Börsipäev 27. oktoober

Kommentaari jätmiseks loo konto või logi sisse

-

USA futuurid hetkel eilsete sulgumistasemete juures. Eilsetest tulemuste teatajatest ehk suurima üllatuse valmistas Baidu.com, kelle nõrk tulevikuprognoos viis aktsia järelturul suurde üle 10%lisse langusse. Täna enne turgu teatavad oma tulemused teiste seas Valero, British Petrol, U.S. Steel, AGCO Corp ning pärast turu sulgemist Visa. Link tulemuste tabelile on siin.

Pool tundi enne USA turu avanemist ehk sel nädalal siis kell 15.00 avaldatakse USA oktoobrikuu tarbijausalduse näitu, mille ootus on 53.5 punkti ning CaseSchileri Home Price Index augustikuule, kust oodatakse -11.9%.

-

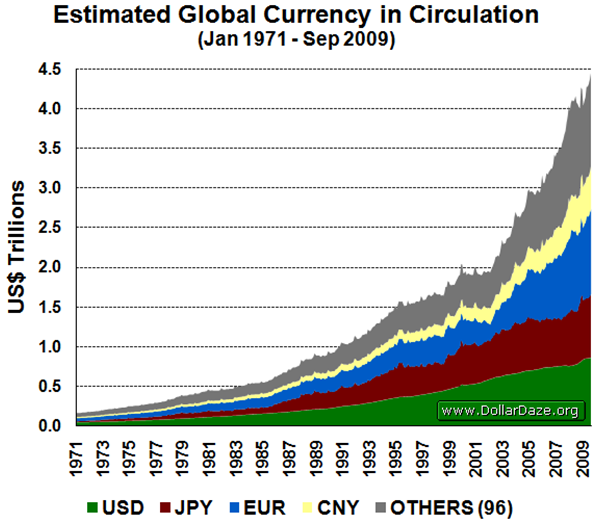

Globaalne ringluses oleva rahapakkumine:

Allikas: DollarDaze

Kui 1990. aastal ületas ringluses olev raha $1 triljoni dollari taseme & 2002. aastal $2 triljoni piiri (kahekordistus 12. aastaga), siis viimase kuue aastaga on see veel kahekordistunud & 2008. aastal ületati 4 triljoni dollari piir.

-

Kuigi India jättis täna intressimäärad muutmata, anti selgeid vihjeid, et lõtva monetaarpoliitikat ollakse koomale tõmbamas ning et tähelepanu on majanduskasvult tagasi üle minemas inflatsiooni ohjeldamisele. India tänasest tegevusest jäi õhku võimalus, et India võib intressimäärasid tõstma hakata veel enne selle aasta lõppu. Link siin.

-

August S&P Case Shiller Composite 20-YoY -11.32% vs -11.90% consensus, July -13.26%

-

Euroopa turud:

Saksamaa DAX +0.11%

Prantsusmaa CAC 40 +0.36%

Inglismaa FTSE 100 +0.42%

Hispaania IBEX 35 +0.03%

Rootsi OMX 30 +1.61%

Venemaa MICEX -2.44%

Poola WIG -1.37%Aasia turud:

Jaapani Nikkei 225 -1.45%

Hong Kongi Hang Seng -1.86%

Hiina Shanghai A (kodumaine) -2.84%

Hiina Shanghai B (välismaine) -1.81%

Lõuna-Korea Kosdaq -0.49%

Tai Set 50 +0.26%

India Sensex 30 -2.31% -

Adapt to the Shift in Character

By Rev Shark

RealMoney.com Contributor

10/27/2009 8:56 AM EDT

Intelligence is the ability to adapt, to change.

-- Stephen Hawking

The key to investment success is to quickly adapt to new conditions as the character of the market shifts. That is much harder to do than it sounds, because it usually doesn't become clear that something has changed until well after the fact.

This market has been particularly tricky, as folks have been looking for the rally to fizzle out ever since it began back in March. At first it was just a minor bear-market bounce, but as it persisted and continued and didn't produce even shallow pullbacks, folks have been wrestling with just how far this rally can go -- so far, it's gone a whole lot further than most anyone thought possible.

