makrole, mida Risto välja tõi, jälgitakse USAs veel septembrikuu Philadelphia Fedi indeksit (kl 17.00), mis annab täiendavat infot tööstussektori kohta ning augustikuu tootjahinnaindekseid (kl 15.30). Enne turgu raporteerib esimese kvartali tulemused FedEx, kelle kommentaare globaalse majanduse väljavaate osas tasub kindlasti tähele panna. Aktiivsemalt kaubeldakse tõenäoliselt ka Oracle'i aktsiaga, kes raporteerib oma majandustulemused peale turgu ning omajagu ootusi on nagu näha juba aktsiasse sisse hinnatud.

Oracle

-

Suurbritannia jaemüügi tulemused (v.a kütus) jäid ootustele alla: -0,4% vs oodatud 0,2% (M/M) ja 1,9% vs oodatud 2,8% (Y/Y).

Naelsterling sattus tugeva surve alla: GBP/USD on viimase 15 minutiga kukkunud 0,54% ja paar kaupleb $1,5542 juures. -

Euro rallib hetkel ilma näilise põhjuseta. EUR/USD tõusis 0,4%, jõudes 1,3068 tasemeni. Hetkel kaupleb 10 punkti madalamal.

-

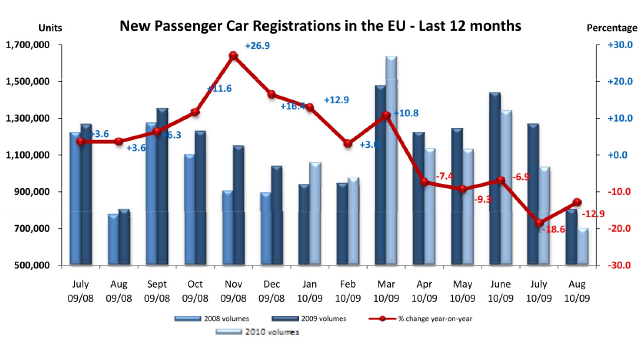

Uute autode registreerimine langes EL-is augustis -12.9% (YoY) 701 710 ühikuni vs juulikuu -18.6% (YoY) langus. Graafik EL-i viimase 12 kuu uute autote registreerimise muutustest European Automobile Manufacturers' Association (ACEA) vahendusel:

-

Euro rallis reaalse põhjuse tõttu.

Spain:

* sells 2723 mln of 10YR bond

* sells 1276 mln of 30YR bond

* 10YR bond bit-to-cover ratio 2.3 (1.88 last auction)

* 30YR b-t-c 2.1 (2.44)

* 10YR average yield 4.144PCT (4.864 pct last auction)

* 30YR 5.077 PCT (5.908) -

momentum, tänud info edastamise eest. Eurotsooni kaubandusbilansi €6,7-miljardiline ülejääk lisab eurole tuge: euro jõudis $1,3083 taseme juurde.

Hooajaline kaubandusbilansi puudujääk jäi oodatust väiksemaks: €0,2 miljardit vs oodatud €0,5 miljardit. -

Headline eksitav, underlying data ei ole tähelepanuväärne.

-

Spain sells 4 bln at bond auctions, yields drop

http://www.forexyard.com/en/news/Spain-sells-4-bln-at-bond-auctions-yields-drop-2010-09-16T093854Z -

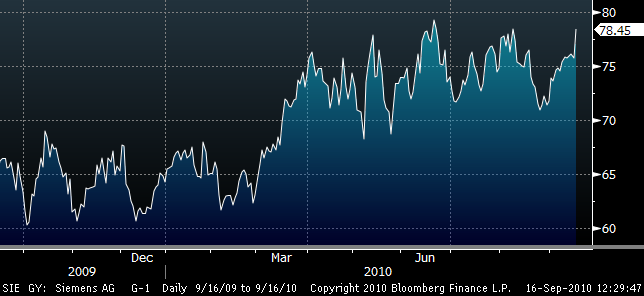

Kui hiljaaegu kergitas UBS Siemensi hinnasiihi 80 eurolt 85 eurole, siis täna toetab aktsiat Morgan Stanley, kelle siht päris Goldmani 126 euroni ei küündi aga 105 eurose prognoosi põhjal korralikku potentsiaali siiski märgib. Peamisteks katalüsaatoriteks peetakse analüütikute päeva, ülekapitaliseerituse tõttu progressiivsemat dividendipoliitikat, NSN-i paremaid marginaale. Morgan Stanley 2010 EPS prognoosi (5,92 EUR) põhjal kaupleb aktsia hetkel 13,2 ja 2011.a prognoosi põhjal (7,37 EUR) 10,6 kordsel PE tasemel.

