Börsipäev 5. jaanuar

Kommentaari jätmiseks loo konto või logi sisse

-

Baltic Morning News

Baltic dairies fighting for raw milk. BBN writes that Baltic countries are on verge of a milk war. Latvian milk farmers prefer to sell milk to Lithuanian dairy companies that pay more than local dairies, while Latvian dairy companies itself are forced to buy milk from Estonia. According to statistics, Latvian milk exports to Lithuania went up 7,000 times in a year last year, and most of the 42,700 tons of exported milk to Lithuania was non-processed raw milk (99.8%). However, the Latvian Prime Minister Aigars Kalvitis is not happy with the situation and he has said that such a policy must be curbed in the "strongest possible way although Lithuania is the neighbour". Of our great interest is how this could affect Pieno´s (Buy) raw milk supplies.

New car sales at record high level. According to Estonian business daily Äripäev, new car sales in Estonia increased 30% to a record high level of 25,230 passenger cars in 2006. The best selling car brand last year was Toyota with 3,529 cars, followed by Volkswagen with 2,141 cars, and Honda with 2,070 new vehicles.

Wages growing faster than productivity. According to Äripäev, the trend of labour costs increasing at a faster rate than productivity also continued in Q3. Productivity (sales per employed person) increased 16% in Q3, while labour costs per employed person went up by 21%.

Number of trades at Tallinn Stock Exchange up 52%. According to Tallinn Stock Exchange (TSE), the number of transactions increased 52% in 2006, while the number of securities accounts registered in Estonian CSD went up by 18%. At the same time, the percentage of private persons trading has increased, as the average size of a transaction has dropped 75% from EUR 47,002 to EUR 12,182. Clearly, investing has become more popular in Estonia.

House prices up 1.6x in a year in Estonia. According to the online real estate portal city24.ee, the average square meter price has gone up 1.58 times in a year for houses sold in Estonia. Currently, the average price per square meter of houses on sale in Estonia is EEK 14,900 (EUR 952), while a year ago the corresponding figure was EEK 9,458 (EUR 604). In Tallinn, the average price for a square meter for houses has gone up less, 51% in a year to EEK 26,132 (EUR 1,670).

Latvians worried about the overheating economy. Yesterday, Latvia's leading economic experts met at the Ministry of Economy to discuss whether the government must intervene to avoid the crash, BBN wrote. The main points discussed were not new: current account deficit at worrying levels (24.2% of GDP in Q3), and economic growth, mainly driven by domestic demand, is not balanced across sectors. Over a half of the 11.8% GDP growth came only from two sectors: trade (+19%) and real estate, renting and business activities (+18.1%). We can add that the same problems apply also to the other Baltic States.

Latvia quadruples fines on jaywalkers and horses. Latvia has long had one of the worst death rates from traffic accidents in Europe. Poor roads, an explosive growth in car ownership and widespread tolerance of drink driving have all contributed to the problem, Playfuls.com wrote. Therefore, Latvian politicians voted on Wednesday to quadruple fines on jaywalkers (pedestrians found out after dark without reflectors) and law-breaking drivers of horse-drawn carriages. Increased fines were also approved for speeding drivers (those with excessively tinted windscreens).

-

Oleme sisenenud kasumihoiatuste hooaega. Eile kommenteerisin natukene Motorolat (MOT) ning järgnev uudis on sellele hea jätk:

MOT Motorola announces preliminary estimates for Q4; lowers Q4 revs below prior guidance; co lowers GAAP EPS guidance

Co announced preliminary estimates of Q4 2006 financial results. Although the co has not finalized its financial results for Q4, sales are now estimated to be in the range of $11.6-11.8 bln (consensus is $11.99 bln), versus the guidance given on October 17, 2006, of $11.8-12.1 bln. Q4 GAAP EPS are now estimated to be in the range of $0.13-0.16, which is below the co's internal forecast at the start of Q4 and may not be comparable to Reuters consensus is $0.38. The estimated EPS range includes estimated net charges, primarily non-cash, of ~$0.10 per share relating to items that are typically highlighted in the co's earnings press releases, including investment-related losses, stock compensation expenses, business reorganization charges and unusual tax expenses. The Q4 will represent MOT's 24th consecutive quarter of positive operating cash flow. -

Eile käis mingi info läbi, et soovitatakse vähendada positisoone Venemaal enne presidendivalimisi.

Vist oli Bear Stearns see ütleja. TRF kukkus eile kah päris kõvasti.

Mida arvata selles valguses Eesti ja kogu Baltikumi kohta?

