Börsipäev 5. jaanuar

Kommentaari jätmiseks loo konto või logi sisse

-

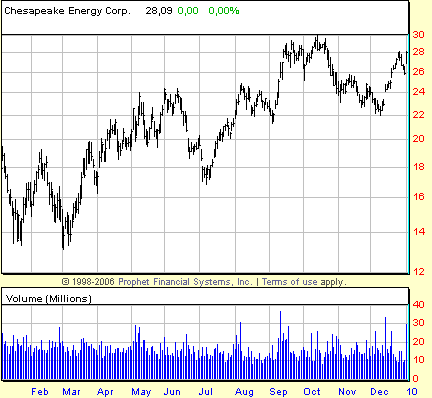

Eile tõusis koos nafta ja maagaasihindade ralli ning Chesapeake Energy (CHK) ja Totali (TOT) vahel sõlmitud partnerluslepingu toel CHK aktsia ca 8%. Kui Goldman langetas oma soovituse 'hoia' peale (hinnasiht tal jätkuvalt $32), siis Deutsche Bank kinnitab täna oma ostusoovitust ja ja tõstab hinnasihi $33 pealt $35 peale ning Citigroup kinnitab oma hoia-soovitust ja tõstab hinnasihi $28 pealt $32 peale. Kuigi aktsia on lühikese aja jooksul tugevalt tõusnud ja võime turu nõrkuse korral CHK'le kohaselt näha ka volatiilsemat allapoole korrektsiooni, usun siiski, et see jääb pigem lühiajaliseks ning et pikaajaliselt on CHK aktsiatel veel potentsiaali tõusta küllaga ning väärivad jätkuvalt kohta investeerimisportfellis.

-

Tänased tähtsamad makroandmed tulevad USAst Eesti aja järgi kell 17.00, mil teatatakse novembrikuu tehaste tellimuste muutus - ootuseks on +0.5%. Samuti teatatakse novembrikuu pending home sales näitaja, millele oodatakse 2%list langust (majanduse tugevuse seisukohalt oleks vajalik, et pending home sales ja tehaste tellimused tõuseksid mõlemad võimalikult palju).

-

Väike meenutus ka minevikku. 2009. aasta esimesel kauplemispäeval tõusis S&P500 indeks +3.16%, teisel kauplemispäeval liiguti +3.16%, kolmandal päeval -0.47%, neljandal päeval +0.78% ning viiendal päeval -3.0%. Seejärel järgnes mitmekuine langus ning aasta neljas kauplemispäev jäi kuni aprillini ka aasta kõrgeimaks hinnatasemeks.

Hommikused futuuriliikumised lubavad igaljuhul ka seekord oodata aasta teisel päeval turgude jätkuvat tõusu. -

Euroopa turud:

Saksamaa DAX -0,27%

Prantsusmaa CAC 40 +0,09%

Inglismaa FTSE 100 +0,42%

Hispaania IBEX 35 +0,54%

Rootsi OMX 30 +0,39%

Venemaa MICEX N/A (börs suletud)

Poola WIG +0,80%Aasia turud:

Jaapani Nikkei 225 +0,25%

Hongkongi Hang Seng +2,09%

Hiina Shanghai A (kodumaine) +1,18%

Hiina Shanghai B (välismaine) +1,34%

Lõuna-Korea Kosdaq +0,95%

Tai Set 50 -0,08%

India Sensex 30 +0,73% -

Looks a Lot Like 2009 Around Here

By Rev Shark

RealMoney.com Contributor

1/5/2010 8:32 AM EST

He who is not everyday conquering some fear has not learned the secret of life.

-- Ralph Waldo Emerson

We started off the year on a positive note. We had strong gains on excellent breadth and increased volume. Volume could have been better, but it is tough to quibble when we had so many pockets of very strong action. China-related stocks did particularly well, and oil, gold and commodity names benefited from a weaker dollar.

If you want to find a negative, the easiest argument is that strength to start the year is just positive seasonality driven by factors other than fundamental considerations. While that may indeed be the case, a gain is a gain no matter why it occurred. While strength may have been driven by beginning-of-the-year inflows and money managers anxious for a good start to the new year, it doesn't change the fact that we had some pretty impressive strength.