We upgrade Siemens to Overweight (price target increased from €83 to €105 for 38% upside) ahead of the November analyst day as we believe the group is capable of delivering throughcycle returns of 15-21%, more than double previous rates. At the upper end of the range, this would drive FY13e EPS toward ~€10. Additionally, we see meaningful scope for improvement in the capital structure – and potentially a more progressive approach to the dividend.

-

INSTANT VIEW 3-Euro zone July trade surplus bigger than fcst

http://classic.cnbc.com/id/39208003 -

Danske Equities, a unit of Danske Bank raised its target price on Danisco shares to 540 crowns from 510 and reiterated its "buy" recommendation on the stock. "We regard the company as an obvious takeover target, trading at a major discount to peers," Danske Equities said in a research note ahead of Danisco's first-quarter results due on Sept. 21. "We expect further share re-rating during 2010 due to increased focus on bioscience exposure and the stock's defensive qualities," Danske said. "We believe Danisco is likely to upgrade its long-term EBIT margin target."

-

FedEx misses by $0.01, reports revs in-line; guides Q2 EPS below consensus; raises FY11 EPS to in-line; combines Freight and LTL ops

Kõrgemate lennukite hooldus- ja personalikulude ning FedEx Freight ärikahjumi tõttu jäi FedEx EPSi ootuse osas alla. Lähikuudeks prognoositakse aga tugeva nõudluse jätkumist. CFO: We expect continued strong demand for our package transportation services through at least December. FedExi aktsia kaupleb eelturul -2,9% punases

-

Šveitsi keskpank jättis intressimäära muutmata 0,25% peale. USD/CHF tegi ligi 100-punktise hüppe üles, jõudes tasemeni 1,0114. EUR/CHF rallis 135 punkti, saavutades 1,3230 taseme.

-

Continuing Claims falls to 4.485 mln from 4.569 mln

Initial Claims 450K vs 460K Briefing.com consensus, prior revised to 453K from 451K

August PPI MoM +0.4% vs +0.3% Briefing.com consensus

August Core PPI M/M +0.1% vs +0.1% Briefing.com consensus, prior +0.3% -

rises (??) to 4.485 mln from 4.569 mln?

-

Briefingu väike näpukas, parandasin ära. Esimese hooga ei pandud ilmselt tähele, et varasemaid numbreid revideeriti kõrgemale.

-

Gapping down

In reaction to disappointing earnings/guidance: APOG -4.6%, WMB -3.1%, FDX -2.9%, DBRN -2.7%.

Select financial related names seeing weakness: IRE -2.7%, NMR -2.4%, DB -2.3%, RBS -1.7%, AEG -1.6%, CS -1.5%, ING -1.5%, PUK -1.3%, UBS -1.3%, BAC -1.0%, BCS -0.9%.

Select mining stocks trading lower: RTP -1.7%, BHP -1.2%, MT -1.1%.

Select iron/steel names seeing continued weakness: CENX -1.2%, AKS -1.1%, X -0.8%.

Other news: NPSP -6.2% (announces pricing of public offering of 6.88 mln shares of common stock at $6.00 per share), AEL -6.2% (to offer $150 mln Convertible Senior Notes due 2015), CFN -3.6% (still checking), BWA -1.6% (ticking lower; weakness attributed to tier 1 firm downgrade), INT -1.1% (priced an 8 mln share common stock offering at $25/share), RIG -0.5% (announces proposed senior notes offering; also filed mixed securities shelf offering).

Analyst comments: VOD -1.9% (removed from European Analyst Focus List at JP Morgan), COG -1.3% (downgraded to Sell from Hold at Lazard Capital).

Gapping up

In reaction to strong earnings/guidance: AIR +5.3% (light volume), CLC +2.6%, PIR +2.4%.