Et kas Eesti on kaugelt vaadates pigem Venemaa lääneprovints või ehk juba EL idaprovints?

Kas võimalik vähendamissoov Venemaal võib kutsuda vähendama positsioone ka Baltikumis? -

http://www.kauppalehti.fi/4/i/uutiset/etusivu/juttu.jsp?oid=2007/01/05/2196703

Nokia reageerib Motorola kasumihoiatusele.

Nokia -3,5%, OMX Helsinki -1,9%. -

Mis puutub TRF liikumisse, siis ise Beari kommentaari ei ole lugenud. Kuid taolised ägedad liikumised võivad olla ohu märgiks. Fondid on kindlasti oma pikki positsioone viimase poole aasta jooksul suurendanud ning põhjust kasumeid võtta on. TRF liikumine meenutab mais toimunut ning sellele järgnes päris hoogne langus ja seda mitte ainult Venemaal. Ma küll ei usu, et meid Venemaa lääneprovintsiks peetakse kuid suuremad liikumised maailmaturgudel võivad samuti mõju avaldada Baltikumile. Ebalikviidsus on võib olla probleemiks.

Bloomberg.com:

``The difficulties of Motorola today will be difficulties of Nokia tomorrow,'' said Valerie Cazaban, who oversees $127 million at Stratege SA in Paris.

Nokia dropped 3.6 percent to 15.34 euros. Credit Suisse Group downgraded shares of the world's largest mobile-phone maker to ``neutral'' from ``outperform.'' The analysts cited their expectations for a ``weak'' fourth quarter and gross margin pressure as they cut their price estimate for the stock to 16 euros from 19 euros.

Ericsson fell 1.1 percent to 28.4 Swedish kronor.

-

Soovitan vaadata ka kahel viimasel päeval toimunud iShares FTSE/Xinhua China 25 Index (FXI) liikumisi. Kahel viimasel päeval on käive olnud märkimisväärne ning graafik hakkab meenutama hype-aktsia liikumist.

-

D.A. Davidson raises their Broadcom (BRCM 33.57) tgt to $35 from $31, as they believe the inventory issue is behind the co and

feel comfortable with their 2007 revenue growth estimate of 10.8% y/y

Stifel Nicolaus downgrades Gap (GPS 19.44) to Hold from Buy with a $26 tgt, based on failed efforts to improve the offerings

sufficiently to stem the decline of sales and traffic at both the Old Navy and Gap divisions

Deutsche Bank downgrades Motorola (MOT 20.55) to Hold from Buy and lowers their tgt to $22 from $30, given concerns that

slowing growth in mobiles, a shift in volumes to low-priced models and reinvigorated competition will force the co to choose

between market share and pricing in coming quarters

Piper Jaffray downgrades Motorola (MOT 20.55) to Market Perform from Outperform and lowers their tgt to $20 from $27,

following disappointing preliminary Q406 earnings and sales guidance and believe it could take several quarters for MOT's

handset operating margins to recover

CIBC downgrades Motorola (MOT 20.55) to Sector Performer from Outperformer, based on disappointing Q406 sales

guidance and margin concerns

Credit Suisse downgrades Nokia (NOK 20.92) to Neutral from Outperform

Prudential downgrades the E&P sector to Neutral from Favorable, based on expectations for lower natural gas prices resulting

from a likely second consecutive warmer-than-normal winter season

Prudential downgrades Chesapeake Energy (CHK 27.72) to Neutral from Overweight and lowers their tgt to $36 from $38,

based on lower natural gas prices

UBS initiates Flextronics (FLEX 11.53) with a Buy

JP Morgan downgrades Dell (DELL 26.24) to Underweight from Neutral, as they believe gross margins may disappoint in the

coming quarters

Lehman downgrades Exxon (XOM 72.72) to Equal Weight from Overweight

Goldman downgrades Aetna (AET 42.12) to Neutral from Buy

Merrill upgrades Abercrombie & Fitch (ANF 73.13) to Buy from Neutral

Goldman resumes coverage of Pfizer (PFE 26.38) with a Buy

J.P Morgan adds Divx (DIVX 23.24) to their Focus List -

Futuurid (ka nafta) kauplevad tublis miinses ning põhjuseks probleemid tehnoloogiasektoris, alustatuna Motorolast. ASP langus on piisavalt suur probleem, mis mõjutab ka marginaale. Siit saavad kindlasti kannatada pikemas perspektiivis komponentide tootjad ja pooljuhtide osas on siin negatiivseid mõtteid võimalik palju mõlgutada. 2007. aasta on alanud volatiilselt nii USAs kui teistel suurematel turgudel ning tõenäoliselt saab volatiilsust olema keskmisest rohkem ka edaspidi:

MOT Motorola downgraded to Peer Perform from Outperform at Bear Stearns

Motorola downgraded to Neutral from Buy at Oppenheimer

BRCM Broadcom downgraded to Underperform at Credit Suisse- tgt $26Credit Suisse downgrades BRCM to Underperform from Neutral with a $26 tgt saying the recent run-up in the stock embeds revenue growth of 25%-30% in both '07 and '08 on 2x the market multiple. However, the firm believes '07 will represent a temporary product cycle lull for BRCM and weigh on rev growth (closer to 9%- 15%). They believe the revenue lull will cause a reset in valuation and cause the stock to underperform the broader semi group over the next 6--12 months.

EBAY eBay: Reducing outlook on lower than expected listings growth & conversion trends - CIBCCIBC believes the '07 consensus rev growth of 21% is too high despite benefits of a weaker dollar. They are looking for 19-20% top line growth in '07 and are lowering their EPS by $0.01 each in 4Q06 and FY07 accordingly. Firm expects further deceleration in listings growth with continued weakness in conversion rates. They believe EBAY faces increasing competitive pressure from e-commerce and search, resulting in higher cross-shopping and lower conversions.

Credit Suisse downgraded NOK to Neutral from Outperform saying Q4 is expected to be weak, with continued ASP and gross margin pressure. They expect continued strength in Nokia handset volumes and believe that mix has continued to deteriorate with ULCH volumes rising to 50% of the total units sold. The firm concludes that such an adverse mix will pressurise ASP's and gross margins further. They also fear that recent commentary from suppliers suggests that the networking business is having a weak quarter as customers postpone investments ahead of the potential merger with Siemens

Soros spree 'targets' discount chains. NY Post reports hedge fund titan George Soros is now focusing his multi-billion-dollar portfolio on positions in the retail sector, where he has made bets on some household names. According to hedge fund Web site Stockpickr.com, Soros Fund Mgmt is dipping its toes in the retail waters, taking out new positions in J.C. Penney (JCP), Kohl's (KSS) and Target (TGT). Not known for devotion to a specific investment style, Soros' foray into the shares of mass retailers is probably more opportunistic than anything, said Stockpickr chief James Altucher. "Many of these companies are very cheap. [Penney,] for instance, is just trading for eight times free cash flow," Altucher said. "It's potentially a buyout candidate, along with many of the other stocks Soros is buying." Soros is not wagering too much of his estimated $8.5 bln fortune on retailers. His fund bought 276,600 shares of J.C. Penney, 302,500 of Kohl's and 326,100 in Target. The bet on Target places him in especially good co - alongside the likes of Berkshire Hathaway's Buffett.

-

Stocks to watch:

- Apollo Investment (AINV) said it plans to make a public offering of 16 million shares of its common stock. The New York-based company expects to use the net proceeds of the offering to pay down debt, to fund investments in portfolio companies and for general corporate purposes.

- Arrow International (ARRO) reported fiscal first-quarter net earnings of $14.5 million, or 32 cents a share, up from $11.8 million, or 26 cents a share, in the year-ago period. Revenue rose to $122.9 million from $113.6 million. Analysts polled by Thomson First Call had expected the Reading, Pa.-based medical supply company to post a per-share profit of 34 cents on revenue of $125 million. For the fiscal 2007, the company is still targeting earnings in the range of $1.40 to $1.48 a share on revenue of $515 million to $525 million.

- Axa SA (AXA) said it has agreed to sell Winterthur's U.S. property and casualty business to Australia's QBE Insurance Group for $1.8 billion, a culmination of a strategic review of the unit that the French insurer began in June.

- BJ's Wholesale Club (BJS) slashed its fiscal fourth-quarter earnings forecast and announced it will close its two ProFoods Restaurant Supply locations and 46 in-club pharmacies.

- Denny's (DENN) said that December sales at stores open at least one year rose 1%. The Spartanburg, S.C.-based restaurant chain also said that the guest check average rose 2.2% during the five-week period ended Dec. 27, while guest counts fell 1.2

- Dollar Tree Stores (DLTR) said that its fourth-quarter sales are trending towards the upper end of its previous forecast of $1.28 billion to $1.31 billion.

