Börsipäev 6. aprill

Kommentaari jätmiseks loo konto või logi sisse

-

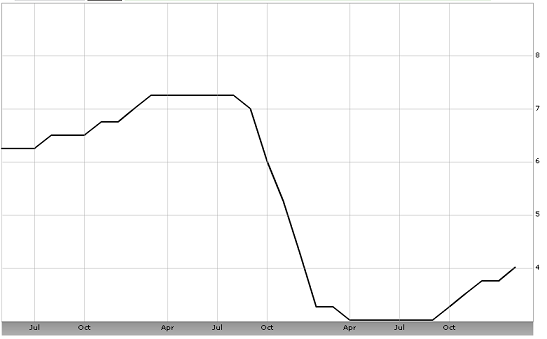

Eile suutsid suuremad USA indeksid liikuda heade makrouudiste peale uute selle aasta tippude juurde (reageeriti ka reedel avaldatud tööjõu raporti peale, kuna börsid olid reedel pühade tõttu suletud). Täna USAst makrouudiseid tulemas ei ole. Hommikul üllatas investoreid aga Austraalia keskpank, kes tõstis baasintressimäära 4% pealt 4.25% peale (loe pikemalt siit). Austraalia keskpank on tõstnud viimasel kuuel kohtumisel juba viis korda intressimäära:

Fed ja ECB ei ole jätkuvalt intressimäärade tõstmisest märke andnud, kuna leiavad, et majanduskasv on veel liiga nõrk (inflatsioon madal ja pangad ei väljasta piisavalt laene).

-

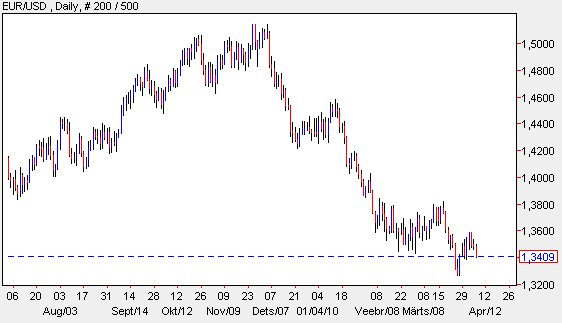

Euro ei suuda oma tugevust hoida ja turul tundub olevat jätkuvalt soov euro tugevust müümiseks kasutada:

-

Ühtegi makroraportit täna turgude meeleolu suunamas ei ole, kui ainsana võiks veidi elevust pakkuda FOMC märtsikuu protokoll (kell 21.00). Kuust kuusse on FEDi sõnastus püsinud muutumatuna, kinnitades leebe rahapoliitika jätkumist, kuid mida selgemaks saab majandusliku taastumise jätkusuutlikkus, seda tõenäolisemalt tuleb hakata turgusid rahapoliiitka karmistamiseks ette valmistama. Osade arvates võiks liikumist selles suunas täheldada juba tänasest protokollist.

-

JPM alustas oil service sektori katmist positiivse väljavaatega. Hoiame sektoril ka ise silma peal ja lähiajal tutvustame ilmselt Pro all ka mõnda ettevõtet pikemalt:

JP Morgan initiates coverage of five offshore drillers in the oilfield services sector with a generally cautious outlook on the group. Firm says while they anticipate global upstream spending to increase by year-end 2010, they believe dayrates for both floating rigs and jackups rigs will likely remain subdued into 2011. Until oil fundamentals tighten and the exploration cycle ramps up, pricing power is in the hands of producers, which are showing scant signs of increasing activity levels. ESV and NE appear to have the most near-term earnings leverage and RIG and PDE the most leverage longer term. Firm says their top pick is ESV, and Diamond (DO) is their least preferred. The firm initiates ESV, SLB, and HAL with Overweights. They initiate RIG, NE, PDE, and BHI with Neutrals, and DO, and WFT with Underweights. (briefing)

-

EUR/USD on päeva jooksul 1.3400 tasemest läbi vajunud ja Kreeka valitsuse 10. a. võlakirjade yield on teinud samuti järsu hüppe 6.5% juurest 7% juurde. Dollari kallinemine on rõhumas ka tooraineid ja aktsiaturge...

-

Gapping down

In reaction to disappointing earnings/guidance: BYI -5.6% (Isle of Capri and Bally Technologies announce Rainbow Casino Deal ; also downgraded to Neutral from Outperform at Macquarie), CA -3.7% (announces workforce reduction of ~1,000 positions), SVA -3.2%... Select financial related names showing weakness: IRE -6.9%, STD -3.4%, DB -3.0%, LYG -2.7%, PUK -2.0% (Prudential in talks with investors - FT), CS -1.5%, HBC -1.4%, ING -1.4%... Select drug related names showing weakness: GSK -4.4% (Crucell N.V. announces collaboration with GlaxoSmithKline Biologicals on second generation malaria vaccine candidate), NVS -1.7%, SNY -1.2% (Sanofi-Aventis settles further Eloxatin patent suits - Reuters.com)... Other news: MEE -7.5% (confirms twenty-five fatalities at its Upper Big Branch Mine, WV resulting from an explosion), UNIS -6.7% (pulling back from yesterdays 40%+ jump), TNK -6.4% (announces offering of 7.7 mln shares of Class A common stock at $12.25/share), RDEA -4.9% (announces pricing of 3.5 mln share offering of common stock), TLVT -3.8% (announces a $175 mln sr subordinated convertible notes offering), PMI -3.7% (still checking), BEXP -3.4% (files mixed securities shelf offering for indeterminate amount), HMY -2.4% (still checking), SAP -1.5% (still checking)... Analyst comments: PHM -3.6% (downgraded to Underperform from Neutral at Credit Suisse), KBH -2.7% (downgraded to Neutral from Outperform at Credit Suisse), SPWRA -1.5% (resumed with an Underweight at JP Morgan).