M&A news: CLU +42.5% (Cellu Tissue to be acquired by Clearwater Paper for $12.00 per share in cash), DIGA +38.5% (PositiveID presents offer to acquire Digital Angel at 60% Premium), OCNW +7.8% (Occam Networks to be acquired by CALX in a stock and cash transaction valued at ~$171 million, or $7.75 per share), WEL +3.4% (Boots & Coots stockholders Approve Merger with Halliburton).

Select gold/metals related names trading higher: GRS +2.5% (revises cost guidance downward and confirms production guidance at ocampo), NG +2.3%, KGC +2.1%, EGO +1.8%, GSS +1.6%, GG +1.5%, AUY +1.5%, GFI +1.4%, SLW +1.3%, GLD +0.6%.

Other news: AZC +16.9% (Augusta Resource announces minority JV with Korean consortium whereby consortium acquire 20% interest in copper molybdenum project in consideration for funding $176 mln of the project expenses), LLEN +6.3% (commissions special task force to evaluate potential appointments of auditors), NXG +3.0% (ticking higher; intersects highest grade-thickness interval of 3.37 grams per tonne gold and 0.95% copper over 60 metres at its Kemess Underground Project), GME +3.0% (announces $500 mln share & debt repurchase program), INCY +2.3% (ticking higher; announced results from a Phase I/II study of Incyte's JAK inhibitor demonstrated marked and durable clinical benefits in patients with myelofibrosis), F +1.6% (Cramer makes positive comments on MadMoney; also strength attributed to tier 1 firm upgrade).

Analyst comments: SI +2.3% (added to Conviction Buy List at Goldman), MRX +1.9% (upgraded to Buy from Hold at Jefferies; tgt $41), OPEN +1.6% (upgraded to Buy from Neutral at Merriman), NFLX +0.6% (upgraded to Neutral from Under Perform at Credit Suisse).

-

Rev Shark: A Tricky Juncture

09/16/2010 7:54 AMLogic is the art of going wrong with confidence.

--Joseph Wood Krutch

Since the market bottom in March 2009, the most challenging aspect of this environment has been navigating the many V-shaped bouncers and rallies we have seen. Numerous times we have seen long streaks of extremely positive action -- an extended market would become more extended, and then run even more.

What would make these streaks even more difficult was that they would often occur not just on mediocre volume, but on diminishing volume. Furthermore, the market would often cut through key overhead resistance levels as if they didn't even exist. I often commented on how the rules of technical analysis no longer seemed to apply.

Right now we are seeing another streaky V-ish move. The S&P 500 has risen for 10 of the last 11 days, and key stocks such as Apple (AAPL - commentary - Trade Now) have climbed for 12 of the last 13 days. Volume has been less than average the whole way. There have been few technical "accumulation" days, and the major indices have cut through resistance levels fairly easily.

So, the million-dollar question now is whether we are seeing another run like we saw back in March and April 2010 or during 2009. The straight upward move, which was similar to this, continued for weeks longer even though stocks were overbought the entire time and never had any healthy consolidation.

The best traders usually stick with the odds. They don't chase extended stocks or markets, especially if volume is slow and there is resistance looming overhead. However, that turned out to be a very poor strategy from March 2009 through April 2010. The right strategy was simply to buy and hold and ignore any and all negatives. It is rather ironic that buy-and-hold was the way to go, especially after nearly everyone had declared the approach dead in early 2009. But if there is one thing we can count on from the market it is its ability to frustrate as many folks as possible.

We are at that juncture again at which traders must wrestle with believing that an extended market will just keep on running. With each new green day now, there are more market players who start thinking that stocks will have to rest pretty soon. But when we don't, underinvested bulls become frustrated and start to chase, and the bears who keep anticipating a top are squeezed once again.

The low in February 2010 to the high in April 2010 is a particularly good illustration of how a V-shaped move can just keep going and going and run anyone who has doubts. For bulls like Jim Cramer, who are very good at sticking with an uptrend, it can be a fantastic market. But, for traders who look for volatility and expect the normal rules of technical analysis to apply, it can be extremely frustrating.