- Electro Scientific Industries (ESIO) reported second-quarter net earnings of $3.79 million, or 13 cents a share, compared with $3.19 million, or 11 cents a share, during the year-ago period. The Portland, Ore.-based provider of manufacturing systems to the electronics market posted revenue of $59.3 million vs. $48.6 million. Analysts polled by Thomson First Call had forecast second-quarter earnings of 16 cents a share on revenue of $59 million. Additionally, the company said it expects third-quarter shipments and revenue of $55 million to $65 million, and a gross margin increase of 2 to 3 percentage points from the second quarter.

- FormFactor (FORM) President Joseph Bronson has decided to leave the company, effective Friday, to pursue other interests. Bronson also resigned from the board, the Livermore, Calif.-based of semiconductor component maker said.

Moody's Investors Service placed the long-term ratings of Gap (GPS) on review for possible downgrade following the retailer's downward revision of full-year earnings and its holiday sales announcement. - Genentech (DNA) reported "encouraging" results from a Phase II study comparing pertuzumab plus gemcitabine to gemcitabine alone in women with platinum-resistant ovarian, primary peritoneal, or fallopian tube cancer. The study enrolled and treated 130 women, and no new or unexpected safety signals were observed, Genentech said. Data from the study will be submitted for presentation at an upcoming medical meeting, the South San Francisco, Calif.-based biotech company said.

- Healthways (HWAY) said that first-quarter net income nearly doubled to $11.8 million, or 32 cents a share, up from the $6.46 million, or 18 cents a share, posted a year ago. Sales were $117.1 million vs. the $90.6 million for fiscal 2006's first quarter. While earnings were in line with forecasts from analysts polled by Thomson First Call, sales fell short of targets by nearly $4 million. The company reaffirmed its forecast of earnings of $1.44 to $1.61 a share for fiscal 2007 on sales of $667 million to $701 million, both in line with First Call estimates. The company said it expects to earn 29 cents to 30 cents a share in the second quarter, while the First Call estimate is for 34 cents. Shares ended the day down 26 cents to $45.74.

- Herbalife (HLF) forecast fourth-quarter 2006 sales of $482.7 million to $484.7 million, and said it still sees earnings in the range of 52 cents to 55 cents a share, excluding expenses associated with its realignment. For full-year 2007, the company reaffirmed its earnings forecast of $2.40 to $2.47 a share, excluding items. For the first-quarter of 2007, the Los Angeles-based herbal supplement maker forecast earnings of 50 cents to 55 cents a share on sales growth of 6% to 10%.

- Laidlaw International (LI) posted a first-quarter profit of $40.1 million, or 50 cents a share, down from $58.3 million, or 58 cents a share, from a year ago, due to lower passenger traffic as a result of price increases. Revenue at the bus operator rose to $858.1 million from $846.8 million, with Greyhound sales falling $25 million from a year earlier. Analysts polled by Thomson First Call had expected a profit of 57 cents a share on sales of $866.3 million.

- Longs Drug Stores (LDG) said preliminary revenue for December was $567.3 million, up 7.2% from $529.4 million during the year-ago period. The Walnut Creek, Calif.-based company said preliminary total retail drug store sales for the month were $539.5 million, up 2.7% from $525.5 million a year ago. Retail drug store same-store sales rose 1% from the prior year, while pharmacy same-store sales increased 2.3%, and front-end same-store sales increased 0.1%, the company said

- Micrel (MCRL) cut its outlook for its fiscal fourth quarter ended Dec. 31. Micrel now expects fourth-quarter earnings of 9 cents to 10 cents a share on revenue of $64 million to $65 million. The San Jose, Calif.-based chipmaker had previously forecast earnings of 11 cents to 13 cents a share on revenue of $67 million to $70.5 million. The company said the revenue shortfall is primarily a result of weakness in demand during the last two weeks of December across its end markets. Micrel added that it expects first quarter 2007 revenue to increase sequentially from the fourth quarter of 2006.

- Millennium Pharmaceuticals (MLNM) said it expects a 2007 net loss in the range of $60 million to $90 million. On a pro forma basis, the Cambridge, Mass.-based company said it sees earnings of $10 million to $20 million for the year. Millennium also said it sees net product sales of Velcade in the United States of $240 million to $260 million in 2007, and royalties in the range of $140 million to $150 million for the year.

- Motorola (MOT) lowered its earnings and sales guidance for the fourth quarter, citing an unfavorable geographical and product mix of mobile-phone sales that hurt margins and average selling prices.

