Börsipäev 8. juuni

Kommentaari jätmiseks loo konto või logi sisse

-

Eilse börsipäeva lõpp kujunes taas punaseks ning müügisurve oli selgelt üle ostuhuvist. Viimase pooleteist kuuga on aktsahinnad läbi teinud tugeva korrektsiooni ning kuu aja pärast näeme juba esimesi teise kvartali tulemusi. Praeguse langusega on ootused tugevalt allapoole tõmmatud ning sellise languse järel võiks minu arust ostuhuvi tulemuste eel siiski taastuda. Aga saame näha.

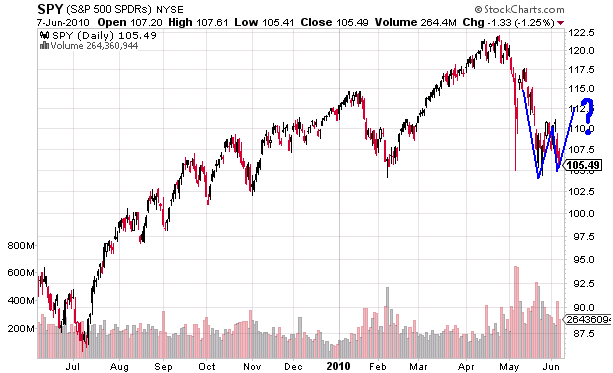

Tehnilist analüüsi pooldavatele kauplejatele siia üks graafik. Kumb tundub tõenäolisem - kas W-põhi ja põrge üles või maikuu põhjadest läbikukkumine ja uutele 8 kuu põhjadele liikumine?

USAst olulisi majandusraporteid täna tulemas ei ole. Varasel eelturul on USA indeksite futuurid ca 1% jagu plussis.

-

Apple tutvustas eile uut iPhone'i, mis osutus oma omaduste poolest ootuspäraseks. Vaata lühikest klippi PC Worldi vahendusel siit. Telefon on 24% õhem võrreldes 3GS mudeliga ja Jobsi sõnul ühtlasi kõige õhem turul leiduvatest smartphone'dest. Tagumine kaamera on 3MP asemel nüüd 5MP ja võimeline salvestama 720p HD videot. Lisaks on videokõnedeks lisatud VGA kaamera ka telefoni esiküljele (videokõned hetkel siiski ainult läbi wifi). Ekraani kõrgem resolutsioon, 4x suurem kontrastsus võrreldes 3GS-ga, kiirem protsessor, parem aku kestvus ja uus OS, mis võimaldab multitaskingut annavad iPhone 4-le kahtlemata märkimisväärse eelise võrreldes lähimate konkurentidega. Analüütikud on oma esimestest kommetaarides positiivselt meelestatud, uskudes et iPhone 4 uued omadused ajendavad seniseid kliente oma vana iPhone'i uuendama, tagades Apple'le turuosa edasise kasvu.

-

Fitch hoiatab, et Suurbritannia valitsusel seisab ees keeruline ülesanne, et eelarved tasakaalu saada (sama võib öelda ka USA kohta):

Britain's fiscal challenge is "formidable" and warrants a faster pace of deficit reduction than was outlined in the April 2010 budget issued by the previous Labour government, Fitch Ratings warned on Tuesday. The agency praised the new Conservative-Liberal Democrat coalition for acting "very quickly" to make fiscal consolidation a top priority. (link)

-

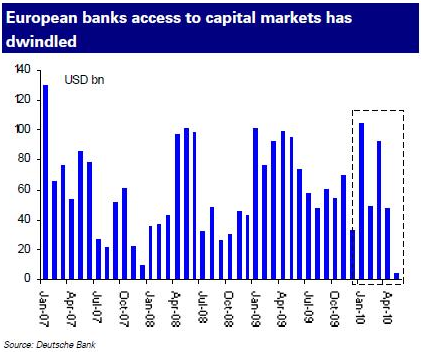

Oleme ka varem juhtinud tähelepanu kapitaliturgude külmumisele pärast euroala võlakriisi esilekerkimist. Siin veel üks hea Deutsche Banki graafik, mis näitab, kui palju Euroopa pangad võlga on väljastanud (mais madalaim tase alates 1989. detsembrist).

(kaua selline olukord kesta ei saa, kuna Euroopa pankadel on vaja järgnevate aastate jooksul tagasi maksta või refinantseerida ca 700 miljardi euro eest võlga aastas)

-

Panen siia ühe graafiku, mis investoritele viimasel ajal ilmselt tuska valmistamas. Nimelt Hispaania 10-aastase võlakirja tulususmäär on kerkimas üha kõrgemale ja kõrgemale. Hetkel on see jõudnud juba 4.65% peale:

-

USA indeksid alustavad päeva ca 0,3%lise plussiga.

