Börsipäev 10. november

Kommentaari jätmiseks loo konto või logi sisse

-

Aasia sessioonil avaldati Hiina oktoobrikuu kaubandusbilanss, mille ülejääk kasvas septembri $16,88 miljardi pealt $27,15 miljardini; oodati $25 miljardilist ülejääki.

Tänastest makroandmetest on Euroopa sessioonil suurima kaaluga Inglismaa keskpanga kvartaalne inflatsiooniraport, mis avaldatakse kell 12.30.

USA sessioonil ilmub USA kaubandusbilanss, mille puudujäägiks oodatakse $45 miljardit. Lisaks avaldatakse esmaste töötuabiraha taotlejate andmed (oodatakse 450K) ja jätkuvate taotlejate andmed (oodatakse 4,3 miljonit). Mõlema puhul oodatakse eelmise nädala suhtes kerget langust.

Euroopa indeksite futuurid kauplevad hetkel punases: FTSE -0,25%, CAC -0,40%, DAX -0,29%.

USA indeksite futuurid hetkel plussis: S&P500 +0,066%, DJIA +0,053% ja NASDAQ +0,126%.

EURUSD on neljapäevasest tipust 1,4280 juurest alla tulnud 3,5% ehk ligi 500 punkti ja asub hetkel 1,3770 juures. -

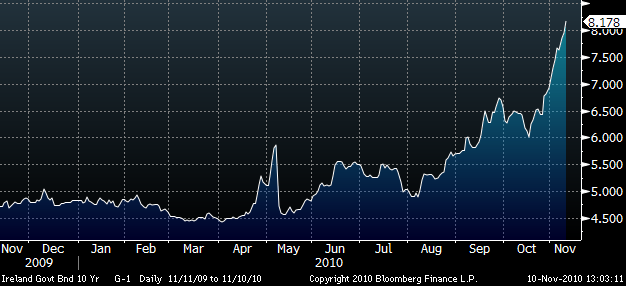

Eilne Kreeka võlakirjaoksjon aitas ajutiselt eurot toetada ning rahustas turgusid. Täna on tähelepanu all Portugal, kes soovib müüa hinnanguliselt 0,75-1,25 miljardi euro eest võlakirju ajal, mil Iirimaa eelarvekärbete arutelu on investorite seas külvanud skepsist ning tõstnud laenukulusid mitte Iirimaa enda, vaid ka teiste Euroopa riikide jaoks. Nii näiteks on Portugali valitsuse 10 aasta pikkuse võlakirja yield teinud viimase kuuga üle 100 baaspunktise hüppe, jõudes 6,7% peale.

-

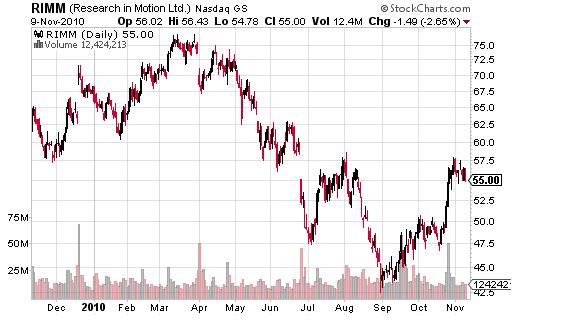

Täna on palju juttu jälle Research In Motion (RIMM)-st ja selle turule tulevast tahvelarvutist PlayBookist.

Bloomberg kirjutab, et RIM hakkab oma PlayBooki müüma järmise aasta esimeses kvartalis hinnaga alla $500. Ettevõte üritab enda toodet eristada iPad-st ja teistest tahvelarvutitest näiteks võimalusega kasutada Adobe Systems`i flash tehnoloogiat, mis toetab enamikku internetis saadaolevat videomaterjali .

Väljaspool USA sihib RIM ühena esimeste seas Lõuna-Korea turgu ja sinna on firma hetkel palkamas inimesi, avamaks juba käesoleva aasta lõpus oma esindus.