Gapping up

In reaction to strong earnings/guidance: ROG +6.2%... Other news: PURE +9.8% (light volume; receives U.S. EPA registration for SDC-based disinfectant and food contact surface sanitizer), CPBY +8.5% (selected by the State Grid Corporation of China as Sole Domestic GIS Provider for Smart Grid), CIGX +6.0% (still checking), NWE +3.7% (will replace The Dress Barn in the S&P SmallCap 600 index), TIVO +3.5% (still checking), KOG +2.9% (acquires 5,500 net acres of Williston Basin leasehold prospective for Bakken and Three Forks Oil Production), DNDN +2.4% (still checking), EP +1.5% (receives FERC approval for Ruby pipeline), COST +0.7% (Cramer makes positive comments on MadMoney)... Analyst comments: AVNR +8.5% (initiated with a Buy at Canaccord), BEAT +7.3% (upgraded to Buy from Hold at Roth Capital), PUDA +3.4% (initiated with a Buy at Brean Murray),

-

Rev Shark: Look Ahead to Earnings

04/06/2010 7:41 AMFaced with the choice between changing one's mind and proving that there is no need to do so, almost everyone gets busy on the proof.

-- John Kenneth GalbraithJust about everyone is scratching their heads and wondering when this market might finally be hit with some profit-taking. Conditions have been unchanged for almost two months now and are still showing few signs that a top is near.

The gain since Feb. 5 has been quite substantial, but most remarkable has been the consistency of the action. The S&P 500 has pulled back more than 1% just once -- way back on Feb. 23 -- and if you have been waiting to buy on a dip, you have had almost no opportunity to do so.

If you are an active trader, you only have two choices for dealing with this sort of action. Either you keep riding the momentum until it fails or you try to anticipate a turning point. I don't have to tell you which approach is working better. Market players have not cared one bit about the indices being technically extended and negatives like higher interest rates, a stronger dollar and higher oil have been shrugged off as we chug along relentlessly.

The problem for momentum investors and trend traders is that little volatility makes it impossible to find good entry points. The essence of momentum trading is summed up in the old saying, "Buy the dips and sell the rips." However all we have had is rips, and that is leaving more and more folks on the sidelines as they sell into strength and then are unable to find new buys.

This has been one of the most hated rallies I can recall. I think that hatred is largely due to the lack of participation by individual investors. Many never returned to the market after they were pummeled in the meltdown, and those who did return have struggled to reconcile this buoyant market action with the economy that is very slowly starting to improve. It seems the market has already priced in a very rosy future, but most individuals are still very worried about jobs, real estate and the pace of economic growth.

Like most other traders, I've found this market that moves only in one direction to be a challenge to trade. I've dealt with it by not trying to anticipate a top but by staying short-term bullish and being very zealous about protecting gains while I have them. Until we actually have some pullbacks or flat action, it is going to be very tough to be aggressive.

The good news is that earnings season is fast approaching, and that will be a good source of potential volatility. At the moment all news is good news, but this straight-up action into earnings season has the potential to create some "sell the news" action if companies do not live up to the high expectations that have been created over the past two months.

Early indications this morning shows some slight weakness. European markets are back open after the holiday and are playing catch-up with some gains while in Asia it is a bit more mixed with weakness in Japan while China remains closed.

We have a Treasury auction and minutes of the last FOMC meeting this afternoon, but there is little economic news to drive the action. The dollar is going to be key once again. Strengthening there is likely to be the catalyst for some selling.

-

Euroopa turud kaotasid päeva teises pooles oma tugevuse, USA alustas -0.4% madalamal.

Euroopa turud:

Saksamaa DAX -0.14%

Prantsusmaa CAC 40 -0.02%

Inglismaa FTSE 100 +0.30%

Hispaania IBEX 35 -0.47%

Rootsi OMX 30 +0.31%

Venemaa MICEX +0.50%

Poola WIG +0.50%Aasia turud:

Jaapani Nikkei 225 -0.50%

Hong Kongi Hang Seng suletud

Hiina Shanghai A (kodumaine) +0.02%

Hiina Shanghai B (välismaine) ++0.12%

Lõuna-Korea Kosdaq +0.25%

Tai Set 50 suletud

India Sensex 30 +0.03%