So, how do we deal with this? The more important thing is to not be overly anticipatory. You have to honor the trend, no matter how extended or ridiculous it may seem, until there is some selling that actually sticks. That doesn't mean you stay fully invested and wildly bullish. You will probably do want to take some gains, but you don't want to be too fast to become negative. Don't go putting on big short positions into strength. The dip buyers can be amazingly tenacious during runs such as what we have seen in the last few days.

We are seeing a little softness again this morning, but the buyers jumped in aggressively the last two mornings when there were similar starts. If this market is going to roll over, this is the place it should do so, but given recent history this isn't that easy of a bet. The bears have been steamrolled numerous times in the past year, and half the time were when the market looked just like this.

Nonetheless, as I mentioned yesterday I'm positioned fairly neutrally -- not because I'm extremely negative, but because discipline has forced me to do a lot of selling and won't allow me to buy extended charts. There was some instability under the surface yesterday that concerned me, and of course some of the blithe bullishness is a troubling sign after the market has gone straight up for a couple weeks.

We'll see what the dip buyers can do with the third soft open in a row, but I believe it won't be as easy to pull off another save. Stay vigilant and flexible as we are at a very tricky juncture.

-

USA futuurid vaatamata oodatust parematele töötuabiraha taotluste numbrile jätkuvalt miinuses. Olulist infot on oodata veel kell 17.00. Hetkel ES -0,38%, YN -0,26%, NQ -0,27%%. Nafta kaupleb -1,1% @ 75,14 USD ja kuld +0,51% @1273,1 USD.

Euroopa turud:

Saksamaa DAX -0,24%

Pantsusmaa CAC 40 -0,51%

Suurbritannia FTSE100 -0,26%

Hispaania IBEX 35 -0,05%

Rootsi OMX 30 -0,29%

Venemaa MICEX -0,20%

Poola WIG -0,27%Aasia turud:

Jaapani Nikkei 225 -0,07%

Hong Kongi Hang Seng -0,16%

Hiina Shanghai A (kodumaine) -1,89%

Hiina Shanghai B (välismaine) -1,95%

Lõuna-Korea Kosdaq -0,14%

Tai Set 50 +0,25%

India Sensex 30 -0,43% -

September Philadelphia Fed -0.7 vs 2.0 Briefing.com consensus, July -7.7

-

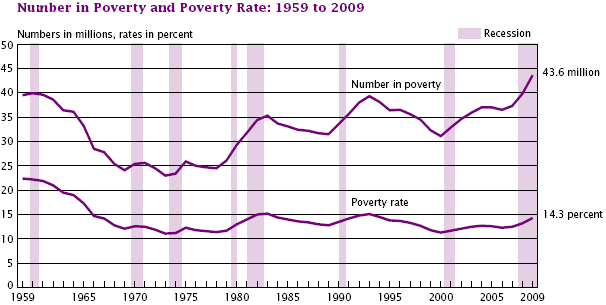

U.S. Census Bureau avalikustas täna raporti, mille kohaselt oli Ühendriikide vaesusmäär 2009. aastal 14.3 protsenti ning vaesuses elas 43.6 miljonit inimest, mis on kõigi aegade suurim arv.

-

Vallo, võiksid lisada, mis on USA-s inimese vaesuses elamise kriteeriumiteks.

-

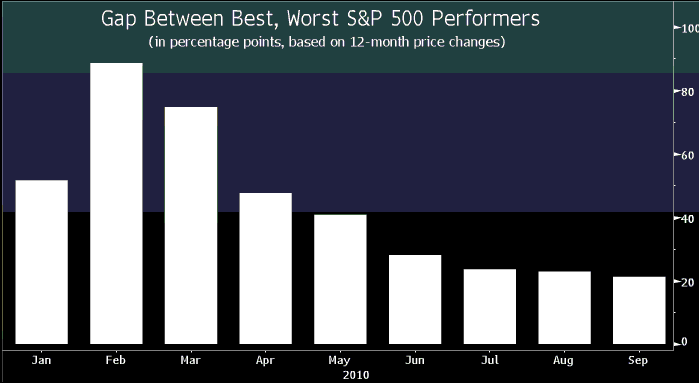

Portfelli mitmekesistamine on turul muutunud üha keerukamaks. Alloleval graafikul on kujutatud S&P 500 indeksis y-o-y baasil parimat ning halvimat tulemust näidanud sektorite vahe protsendipunktides. Ehk möödunud aasta septembrikuuga võrreldes on S&P indeksis parima (ehitusettevõtted, jaemüüjad ja meediaettevõtted) ja halvima tootlusega sektorite vahe olnud ca 20 protsendipunkti. Bloombergi andmetel on tootluse vahe langenud paari kümnendi madalamale tasemele – sektoripõhised panused ei ole enam kuigi atraktiivsed.