Ka Wall Street Journal –st saab täna RIMM-i kohta lugeda ning seal arutatakse võimaluse üle, kas RIM-i tahvelarvuti võiks olla toode, mis muudab kogu mängu. Artikli autor Martin Peers usub, et madalad ootused ja negatiivne keskkond võivad RIMM-i kasuks pöörata ning ehk on nüüd just õige aeg osta ettevõtte aktsiaid.

But perceptions about RIM's technology prowess could change quickly once its PlayBook tablet hits the market next year. The device will use software from QNX, recently acquired by RIM. Eventually QNX software is expected to be used in BlackBerry phones as well.

Gartneri analüütik Ken Dulaney ütleb, et tahvelarvutis kasutatav QNX tarkvara võib saada siiani ühe suurima probleemi lahendajaks ehk siiani on iPhone`i üks eeliseid olnud puutetundliku ekraani kerge ja mugav käsitlemine.

QNX gives RIM a "fresh start" with its operating system, says Gartner analyst Ken Dulaney. The company could use it to solve its biggest problem, the lack of a touch screen interface as easy to use as the iPhone's, he adds. But it has to show it has the engineering expertise to take advantage of the opportunity.

And it needs to do so without too much delay as rivals like Apple continue to forge ahead. So big risks remain. But at 8.9 times fiscal 2012 earnings, the stock may be getting cheap enough to warrant a second look.

Kui RIM nüüd ühtegi viga ei tee, siis võib järgmine aasta olukord üpris huvitavaks kujuneda.

-

Äsja ilmus Inglismaa keskpanga inflatsiooniraport, kus peamise punktina on välja toodud, et prognooside kohaselt jääb THI keskpikas perspektiivis keskpanga sihtmärktaseme 2% juuurde. Naelsterling on hetkel tuge saamas: kiiresti liiguti $1,6048 tasemeni.

-

Portugal not good

-

Portugal müüs siis 556 mln 2016 võlakirju yieldiga 6,15% versus 4,37% augustis, kui nõudlus ületas pakkumist 2,3x vs 2,1 augustis. Lisaks läksid kaubaks 686 mln väärtuses 2020 võlakirjad yieldiga 6,806% vs 6,24% septembris, kuid siin oli bid to cover juba oluliselt kehvem võrreldes eelmisega korraga (2,1 vs 4,9). Euro on tulnud selle peale järsult madalamale ning kaupleb dollari suhtes päeva põhjade juures @ 1,3760

-

Nelli

Kas Android OS ei ole karta? See tuleb üsna jõudsalt turule. Dell lahkub RIMMI telefonidest ja pushib oma töötajatele Dell Venue Pro-d, mida jooksutab Android. -

Iirimaal endal peaks olema piisavalt sularahavaru, et laenamiseta hakkama saada järgmise aasta keskpaigani, kuid intressid on sealgi üsna hirmutavaks muutunud. 10 aastase yield oli eile 7,94%, täna aga jõudnud uue 15a tipuni.

-

Nagu foorumilugejad tähele on pannud, siis juba mõnda aega on meie poolt väärtusliku sisuga abiks olnud Nelli Janson.

Nelli on juba paar aastat LHV Finantsportaali artikleid kirjutanud ning alates eelmisest kuust töötab ta LHV-s analüütikuna. Kogu selle aja ja enne sedagi on Nelli peamiselt tegelenud päevakauplemisega ning üksikaktsiatest ideede otsimisega. Nüüd siis aitab ta ka foorumilugejatele huvitavamaid ettevõtteid puudutavaid sündmusi koju tuua ning tausta selgitada. -

Stocker: Ikka on. Konkurents on kahtlemata tihe ja seetõttu ei tohigi RIM nüüd ühtegi viga teha, et üldse pildile tagasi saada. Sealt edasi saab alles mu arvates vaatama hakata, kui palju kandepinda ettevõtte lootustel oma konkurentsieeliste osas tegelikult on.

-

USD/JPY on tõusnud täna 0,61% ja kaupleb esimest korda alates 11. oktoobrist 82,20 taseme juures.