Technically the indices are a bit stretched at this point, but if there is one lesson we learned over and over in 2009 it is that we shouldn't fear an overbought market, as they can (and often will) become even more overbought. We consistently had some straight-up action at the beginning of a new month. In September, October and November in particular we had multiple positive days in a row early in the month.

So once again here we are in a situation with a strong but a bit technically extended market and players rather complacent. While it would make sense to worry about that setup, this is the sort of environment that consistently has produced a large supply of dip-buyers. Many market players are too disciplined to chase strength but they are happy to jump in on any minor pullbacks. That is what gave us so many long winning streaks in 2009.

Strong positive seasonality begins to wane after the first few days of January, and we usually have at least one good bout of profit-taking fairly early in the year as those who delayed taking taxable gains in the prior year move to lock in some profits. However, another lesson we learned over and over in 2009 is that it was a mistake to anticipate weakness. The market consistently ran up much further than many folks thought reasonable and produced some impressive short squeezes.

Although we are only two days into the new year, the action still feels very much like it did in 2009. That means we have to respect the strength and not be overly concerned about when it might end. That doesn't mean that we should become undisciplined, but until the bulls actually do something wrong they deserve our respect.

The dollar is weak again this morning, which is helping to boost gold, oil and commodities, but the indices are around flat. Apple (AAPL) is active on some confirmation that its iTablet device will indeed be on the market in the next few months.

-----------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: MERX +22.8% (light volume)... Select financial names showing strength: IRE +7.9%, RBS +7.6%, AIB +5.6%, BCS +4.4%, ING +3.8%, LYG +2.9%, DB +2.4% (initiated with Overweight at Barclays), HBC +2.2% (initiated with Overweight at Barclays), STD +1.7%, CS +1.6%, UBS +1.1%... Select metals/mining names showing early strength: IAG +1.8%, AU +1.4%, SLW +1.3%, EGO +1.3%, RTP +1.0%... Select casino related names trading higher: MPEL +3.6%, LVS +3.5% (initiated with a Overweight at Barclays Capital), MGM +2.9%, BYD +1.9%... Other news: BSQR +27.4% (renews OEM distribution agreement with Microsoft), YTEC +11.4% (Yucheng Technologies and NTT DATA Establish E-Banking ASP Joint Venture), WAVX +8.9% (receives $5.7 mln in software license and maintenance orders for a global automaker), ACH +6.3% (still checking), WPRT +6.2% (Cramer makes positive comments on MadMoney), APWR +3.7% (Signs License Agreement with W2E Technologies)... Analyst comments: THC +9.2% (added to ConvictioN Buy list at Goldman- Reuters), ZOOM +9.0% (initiated with a Buy at Global Hunter Securities), SLXP +8.2% (target raised to $58 at Piper Jaffray), RSH +5.2% (upgraded to Buy at Goldman; added to Conviction Buy list, tgt raised to $25 from $21- Reuters), TKC +4.9% (upgraded to Buy from Neutral at BofA/Merrill), PALM +4.1% (initiated with Overweight at Morgan Stanley), POT +2.6% (upgraded to Outperform at Credit Suisse), AXL +2.2% (upgraded to Neutral from Underperform at BofA/Merrill), QCOM +1.9% (initiated with Overweight at Morgan Stanley), RIMM +1.6% (initiated with Overweight at Morgan Stanley), IPI +1.6% (upgraded to Neutral at Credit Suisse), BIIB +1.4% (upgraded to Neutral at BofA/Merrill), TEVA +1.1% (initiated with an Outperform at Calyon), DELL +1.0% (initiated with a Buy at Stifel Nicolaus), COF +1.0% (upgraded to Buy from Hold at Stifel Nicolaus).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: CELL -6.8%, ACE -1.4%... M&A news: CBY -3.4% (Kraft sweetens Cadbury takeover offer; Nestle (NSRGY) also declared that it would not make or participate in a rival offer for the British confectioner- FT)... Select European drug names trading lower following weakness overseas: SHPGY -2.8% , GSK -2.5% , AZN -1.2% , SNY -1.0%... Other news: MESA -36.4% (commences restructuring), JTX -2.9% (provides update on SBBT to prevent any interruption in financial product program for the 2010 tax season)... Analyst comments: BEXP -3.3% (downgraded to Neutral from Overweight at JP Morgan), ASIA -2.8% (downgraded to Neutral from Buy at Goldman- DJ), LFT -2.2% (downgraded to Neutral from Buy at Goldman- DJ), XCO -1.3% (downgraded to Underweight at JPMorgan). -