As the rally has continued, market players have kept looking for some indication that this time it is different and that a real correction or trend change will finally kick in. We have had five or six pullbacks that looked like they could develop into something more severe and lasting, but in every case the market rebounded strongly just as it looked like we were ready to accelerate more to the downside.

About five days ago we began to pull back once again, and market players are wondering if this finally is going to be a more meaningful market dip. A couple of things look different this time. First and foremost is that the market is selling off on good news. Earnings reports have generally been very good and nothing much has changed as far as the economic reports, but we have seen consistent selling on good news this past couple of weeks. A few big-cap stocks -- most notably Amazon (AMZN) , Apple (AAPL) and Google (GOOG) -- have bucked the trend and helped to support the major indices, but the overall mood has been "sell the news."

Another change in the past week is that we have had a number of intraday reversals and weak finishes. One of the most consistent things that occurred as we rallied was strength in the final hour or two of trading. No one was too worried about early weakness, because they were always optimistic that the buyers would show up later in the day and keep things running. The very persistent dip-buyers ran over anyone who got in the way.

This past week, the late push and dip-buying has dried up. We still haven't really pulled back significantly from the highs, but it is much more of a struggle and the mood is growing more cautious.

During the last seven months, the market has consistently made fools of us if we became more cautious if the action hinted at some weakness. The smart move was to buy any and all weakness and stay unrelentingly bullish. So why should be more cautious this time?

The reason you take heed when the market exhibits signs of weakness is that we must always remember that our No. 1 job is to protect capital. When it looks like the character of the action is changing, we react to it and then ask questions later. If we are wrong and the market recovers and start running again, then we jump back in, but playing defense is cheap insurance.

The market is showing some warning signs here with the poor reaction to good news, diminished dip-buying, weaker dollar and weak closes. We may turn around and go straight back up once again, but for now we need to respect the change in character and be defensive.

We have a mixed start as high-momentum favorite Baidu (BIDU) gets absolutely slammed following its earnings report. There are some good reports out there as well, but it's mostly secondary stocks and they are not affecting the indices much. The market is a little nervous and buyers are hanging back, waiting to see if we can stabilize.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: UCTT +8.5%, LULU +8.5%, HTZ +8.1%, HSP +7.8%, EVVV +7.6%, PCX +7.2%, CE +6.3%, BONT +6.2% (light volume), BP +5.1%, VECO +4.9% (also announces public offering of up to 5 mln shares of its common stock), COG +4.4% (also upgraded to Overweight at JPMorgan), SOA +4.3%, LDK +3.8%, PRE +3.6% (light volume), RCI +3.1%, HMC +2.8%, FLEX +2.7%, DRYS +2.6%, WYNN +1.5%, FDP +1.1%... M&A news: HPGP +31.3% and HLND +23.1% (Hiland Partners announces that Harold Hamm has proposed to increase the merger consideration to be received by the common unitholders of each of Hiland Partners and Hiland Holdings)... Select oil/gas related names showing strength: RDS.A +2.5%, TOT +2.5%, E +1.0%... Select large cap European drug names trading higher: NVS +3.1%, GSK +3.1% (FDA approves new treatment for chronic lymphocytic leukemia), AZN +1.8%, SNY +1.8%... Select financial names ticking higher: AXA +2.0%, DB +1.6%, CS +1.2%... Other news: ANLY +17.0% (Analysts Intl and Microsoft announce new contract to modernize criminal intelligence processes AT Las Vegas Metropolitan Police), ARCI +16.8% (discloses it entered into an Appliance Sales and Recycling Agreement with General Electric), HLCS +16.1% (provides update; expects ~$5 mln in cash receipts from previously announced System orders), MDVN +10.2% (Medivation and Astellas enter into worldwide agreement to co-develop and co-commercialize MDV3100 for the treatment of prostate cancer), SVA +7.9% (obtains third H1N1 vaccine order from Chinese Central Government; under this purchase order SVA is required to produce an additional 5.19 mln doses of PANFLU.1), MVIS +5.0% (received an initial purchase order from its European distributor for its SHOWWX laser-based pico projector), PFG +1.7% (announces $0.50 per share quarterly dividend; up from $0.45 previously), NOC +1.0% and MNRO +1.0% (Cramer makes positive comments on MadMoney)... Analyst comments: PODD +11.1% (upgraded to Outperform from Mkt Perform at William Blair), CAKE +3.0% (upgraded to Buy from Neutral at Goldman- Reuters), TXN +1.3% (upgraded to Outperform at FBR).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: BIDU -19.2%, SGMS -11.0%, ZRAN -10.4%, RCII -9.4%, LTD -9.3%, HMA -9.0%, BLDP -8.3%, WINN -8.1%, CRDN -7.0%, VFC -7.0%, OMI -6.7%, WMS -6.1%, MTXX -5.5%, DTG -4.2% (also files for a 5.75 mln share common stock offering), SCHN -3.3%, EPIQ -2.9%, ALB -2.9%, AFG -1.4%... M&A news: MBRX -40.7% (Ligand will acquire all of the outstanding shares of Metabasis for ~$3.2 mln)... Select Indian related names showing weakness: IBN -4.3%, SLT -4.2%, IFNNY -2.8%... Other news: ICGN -26.0% (reports top-line results of Phase IIa study of senicapoc in exercise-induced asthma; senicapoc failed to demonstrate improvement in the primary study endpoints), ORCC -8.3% (filed for a 13 mln share common stock offering; ~4.621 mln shares are being offered by selling shareholders, the remainder are being offered by the co), HUVL -6.5% (priced a 3.6 mln share common stock offering at $25/share), AGNC -5.1% (prices 5.0 mln common share offering at $26.60/share)... Analyst comments: SE -4.3% (downgraded to Sell at Citigroup), OKE -1.4% (downgraded to Hold at Citigroup), SQM -1.3% (downgraded to Underweight from Neutral at JP Morgan), PALM -1.3% (hearing weakness attributed to downgrade at BMO Capital). -