-

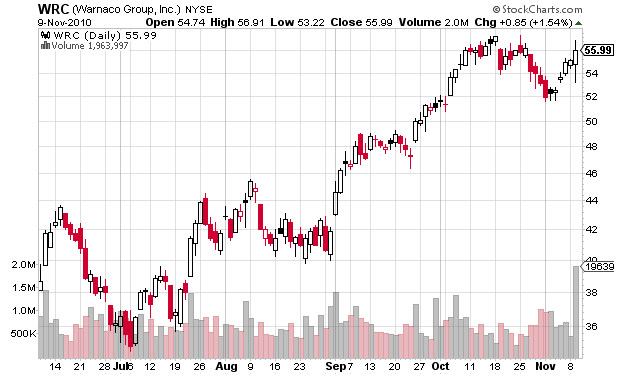

Täna on Merrill Lynchi analüütikud väljas reitingumuutusega USA rõiva-ja jalatsitootjate kohta.

Nimelt peavada nad osade firma väljavaateid üsna negatiivseks ning alandavad V.F. Corporation (VFC), Jones Apparel Group (JNY), Phillips- Van Heusen (PVH), Warnaco Group (WRC) Columbia ja Sportswear Company ( COLM)- reitinguid „osta“ pealt „hoia“ peale.

Alles esmaspäeval kirjutas Financial Times, et luksuskaupade müüjad võivad lootusrikkamalt tulevikku vaadata, kuna tarbijad on taas lahkemalt oma rahakoti raudasid nõus avama ning valmis ostma ka kallihinnalisemat kaupa. Olgu öeldud, et eelpool nimetatud ettevõtete aktsiad on teinud alates septembri algusest läbi ka muljetavaldava ralli.

Kuid Merrill Lynchi analüütikutel on plaan see pidu ära lõpetada ning nende arvates ilmuvad rõivatootjate taevasse tumedamad pilved Hiinast.

China’s tighter manufacturing capacity creates 2011 risks and following our BofAML China Retailing/Sourcing Tour last week, we now believe the challenging apparel sourcing landscape is worse than we thought.

After benefiting from an over-supply landscape the last 20+ years, U.S. apparel importers now face manufacturing capacity issues in China that we believe will continue to drive disruptions throughout the apparel supply chain (including manufacturing, transportation and shipping) through 2011, given: (1) a significantly reduced manufacturing base in China (we estimate by at least 10%) due to cut & sew factory and textile mill closures following the 2008 global recession; (2) a slow pace of new capacity growth in China as smaller garment factories lack gov’t and bank financing support; (3) competition from local demand for capacity as Chinese apparel consumption rises on higher domestic income levels (roughly 50% of the provinces in China have raised local minimum wages by 15-25+% y/y since the beginning of 2010); and (4) less restrictive production guidelines vs. U.S. apparel sourcing companies, which favors factories working with local Chinese players over more compliance focused global brands.

Lühidalt öeldes usuvad analüütikud, et järgmisel aastal seisavad USA rõivaste importijad Hiinas silmitsi mitmete komplikatsioonidega muu hulgas nii tootmise kui ka transpordi osas. Analüütikute veendumus põhineb järgnevatel argumentidel: esiteks väheneb tootmisvõimsus märkimisväärselt ( vähemalt 10%), kuna 2008. Aasta majanduskriisi tõttu suleti mitmeid tehaseid, teiseks on võimsus visa taastuma, kuna paljudel väiksematel tehastel puudub nii valitsuse kui ka pankade finantsiline toetus, kolmandaks tahavad oma osa tootmisvõimusest saada ka kohalikud konkurendid, kuna inimeste sissetulekud on suurenenud ja nõudlus rõivaste järele samuti ja neljandaks soositakse pigem neid ettevõtteid, kes teevad koostööd kohalike Hiina firmadega.

Lisaks sellele on Warnaco Group (WRC) täna see firma, mille suhtes on negatiivsed kaks analüüsimaja. Nimelt annab WRC-le „hoia“ reitingu ka Sterne Agee analüütikud.

Downgrading to NEUTRAL as pressures mounting on GPM in ’11, sales upside now more fully appreciated and valuation surpasses our $55 PT.