- Openwave Systems (OPWV) said it expects a second-quarter per-share loss of 24 cents, or a loss of 8 cents to 9 cents on a pro forma basis, on revenue of $83 million to $84 million. The pro forma loss outlook excludes stock-based compensation expense of 8 cents a share, amortization of acquisition-related costs of 6 cents a share, and restructuring and other expenses of 2 cents a share. The Redwood City, Calif.-based software company also said it has authorized a $100 million share buyback program, scheduled to begin later this month. Additionally, Openwave said it expects third-quarter pro forma earnings to be breakeven on a per-share basis, on revenue of $85 million to $90 million. For the fourth quarter, the company said it expects pro forma earnings to increase slightly from the prior quarter on revenue of revenue of $90 million to $95 million.

- Redback Networks (RBAK) forecast lower-than-expected revenue of roughly $64 million for fourth-quarter ended Dec. 31. "Unfortunately we failed to meet our revenue targets due to, among other reasons, distribution channel disruptions caused by the timing of our proposed acquisition by Ericsson, and lower-than-expected revenue from our older SMS product line as we transitioned our largest SMS customers in the fourth quarter to our SmartEdge products," said Kevin DeNuccio, president and chief executive, in a statement. "We expect that substantially all of the delayed purchases will become revenue in 2007."

- RightNow Technologies (RNOW) said it expects fourth-quarter results to come in below its previous outlook. The Bozeman, Mont.-based company had previously forecast results in a range of a net loss of 2 cents a share to breakeven. RightNow also said it expects fourth-quarter revenue of $28 million.

- Saba Software (SABA) reported a second-quarter net loss of $1.01 million, or 4 cents a share. During the same period a year ago, the Redwood Shores, Calif.-based company posted net earnings of $131,000, or a penny a share. Pro forma earnings were $2 million, or 7 cents a share, compared with $694,000, or 4 cents a share, a year ago. Saba reported revenue of $26.2 million vs. $16.2 million. Analysts polled by Thomson First Call had forecast second-quarter earnings of 6 cents a share on revenue of $25 million. Additionally, Saba said it expects third-quarter per-share results to range from breakeven to a profit of 3 cents on revenue of $26.5 million to $27.5 million. On a pro forma basis, the company said it sees earnings of 7 cents to 10 cents a share for the quarter.

- Syms (SYM) reported third-quarter net earnings of $2 million, or 14 cents per basic share, compared with $1.18 million, or 8 cents per basic share, during the same period a year ago. The Secaucus, N.J.-based retailer posted revenue of $72.8 million vs. $74.7 million. Same-store sales fell 1.5% during the quarter, the company said.

- UAP Holding (UAPH) reported a fiscal third-quarter net loss of $13.2 million, or 26 cents a share, compared with a net loss of $9.35 million, or 19 cents a share, in the year-ago period. Revenue at the Greely, Colo.-based distributor of agricultural and non-crop inputs rose 16% to $375.7 million from $323.1 million. UAP revised its fiscal 2007 earnings forecast to a range of $1.15 to $1.25 a share, excluding charges related to the refinancing of debt.

- Xyratex (XRTX) reported fourth-quarter net earnings of $9.35 million, or 32 cents a share, down 32% from $13.8 million, or 48 cents a share, during the same period a year ago. Earnings from continuing operations were $10.9 million, or 36 cents a share. The U.K. maker of data storage equipment posted revenue of $241.1 million vs. $203.6 million. Analysts polled by Thomson First Call had forecast fourth-quarter earnings of 30 cents a share on revenue of $225 million. The gross profit margin was 17.4%, compared with 21.7% a year ago. Additionally, Xyratex said it expects first-quarter per-share earnings of 16 cents to 26 cents, or 23 cents to 33 cents on a pro forma basis, on revenue of $220 million to $235 million.

Market Summary- Asian trading closed with the Hang Seng +0.93%, Sensex -0.08% and Taiwan -1.25%, Shanghai -2.74%, Jakarta +0.46% and Nikkei -1.51%.

-

Average Workweek 33.9 vs 33.9 consensus

Hourly Earnings m/m +0.5% vs +0.3% consensus

Unemployment Rate 4.5% vs 4.5% consensus

Nonfarm Payrolls 167K vs 115K consensus, 100K Bloomberg consensus

Tunnipalga oodatust suurem tõus võib jutu viia taas inflatsioonile. -

mis antud juhul tähendab vist lihtsalt pausi pikenemist

-

Hourly Earnings tõus viitab unit labor cost suurenemisele, mis ettevõtete marginaalidele võib halvasti mõjuda...