Baidu on eelturul 19% miinuses & kaupleb kehvade prognooside peale $350 dollari juures. Analüütikud langetavad samuti hinnasihte, kuid tänasest hinnast jäävad need valdavalt kõrgemale:

JP Morgan cut their tgt to $460 from $480

Bernstein cut their BIDU tgt to $420 from $460 following earnings.

Goldman target $435

-

October Consumer Confidence 47.7 vs 53.5 consensus, prior 53.1

-

Amazon tuleb kolinal alla tagasi. Hea, et esialgu putid kätte jätsin ega esimese reaktsiooni peale ei müünud. Mine tea, äkki saan veel kasumitki.

-

Key Senate Democrats reach agreement on homebuyer tax credit extension, according to Senate Banking Chairman Dodd - Reuters

-

Apollo Group prelim $1.06 vs $1.04 First Call consensus; revs $1.08 bln vs $1.03 bln First Call consensus

Apollo Group shares slide through all notable daily moving average support, Sept swing low @ 63.10 is a key price level for possible support

Ja juba kauplemas allpool $62 taset. -

E*TRADE prelim ($0.05) vs ($0.06) First Call consensus

-

Apollo Gruppi rõhumas ka see teade:

Apollo Group announces Securities and Exchange Commission informal inquiry

"The Company announced that the Enforcement Division of the Securities and Exchange Commission ("SEC") has commenced an informal inquiry into the Company's revenue recognition practices. Based on the information that has been disclosed to Apollo Group, the scope, duration and outcome of the inquiry cannot be determined at this time. The Company intends to cooperate fully with the SEC in connection with the inquiry." -

Visa prelim $0.74 vs $0.72 First Call consensus; revs $1.88 bln vs $1.78 bln First Call consensus

-

APOL on üldiselt tulemusi alati biitinud ja teinud seda ikka vähemalt 10 sendiga - seega väike külm dušš neist numbritest tõepoolest.

-

Visa esimese reaktsioonina samuti kukkumas, kui kivi. Kerge toetuse annab aga selline uudis: Visa authourizes $1b ln share repurchase plan