Importantly, we believe that much of the sales upside in ’11 is now well conveyed given parameters provided around the CK1 launch, square footage growth assumptions and the justifiably bullish posture of management. We believe that there is an increased likelihood of negative ’11 sell-side earnings revisions in coming months given escalating product costs and the uncertainty of “realized” price increases. While WRC has meaningfully reduced its dependence on the U.S. department store channel (~22%), it is still an exposure (along with retail) where upfront price increases do not necessarily translate into realized price increases due to markdown allowances. WRC is more insulated than most peers to inflationary pressures given evolving business mix (international wholesale 32%, DTC 25%), strong brand (Calvin 75% of business) and changing product, but no company is likely immune to pressures in ’11.Muu hulgas juhivad analüütikud tähelepanu sellele, et WRC on võrreldes oma konkurentidega küll rohkem kaitstud inflatsioonilise surve vastu, aga ükski firma ei ole nende sõnul immuunne turul toimuvate muutuste suhtes.

Usun, et eile õhtul aset leidnud müügisurve saab täna jätku ning turuosalised otsivad võimalusi lühikeseks minna. Kuigi üldjuhul nö grupi reitingumuutused ei oma suurt mõju, siis kaldun arvama, et täna näeb terve sektor teatavat müügisurvet ning WRC võib kuni 3%-4% kukkuda.

Vaatamata Merrill Lynchi kaalukatele argumentidele võib negatiivne mõju täna olla ka oluliselt väiksem tänu Polo Ralph Loren ( RL)-le , sest äsja teatas ettevõte oma kolmanda kvartali tulemused . Numbrid olid üle ootuste ning aktsia kaupleb hetkel 3% kõrgemal. Arvestage sellega ja olge ettevaatlik.

-

Continuing Claims falls to 4.301 mln from 4.387 mln

Initial Claims 435K vs 450K Briefing.com consensus

Prior week initial claims revised to 459K from 457K

September Trade Balance -$44 bln vs -$44.8 bln Briefing.com consensus; August revised to -$46.5 bln from -$46.3 bln -

Gapping down

In reaction to disappointing earnings/guidance: SMT -22.3% (also downgraded to Sector Perform from Outperform at RBC Capital), FEED -16.0%, CAGC -15.1%, AONE -11.0% (also Selected to Develop Battery Pack for New Electric Vehicle from Shanghai Automotive Industry Corporation), SOMX -10.4% (light volume), JMBA -9.5%, CAST -8.7%, TSON -6.2% (thinly traded), SMTX -5.2% (thinly traded), CMFO -4.9%, LOPE -4.6%, HRBN -4.5%, JOBS -4.3%, IDSA -4.3%, AOB -4.3%, SNIC -3.6%, CPB -3.6%, IGT -3.4% (light volume), UEPS -3.3% (light volume), WTW -2.3%, PEGA -1.5%.

Other news: GGP -13.8% (trading post split; emerges from Chapter 11), EGAS -6.9% (trading ex dividend; also Gas Natural prices an underwritten public offering of 2.1 mln shares of its common stock, of which 1.76 mln shares will be sold by co and 340K shares will be sold by certain selling shareholders, at a price of $10.00 per share), IVZ -6.5% (Invesco and Morgan Stanley prices 30.89 mln shares of Invesco's common stock held by an affiliate of Morgan Stanley at $21.48 per share), LOGI -4.1% (pulling back from yesterday's strength following Investor Day), DPM -3.9% (commences an underwritten public offering of 2.5 mln of its common units), EEP -3.3% (announces offering of class A common shares), ELN -3.2% (still checking), HTGC -2.9% (plans to make a public offering of 5,750,000 shares of its common stock), ARCC -1.8% (plans to make a public offering of 10 mln shares of its common stock), BA -1.6% (early weakness after BA 787 emergency landing yesterday and subsequent canceling of flight tests), SAP -1.1% (still checking).

Analyst comments: LVS -1.7% (downgraded to Neutral from Buy at UBS), BEXP -1.7% (downgraded to Outperform from Strong Buy at Raymond James), IHG -1.3% (downgraded to Neutral from Buy at Natixis), DF -1.2% (downgraded to Underperform from Neutral at Credit Suisse).