Võimalik, et olen natuke paranoiline, kuid arvestades viimase aja korrigeerimis ja vigu majandusandmetes (nagu ka viimase GDP kasvu puhul), tundub, et mõne aja pärast korrigeeritakse seda numbrit kas kõvasti alla või üles (novembrikuine nonf. payroll tõsteti 154K peale originaalsest 132K näitajast). Kuuldavasti on ka soe ilm tõstnud tänahommikust ehitustöödega seotud hõivatust (25-30K) ning külmemate ilmadega peaks see järgnetavel kuudel taas langema. -

Aon prognoosib kindlustusele raskeid aegu.

While the cost of property coverage in peak hurricane zones like the U.S. Gulf Coast continues to rise, premiums charged for the vast majority of other lines of coverage -- like personal injuries or workers compensation -- have dropped over the past year and will likely continue to fall in 2007, according to global insurance brokerage Aon Corp.

The price of primary airline coverage, for instance, has fallen up to 20% and property coverage outside the U.S. is down 10% to 15%, Aon said. -

Eilsed jaemüüginumbrid toetavad mitmeid retailereid. American Eagle Outfitters (AEOS) on murdnud läbi väikse volatiilsusega külgsuunalisest kanalist tugeva käibega. Mitu kuud maadeldi 20 päeva libiseva keskmisega ning testiti 50 päeva MAd. Kuigi MACD on selgelt vastassuunalises liikumises, on tehtud crossover ning ka MACD histogramm on tugevalt positiivne. Olid ju AEOSi võrreldavate poodide detsembri müügitulemused 13 protsenti paremad kui 2005. aastal.

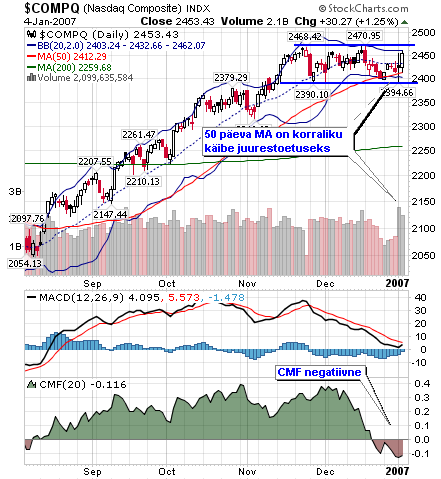

Indeksite volatiilsus on kokku kuivanud ning jätkuvalt viibitakse üsna kitsas kauplemisvahemikus. Näeme, et 50 päeva libisev keskmine on pakkunud Nasdaqle toetust. Kuna tänahommikused futuurid on miinuses, siis ilmselt jääb MACD'l ka seekord crossover tegemata.

DJIA graafikul näeme, et käive enam tõusu ei toeta ning CMF on muutumas negatiivseks. See ei ole kaugeltki hea märk. Ka MACD on juba pikemat aega liikunud indeksiga vastassuunas. Siiski ollakse üsna tublilt bollingeri positiivse poolepeal ehk ülalpool 20 päeva libisevat keskmist. Selle murdmisel ootaksin nagu Nasdaq puhul esimest toetus 50 päeva MA juures.

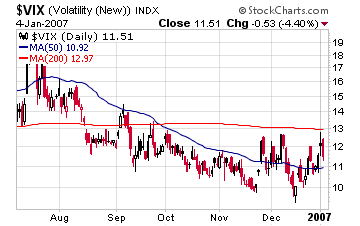

Volatiilsusindeks VIX on tasapisi tõusnud ning on 12 punkti all. 200 päeva libisev keskmine pole kaugel, 12,97 punkti juures.

-

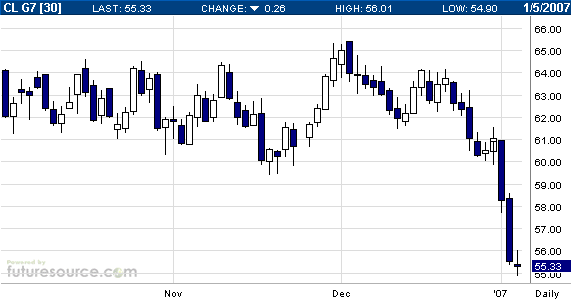

... ja toornafta teeb selliseid kukkumisi:

-

Oliveri mõtted huvitavad. Seda enam, et 3. jaanuaril pärast börsi sulgemist ilmus TheStreet.com'is artikkel FOMC-i poliitika arutelude kohta, mille üks osa sobib ka siia. Nimelt on küsitav, et ega 3. kvartali SKP lõplik näit (mida niigi alandati algsega võrreldes) polnud ikkagi ülepakutud. Sellise stsenaariumi korral esitataks 4. kvartali SKP näit jälle oodatust väiksem.