Külmad ilmad Hiinas on kiiresti suurendanud nõudlust söe ja gaasi järele. Kui näiteks Pekingi jaanuari ajalooliseks keskmiseks maksimumtemperatuuriks on päeval +2 ja öösel keskmiseks miinimumtemperatuuriks -9, siis viimasel nädalal on Pekingis valitsevad külmad ilmad neist numbritest oluliselt madalamal ning ka järgnevate päevade ilmaprognoos muutust ei luba. Kolmapäeval oodatakse päeval -7, öösel -16; neljapäeval päeval -6, öösel -13; reedel päeval -6, öösel -11; laupäeval päeval -5, öösel -12; pühapäeval päeval -3, öösel -13 kraadi.

Seega energiavarusid põletatakse heleda leegiga. -

Pending Home Sales M/M -16.0% vs -2.0% consensus, prior +3.9%.

November Factory Orders +1.1% vs +0.5% consensus, prior revised to +0.8% from +0.6%. -

Majade müük oli novembris väga kehv. Statistika mõjutas ilmselt see, et esialgu pidi esmakordsetele kinnisvara ostjatele mõeldud maksusoodustus novembris lõppema. Lõpuks otsustati seda siiski pikendati 30. juunini 2010. Kinnisvaraturu jaoks oluline, et uuel aastal (paljud arvavad, et kevadel) otsjad turule tulevad.

-

World Bank sees "relatively muted" global recovery, official says - DJ

-

Avatari edu sunnib IMAXit (IMAX) uusi võimalusi otsima & NYT kirjutab, et koos Discovery & Sonyiga plaanitaks juba järgmisel aastal tuua turule 3D telekanal (IMAX kaupleb täna +4.4%):

NY Times reports Discovery (DISCA), Imax and Sony (SNE) are forming a joint venture for a 3-D television channel, two people with knowledge of the deal said. The joint venture will be announced sometime Tuesday, timed to the Consumer Electronics Show in Las Vegas, where 3-D television is expected to be a hot topic. The three companies will own equal stakes in the channel, according to one of the people with knowledge of the deal, who requested anonymity because the channel had not been announced. Discovery Communications, which operates the Discovery Channel, TLC and other cable channels, will distribute the channel, which has a 2011 start date. It is expected to showcase a mix of 3-D content, including entertainment and sports. It will also show some of the natural history programming that Discovery is well known for.

-

Lisaks Hiinas valitsevale külmale ilmale tahaks ära märkida ka erakordselt külma talve Venemaal, Suurbritannias ning USA mitmes põhja-osariigis. Suurbritannia andis täna välja kõrgeima kategooria ilmahoiatuse, kuna ootab põhjast lõuna poole liikuvast pilvemassiivist ca 20 sentimeetrilist lumevaipa ning sellele peaks järgnema kuni -20 kraadine külmalaine, mis toob mitmele poole uued külmarekordid. Kõik see mõjub positiivselt energia hindadele, kuna varud on üha kiiremini kokku kuivamas ning teadupärast olid energia ettevõtted madalate energiahindade tõttu ju majanduslanguse perioodil oma investeeringuid sektoris tugevasti koomale tõmmanud.

-

Tea, miks kliimasoojenemise eest võitlejad kuskil meelt ei avalda?

-

Fitch downgrades Iceland to 'BB+'/'BBB+'; outlook negative

-

U.S. Judge sides with tobacco companies on challenge to FDA ban on color, graphics in labels, advertising; Judge also says cannot ban tobacco claims implying that products safer because of FDA regulation - Reuters

-

Fitch siis alandas Islandi krediidireitingu prügi peale. Viimane investment grade tase on BBB.

-

IMAX on tänase teate peale koos Discovery ja Sony'ga 3-D televisioonikanal luua rallinud ca 8%. Kuna 15. detsembri seisuga oli ca 3.7 miljonit aktsiat IMAXis lühikeseks müüdud, siis sellised positiivsed teated panevad lühikesi korralikult higistama. Seda enam, et 3.7 miljonit aktsiat on ca 5-kordne keskmine päevakäive.