Gapping up

In reaction to strong earnings/guidance: PCBC +64.1%, PDEX +17.5%, JCS +9.2% (thinly traded), DEG +6.3%, ING +3.8%, DEER +3.8%, MDSO +3.8% (ticking higher), RL +3.5%, PSEC +3.4% (ticking higher), UVE +3.4% (thinly traded; ticking higher), AGM +3.2%, LGND +3.0% (thinly traded), CPST +2.6%, IPAR +2.6%, SVM +2.3%, M +1.0% (light volume).

M&A news: VCGH +16.7% (to be acquired for $2.25 per share in cash in a going-private merger transaction ).

Select financial related names showing strength: IRE +1.7%, RBS +1.1%, PRU +1.1% (increases annual dividend 64% to $1.15 per share; returns dividend to 2007 level ), BCS +1.0%, C +0.8%.

Select metals/mining stocks trading higher: URRE +5.9%, AU +4.5%, HL +4.0%, EXK +3.6%, SLV +3.5%, GSS +2.9%, GFI +2.9%, HMY +2.6%, GBG +2.3%, AUY +2.2%, FRG +2.1%, REE +1.9% (reports second round 2010 gold drilling assays), NXG +1.8%, GRS +1.4%, GDX +1.4%, GOLD +1.2%.

Other news: BNVI +19.8% (says FDA has approved its total clinical development plan for Menerba), XOMA +6.1% (ticking higher; reports positive XOMA 052 results in Inflammatory Eye Disease), ENER +3.9% (ticking higher; strength attributed to tier 1 firm upgrade), BJ +3.5% (ticking higher; strength attributed to article out overnight saying co is seeking advisors for strategic alternatives), NOK +1.5% (Ericsson and Nokia are developing pioneering TD-LTE demonstration devices for China Mobile).

Analyst comments: CAAS +1.9% (upgraded to Accumulate from Neutral at Global Hunter).

-

Rev Shark: Change of Character or Brief Pause?

11/10/2010 8:18 AM"He is most free from danger, who, even when safe, is on his guard."

-- Publilius Syrus

On Tuesday the market suffered its worst day of selling since Oct. 19. It has been over a month since we've had two days of consecutive selling, and we really haven't had any pullbacks of note since the recent run began way back at the end of August.

We were due for some selling, but the question for us to contemplate this morning is whether the selling is the start of a change in market character or just a brief pause before the uptrend continues. Anticipating market weakness has been a very dangerous game, and we don't want to be too bearish until there is clear reason to be more negative. On the other hand, the action yesterday suggested that we tighten up our defenses and be more vigilant. As any trader knows, you can give back some big gains very quickly when the market turns. If you protect gains and don't have to make up losses, you will be far ahead of the game.

The bullish case for this market is very clear. We've had many excellent earnings reports and even some better-than-expected economic news, but the primary driving force is the Fed. Although it is tough to find an economist that believes QE2 is a good idea, the Fed has made it clear that it is intentionally trying to prop up the stock market in hopes that it will create a positive feedback loop. The hope is that consumers will feel good about making money in the stock market, which will lead them to spend more, which will help business and result in further gains for the stock market and so on.

Regardless of whether you agree with the Fed's theory, we would be foolish to disregard the fact that the Fed is providing some major underlying support for the market. The old adage about not fighting the Fed may sound trite but, there are some very good reasons for honoring that saying.

The bears' best argument right now is that, yes, there are positives out there but we have been anticipating and pricing them in for two and a half months now. The good news has been fully discounted, and without further positive catalysts, this market has limited upside. The economy is still struggling, and the Fed is running out of ammunition.

The problem with the bearish arguments is that they are the same ones that the market has been ignoring for over a month now. They haven't mattered to this market and until the price action begins to reflect some pessimism, we can't fully embrace them. At some point, the bears will be right, but the key is to nail the timing. Good theoretic arguments only matter when the market decides that they matter.

Keep in mind that market tops are a process. Even if we are starting to see a change in market character, it is likely that we have some more upside action before a more severe correction sets in. It takes a while to discourage the bulls when they have been doing so well for so long. They aren't going to suddenly change their minds about the market until they have suffered a little bit first.

We have a mild start this morning. Europe is down, and China tightened its banks' reserve rations by a half point. This is the fourth increase this year on concerns that there is too much liquidity in the system.