Täpsem selgitus artiklist selline:

Buried on page three, meanwhile, was an overlooked gem of insight, says Joe Brusuelas, chief economist at IDEAglobal. The FOMC discusses "measurement issues" of automobile output, adding that these issues "likely caused an overstatement of the rate of increase in real GDP in the third quarter, and the gradual unwinding of those effects would probably lead to an understatement of real GDP growth over the next several quarters."

"If this is true, this is enormous," says Brusuelas. "This is the kind of stuff you seen in the green book," the Fed's insider version of the so-called beige book report on economic activity, which is published between FOMC meetings.

Translation: To account for the overstated GDP in the third quarter (and most likely the fourth too, according to Brusuelas), headline GDP for the coming quarters will look lower than they really are. -

Ülespoole avanevad:

CPSL +12% (momentum name, bounces after 20% drop in 2 days), HIHO +7.3% (bounces after 12% drop yesterday), MAMA +6% (extends yesterday's 9.1% move), RBN +4.2% (reports NovQ, beats by $0.08), CC +3.8% (reports Dec same store sales, raises revenue guidance), STEM +3.5% (extends yesterday's 17% move), BBY +3.8% (reports strong Dec same store sales, raises prior guidance), TASR +3.5% (announces it will launch new product on Monday), AZZ +3.3% (reports Q3), DIVX +2.8% (JP Morgan adds to Focus List), MEDI +2.8% (profiled in BWeek Inside Wall St section), APKT +2.7% (profiled in IBD), BRLC +2.2% (Brean Murray raises tgt to $18), SHPGY +1.9%, QGEN +1.8% (Credit Suisse upgrade), NYX +1.3% (Cramer names it as his top growth pick for 2007).

Allapoole avanevad:

Gapping down on disappointing guidance: MOT -12% (also multiple downgrades; down in sympathy: RFMD -4.2%, SWKS -3.8%, TXN -1.9%), MTXX -12%, RNOW -8.7%, OPWV -4.5% (also Jefferies downgrade), SPSN -5.3%, LPNT -4.2%... Other news: GPN -7% (reports NovQ), ESIO -5.7% (reports NovQ, misses by $0.03),NOK -5.1% (Credit Suisse downgrade, also in sympathy with MOT), AEM -4.1% (extends recent weakness, stock down 14% in 2 days), AUY -4% (extends recent weakness, stock down 13% in 2 days), MRVL -2.3% (co says stock option review finds incorrect dates; also Credit Suisse downgrade), DELL -2.2% (JP Morgan downgrade), BRCM -1.8% (finds misdated options; also Credit Suisse downgrade), GLD -1.7% (weak gold prices), INTC -1.4% (Credit Suisse downgrade to Underperform)... Large cap Chinese stocks continue yesterday's sell-off: LFC -4.7%, ACH -3.7%... Under $3: BPOM -14% (Nasdaq declines request for contiuned listing). -

Maagaasivarud vähenesid -46bcfi vs keskmiselt oodatud -61 bcfi.

-

Joel, mida arvad CHK-st hetke tasemetel ? Tean, et Sul on see ettevõtte pikka aega radaril olnud ning CHK tegemisi on ka siin foorumites kajastatud. Hetkel tundub üpriski huvitav hetk sisenemiseks, sest langus on olnud tavatult järsk ning $27-28 kandis on olnud ajalooliselt tugev toetustase. Ise taastasin täna positsiooni.

-

JRCC

-15%

Kommentaarid? -

Kogu energiasektor saab tappa.

-

Pisut mõtteid Chesapeake'ist(CHK)

Viimase aja kiire kukkumine on tulnud suuresti USA soojemast senisest talvest kui oodatud (nagu ühes teises foorumis siin ka mainiti tasub North-East USA piirkonna ilmal eriti silma peal hoida, sest seal just suurim küttepiirkond)... Ja seda teist aastat järjest, mis on gaasivarusid oluliselt suurendanud, pannes gaasi ja kivisöe ettevõtted keerulisse olukorda (märkus. gaasi tarbimise koha pealt on tähtis eelkõige külm talv, sest kütmine käib suuresti eramajades gaasi pealt; suvel on elektritarbimine küll suur seoses konditsioneeridega, kuid ca 50% elektri tootmisest tuleb kivisöe pealt)