Euroopa turud:

Saksamaa DAX -0,70%

Pantsusmaa CAC 40 -0,77%

Suurbritannia FTSE100 -0,65%

Hispaania IBEX 35 -1,06%

Rootsi OMX 30 -0,37%

Venemaa MICEX -0,70%

Poola WIG +0,10%Aasia turud:

Jaapani Nikkei 225 +0,18%

Hong Kongi Hang Seng +0,56%

Hiina Shanghai A (kodumaine) +0,08%

Hiina Shanghai B (välismaine) +1,56%

Lõuna-Korea Kosdaq +1,49%

Tai Set 50 -0,48%

India Sensex 30 -0,98% -

Navigating the Muck

By Rev Shark

RealMoney.com Contributor

6/8/2010 8:40 AM EDT

I'm not upset that you lied to me; I'm upset that from now on I can't believe you.

-- Friedrich Nietzsche

The market has sold off over the past week with enough energy to set the stage for some sort of oversold bounce. But we should not be very trusting of upside at this point. There is no reason to expect that the recent correction has hit bottom. Sentiment has simply become so negative and the selling so extreme that some relief is bounce to occur in the near term. But this is a broken market and we have to respect that fact until conditions improve.

There is a tremendous amount of uncertainty about the European economic situation, and we have very little positive news flow. This morning ratings agency Fitch warned that the U.K. faces formidable fiscal challenges. Virtually every major economy other than the U.S. is now focused on cutting spending and implementing austerity measures. In the U.S., we have shifted from celebration of the economic recovery to concerns that it is going to be painfully slow. Problems at the state and local government levels are gaining traction and further stimulus and bailouts have lost their appeal as the deficit spirals ever higher.

I really don't need to list all the negatives. The market action speaks for itself. There is a lot of worry and concerns out there, and many market players are moving to the sidelines until they have some clarity.

Our job is to navigate this mess, and it is a tricky task. We can try to catch some oversold bounces. The biggest spikes tend to occur within downtrends, so there is good opportunity if we time things right. But we can pretty much forget the "V"-shaped bounces that worked so well from March 2009 through April 2010. This market has undergone a substantial change in character over the past month and we need to respect that.

If your time frame is short enough, it's now probably a good time to watch for some snapback trades. For the longer-term investor, there is little reason to do any major buying at this point. You might add a little to some favorite names, but it's a good idea to keep your powder dry and wait for signs that a more lasting turn may be in the cards. The biggest danger in a downtrend is being too quick to assume that we have hit bottom. It is quite easy to mistake an oversold bounce for a lasting turn; the only way to decrease the risk is to stay skeptical of calls that a trend change is at hand.

We had some absolutely dismal action yesterday, and it looks like market players are trying to be a bit more upbeat this morning. If we can hold gains early, we have a good chance that a bounce will gain some traction, but be ready to do some flipping into strength. This is not the time to be very trusting of the market action.

----------------------------------

Briefing.com vahendusel:

Ülespoole avanevad:

In reaction to strong earnings/guidance: DG +3.0%, TLB +2.4%, ALTR +1.2%.

Select metals/mining stocks trading higher: BHP +2.1%, HMY +2.0%, EGO +1.8%, VALE +1.7%, PAL +1.6%, BBL +1.7%, SLW +1.4%, ABX +1.2%, NEM +1.2% (acquires 2,000,000 shares of Eurasian Minerals through private placement), RTP +1.0%.

Other news: ABK +23.3% (announced that it has commuted all of its remaining $16.4 bln of exposure to collateralized debt obligations of asset-backed securities), DEPO +10.6% (announces acceptance of new drug application for investigational postherpetic neuralgia treatment DM-1796), HERO +5.6% (still checking for anything specific), AONE +5.0% (announced a production agreement with Navistar subsidiary to supply lithium ion battery systems for electric vehicles), DNDN +3.0% (still checking for anything specific), BIDU +1.4% (Cramer makes positive comments on MadMoney), VVUS +1.3% (Positive results from Ph. 2 study of Qnexa in obstructive sleep apnea presented at SLEEP 2010).

Analyst comments: GLW +2.5% (upgraded to Outperform from Market Perform at Bernstein), ABB +2.3% (upgraded to Buy from Neutral at Goldman), TCK +1.6% (upgraded to Overweight from Neutral at HSBC), AET +1.4% (initiated with Outperform at Wells Fargo), FCX +1.2% (upgraded to Overweight from Neutral at HSBC).

Allapoole avanevad:

In reaction to disappointing earnings/guidance: NWY -7.9%, FCEL -6.6%, PBY -1.7%.

Other news: DFR -9.6% (thinly traded, light volume; received a "Wells notice" from the Staff of the SEC ), WX -2.8% (Jana Partners discloses 7% stake in Charles River; sees WuXi acquisition as suboptimal), BP -1.5% (announces 1Q10 dividend of $0.84/ADS; record date was May 7, 2010).

Analyst comments: DO -2.7% (downgraded to Sell at Goldman, downgraded to Underperform at FBR), NE -1.6% (downgraded to Neutral at Goldman, downgraded to Mkt Perform at FBR), RIG -1.1% (downgraded to Neutral at Goldman). -

Daniel Amerman on kirjutanud üsna huvitava artikli selle kohta, mida euro nõrkus USA töökohtade jaoks tähendab: US Employment May Be Hammered By Euro Plunge.