Some heightened caution is warranted right now, but it is still a bit too early to be bearish. This market has a remarkable record of shrugging off the bouts of selling, and we'll have to wait and see how it handles it this time.

-

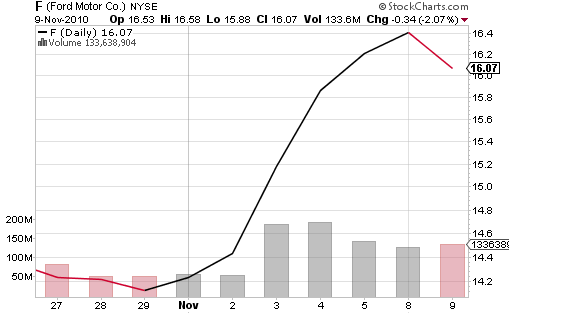

Morgan Stanley analüütikud on täna mängimas mõttega, kas Ford (F) võiks olla $30 aktsia.

Morgan Stanley on kahtlemata ettevõtte suhtes äärmiselt positiivne ja täna leiavad analüütikud, et F aktsia võiks teatavatel tingimustel väärt olla ka $30.

Our $23 base case valuation for Ford has allowed for a number of headwinds we believe the company will face medium term… including declining US market share, severe price pressure and mix deterioration. Our assumptions are also based on declining margins in S. America and rather pedestrian assumptions for growth in other emerging markets, especially in China. Could our base case assumptions prove to be too conservative? Yes, they could. In a modestly more bullish scenario, could Ford’s fundamental operating performance justify a $30 share price? We think yes. Ford shares hit a spin-off and split-adjusted high of $37 in 1999 and $30 in early 2001, albeit during more heady economic times but with far less structural potential to generate free cash flow to equity than it has today.

Conditions for a $30 share price:

• US market share: US market share improving to 19% from 17% currently. Our current target is

based on Ford share falling to 16% long term.

•US SAAR: US sales improving to 14.5m in 2011 and 18m by 2015. We currently assume a US

SAAR of 14m in 2011 and less than 17m by 2015.

•N. American pricing: Pricing no better/no worse than 2010 levels with sustainable NA margins at 7%. We have currently allowed for a $0.5bn drop in pricing in 2011 with a long term NA margin of 6%.

•Emerging markets: S. American margins of 9% and affiliate earnings contribution of $1bn per annum. We currently assume 7.5% S. American margins and less than $0.6bn of affiliate earnings.Analüütikud usuvad, et peagi on tingimused saavutamaks $30-st hinnasihti piisavalt küpsed ja eeldused selleks oleks järgnevad : Firma turuosa USA-s kasvaks 17% pealt 19% peale, müüginumbrid suureneks , hinnad jääks enam- vähem samale tasemele koos jätkusuutliku 7%-lise marginaaliga .

Teatavasti võttis Morgan Stanley F-i 1. novembril oma RTI ( Reasearch Tactical Idea) nimekirja ja tõstis ka hinnasihi $23 peale. Sel päeval kauples aktsia $14,30 kandis ja paraku samal päeval märkimisväärset ostuhuvi ei tekkinud. Samas täna kaupleb aktsia juba $16,30 kandis ehk siis kümne päevaga on aktsia tõusnud ligi 15%.

-

Kreeka ja Saksamaa 10-aastaste võlakirjade tulususte vahe kasvas 900 baaspunktini. EUR/USD üle poole protsendi miinuses ja kaupleb juba allpool 1,3700 taset.

-

Pistke siia Iiri 10y päevasisene ka. Suht kole.

-

Turuosalised ei lasknud ennast täna RL-i tugevatest tulemustest häirida ning on müünud WRC korralikult miinusesse. Nii nagu ma hommikul ka eeldasin on aktsia kukkunud 3,7%-sse miinusesse, kaubeldes hetkel $53,80 kandis.

Avanemisel oli aktsiat võimalik lühikeseks müüa $54,60 kandis, seega oli reaalselt laual $0,70-$0,80 kasumit.

Müügisurve all on ka teised Merrill Lynchi analüütikute poolt nimetatud aktsiad: PHV kaupleb 3,2%, VFC 2,8%, JNY 2,4%, ja COLM 4% miinuses.