CHK vähendas selle aasta sügisel pisut oma ettemüüdud gaasi kogust, et ennast gaasihindade võimalikule tõusule avatumaks muuta, kuna ettevõtte sünoptikute meeskond prognoosis, et selle aasta talv tuleb normaalne või normaalsest pisut külmem. Sellega tõsteti ka ettevõtte kasumile avanevat riski gaasihindade languse korral, kuid minu arust täiesti mõistlikkuse piires. Ehk teiste sõnadega, jätkuvalt on tegu ettevõttega, mis on hästi kaitstud hindade languse eest ja seda nii 2007, 2008 ja osaliselt ka 2009. aastal.

Negatiivne meelestatus turul energia vastu tervikuna aktsiahinna liikumist ülespoole seni toetanud pole. Samas, viimastel päevadel on lõpuks ka mitmed analüütikud nii tervet sektorit kui ka CHK-d ennast downgrade'inud (neutraalse peale) ning varasem hiigelpositiivsus on asendumas konservatiivsema lähenemisega erinevate analüütikute poolt. See aga aitab kaasa suurendamaks potentsiaali ülespoole liikumiseks - kui kõik oleks positiivsed, poleks ju kedagi enam varsti ostmas.

Ise julgeks praeguse langusega tõmmata paralleele 2006. aasta veebruari langusega, mil hoolimata veebruari lõpu külmadest ilmadest jõudis investoritele kohale arusaam, et talv jääb liiga soojaks. Sedapuhku tundub sarnane arusaam juba praegu turul kohal olevat, kuid võrreldes eelmise aasta veebruariga, mil kevad ukse taga, on praegu veel aega n-ö üllatuskülmadeks.

Kuigi energiasektoris ennustuste tegemine on ka pikas perspektiivis tänamatu töö (näiteks nafta hinna aastalõpu prognoose leidub nii $40st kuni $100ni:)), usun pigem, et praegustel tasemetelt on CHK puhul tegu hea ostuga. Kogemustega juhtkond, suur osa toodangust müüdud ette mitme aasta peale kõrgete hindadega ning laiaulatusliku varude juurdeostuplaani lõpetamine eelmisel kvartalil on see, mis mu nägemust toetavad.

Kõige suuremaks probleemiks siis jätkuvalt kõrged varud, mis võivad lõpuks sundida ettevõtteid tootmist vähendama, kuid kui hind peaks jääma praeguste tasemete juurde, ootaks praeguse meelestatuse juures kindlasti ka tulemustejärgselt üllatust ülespoole. -

JRCC languse taga nende eile õhtul sisse antud 8-K, mis puudutab ettevõtte Bell County tegevuse müümist, mis esialgse kokkuleppe järgi pidi müüki minema $24.4 miljoniga. Nüüdseks anti aga teada, et lõplik tehingu lõpuleviimine lükkub edasi ja uueks tähtajaks pandi 30. jaanuar(üks võimalikke põhjuseid, et ostja tahab hinna üle vaielda). Samas on JRCC'l pooleli krediidilepingu tingimuste muutmine, mille üheks punktiks on see, et 28. veebruariks peab ettevõtte likviidsus olema vähemalt $20 miljonit. Ja selle tingimuse täitmine sõltub suuresti Bell County müügi edukast ja õigeaegsest lõpuleviimisest. Samuti pole välistatud paari viimase päeva suurt käivet vaadates, et mõni suurtest fondidest(nt Pirate?) on aktsiast lõplikult väljumas, tekitades lisamüügisurvet.

Probleemid Bell County müügiga seavad kahtluse alla, kas ettevõte kvalifitseerub õigeaegselt lepingu pikendamiseks.

Tähelepanu tasub pöörata sellele punktile lepingu all:

Upon effectiveness of the Amendment, approximately $7.5 million was available for borrowing under the Revolver facility, and approximately $63.6 million of letters of credit were issued under the Credit Facility. The Company expects to be in compliance with the revised maximum leverage and minimum consolidated EBITDA (that is $70 mln) ratios based on current projections. However, compliance with the minimum Liquidity requirement as of February 28, 2007 is substantially dependent upon the Company's sale of assets or securing new financing. There can be no assurance, however, that the Company will be successful in these activities -

Ja veel CHK juurde tulles... CEO Aubrey Mclendon ostis 3. jaanuaril 340 000 aktsiat hinnaga $27.83 (kuigi tema puhul püsivad aktsia ostud on olnud tavalised juba paar viimast aastat).