-

Eilses börsipäeva foorumis sai pikalt arutatud USD/JPY valuutakursi teemal. Täna kaupleb USD ca 85.7 jeeni peal ehk eilse sulgemishinnaga võrreldes erilist muutust olnud ei ole. Allolev graafik näitab USD/JPY liikumist viimase 11 päeva jooksul.

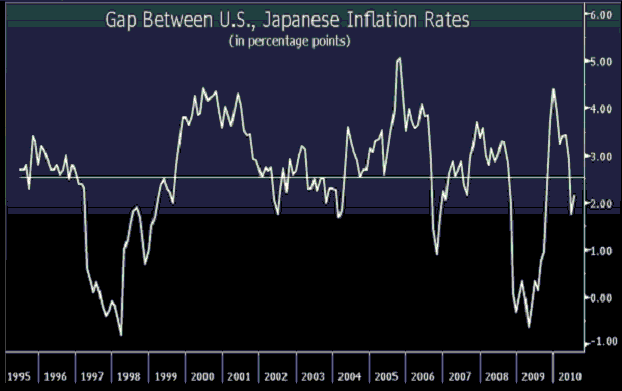

Alloleval graafikul on aga kujutatud USA ja Jaapani inflatsiooni viimase 15 aasta vahe protsendipuntides. USA tarbijahinna inflatsioon on ületanud Jaapani inflatsiooni y-o-y baasil keskmiselt 2.5 protsendipunkti. Inflatsiooniga kohandatuna on nimetatud perioodil jeen dollari suhtes odavnenud ca 32%. Bank of New York Mellon’i sõnul peaks USD/JPY kurss langema 64.35le, et taastada ostujõud, mis oli jeenil 1995. aastal. Ettevõtte analüütikute arvates on deflatsioon Jaapanis endiselt suur risk, mis langetab ka edaspidi USD/JPY kurssi. Olgu öeldud, et Jaapanis on hinnad langenud nüüdseks 18 kuud järjest ning juulis registreeriti tarbijahinna indeksiks 99.2 punkti – tegu on madalaima tulemusega 1993. aastast saati.

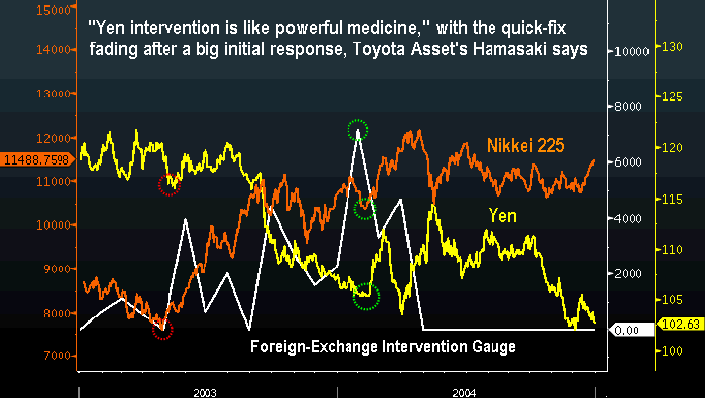

Millist mõju avaldab eilne uudis Jaapani turgudele? Kui heita allolevale graafikule, siis vähemalt mõneks ajaks peaks USD/JPY langus Jaapani turgudele tuge pakkuma.

Oma arvamust on meedias täna avaldanud Toyota Asset Management, kelle arvates Nikkei 225 paari nädala perspektiivis tõuseb, kuid ilmselt järgneb sellele järgneb langus. Viimati müüs BOJ jeeni 2004. aasta 16. märtsil, kui jeen kauples dollari suhtes ca 109 peal. Valuutakursi langus tõi kaasa selle, et Nikkei 225 tõusis 6 nädala jooksul 8.2%. Pärast rallit langes aga indeks 14%.