-

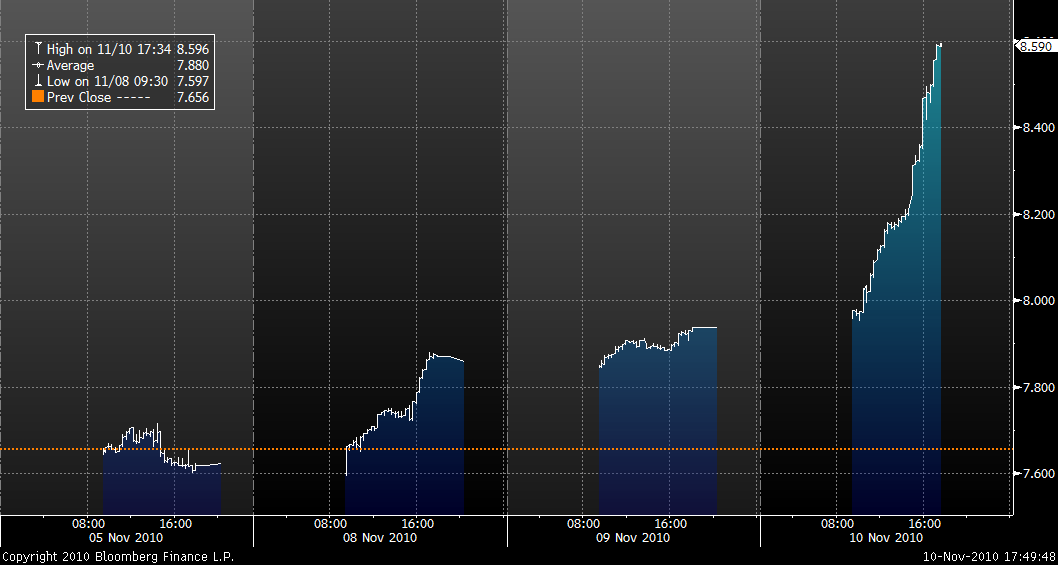

Iirimaa 10-aastase võlakirja tulusus viimase nelja päeva jooksul:

-

--> IE - Ireland

<-- PT - Portugal

--> ES - Spain

<-- IT - Italy

--> GR - Greece -

$16 bln 30-yr Bond Auction Results: 4.320% (Expected 4.288%); Bid/Cover 2.31x (Prior 2.49x, 10-auction avg 2.70x); Indirect Bidders 38.4% (Prior 32.4%, 10-auction avg 35.1%)

-

October Treasury Budget -$140.4 bln vs -$140.0 bln Briefing.com consensus, prior year -$176.4 bln

-

Föderaalreserv ostab järgmise kuu jooksul $105 miljardit väärtuses riiklike võlakirju. Ajavahemikul 12. november kuni 9. detsember toimub 18 OMO (Open Market Operations).

-

AMZN on täna saanud palju kajastust seoses raamatu "The Pedophile`s Guide to Love and Pleasure: a Child-lover`s Code of Conduct" Philip R.Greaves II sulest. Tegemist elektroonilise raamatuga, mida saab Kinle vahendusel lugeda.

Paljud AMZN kliendid on avaldanud arvamust, et juhul, kui raamatut müügilt ei korjata siis kutsutakse inimesi boikoteerima.

AMZN aktsiat selline kajastus ei ole mõjutanud ja ettevõtte aktsia hinnatase testimas aasta tippe. Aasta tipuks $73.20 ja hetkel püsimas $172.80 tasemel. Päeva tipuks $173.08. -

Hommikul tegi Nelli juttu Research In Motion’ist (RIM). Aktsia kaupleb hetkel ca 7% plussis ning sihikule on võetud 200 SMA.

-

Tänast RIMM-i aktsiagraafikut vaadates võib küll vist öelda, et turuosalised pole ettevõtte suhtes veel lootust kaotanud.

-

Cisco Systems prelim $0.42 vs $0.40 Thomson Reuters consensus; revs $10.75 bln vs $10.74 bln Thomson Reuters consensus