-

USAs ja maailmas mõõdetakse vaesust mitut moodi. U.S. Census Bureau definitsiooni järgi on inimene vaene, kui ta teenib alla 1000 dollari kuus (pere puhul siis inimese kohta) pärast makse. Arvestades, et USAs on toit odavam, kui Eestis, äärelinnades on majad odavad, bensiin on 7 krooni liiter... mida te vingute? :)

-

Parandus: kui inimene kulutab vähem, kui 1000 dollarit kuus pärast makse.

-

Tõe huvides pean lisama, et Death Valleys oli liiter bensiini üle 10 krooni. Aga seal on "elada" suht raske, seega see ei lähe arvesse.

-

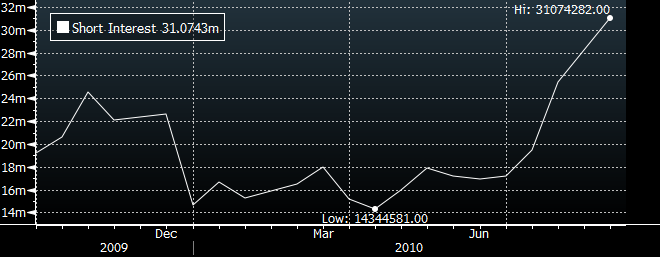

Täna peale aktsiaturgude sulgemist avaldab 2. kvartali majandustulemused Research In Motion (RIMM). Bloombergis kirjutatakse, et RIMM’i „short interest“ tõusis 31. augustil 31.1 miljonile aktsiale, mis on ca 2x enam kui 15. augustil. Konsensus ootab ettevõtte aktsiapõhiseks kasumiks $1.36 ning tuludeks oodatakse $4.48 miljardit.

Ettevõte on selgelt Apple’ile ja Motorola’le turuosa kaotanud. Augustis viisid Sanford C. Bernstein ning JPM läbi küsitluse. 74% vastanutest teatasid, et ettevõte lubab neil kasutada ka teisi „nutitelefone“ peale BlackBerry. Möödunud kuul tegi RIMM algust uue telefoni BlackBerry Torch müümisega. Uudiseid telefoni müügiedu kohta ei ole. Aasta algusest saati on RIMM aktsia langenud ca 34%

-

Homme on optsioonireede - siinkohal oleks oluline märkida, et kuna tegu on aasta üheksanda kuuga, siis maksab üks populaarseid kauplemisinstrumente SPY homse börsipäeva eel oma kvartaalset dividendi. Sedapuhku on selleks $0.58 osaku kohta. Seega kui praegu on SPY 112.80, siis optsioonireede kontekstis on selleks $112.22.

-

Halt traiding Õmblus ja Kundla TV3-es.

-

The Office of Management and Budget defined the poverty threshold level as less than $21,954 for a family of four in 2009 and $10,956 for an individual. The poverty rate increased for all racial groups except Asians.

Census Bureau reports new spike in poverty

http://finance.yahoo.com/news/Census-Bureau-reports-new-cnnm-2077327017.html;_ylt=Akgf3CAUx2r.TDXEkXOz.nS7YWsA;_ylu=X3oDMTE1a2xuazY4BHBvcwMyBHNlYwN0b3BTdG9yaWVzBHNsawNjZW5zdXMxaW43aW4-?x=0&sec=topStories&pos=main&asset=&ccode= -

Oracle prelim $0.42 vs $0.37 Thomson Reuters consensus; revs $7.59 bln vs $7.27 bln Thomson Reuters consensus

-

Hilinenud laul, aga täidame ka selle lünga.

Research in Motion Ltd ( RIMM ) Reports Q2 $1.46 v $1.35e, R$4.62B v $4.5Be

- Guides Q3 $1.62-1.70 v $1.39e, R$5.3-5.55B v $4.8Be -

stockeri poolt öeldule lisan veel niipalju, et RIMM tõusis järelturul 5%.

-

No, kui Q3 ootused on üle latvade, siis ütleks, et vähe. :)