Börsipäev 8. oktoober

Kommentaari jätmiseks loo konto või logi sisse

-

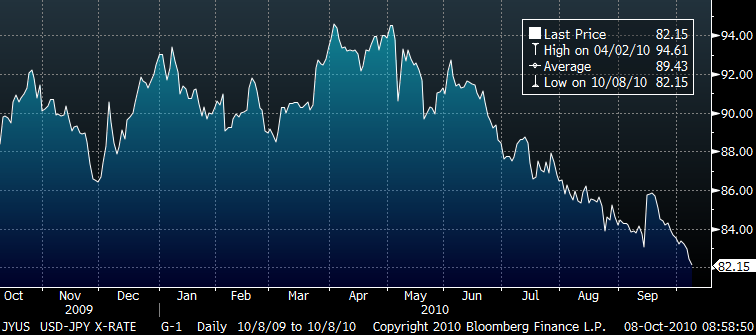

Kuigi suurem osa Aasia börsidest on enne USA tööjõuraportit kerges miinuses kauplemas, siis nädalase püha tõttu riskiisu paranemisest ja toorainete hinnatõusust kõrvale jäänud hiinlased olid suurema ostuhuviga kohalikul turul nelja nädala võimsaimat rallit toetamas. Shanghai Coposite kerkis 3,4%, samal ajal kui Hang Seng oli 0,7% plussis, Nikkei 225 aga -1,0% punases. Viimasele oli järjekordselt survet avaldamas tugevnev jeen, kui USD/JPY vahetuskurss jõudis hommiku poole käia tasemel 82,15.

Septembrikuu tööjõuraport (kl 15.30) saab olema tänase päeva haripunktiks ning kuigi ADP numbrid võisid selles osas paljusid kergelt pessimistlikumaks muuta, ootab konsensus endiselt 74 000 töökoha loomist erasektoris ning rahvaloendajate vähendamise tõttu 0 töökoha loomist nii era- kui avalikus sektoris kokku. Töötusemääraks prognoositakse 9,7% vs 9,6% augustis.

-

Suurbritannia septembri tootjahinnaindeksid tulid oodatust kõrgemad. PPI Output (Y/Y) 4,4% vs oodatud 4,3% ja PPI Output Core 4,6% vs oodatud 4,3%. Naelsterling on päevasest põhjast $1,5821 taastumas ja kaupleb hetkel $1,5857 juures.

-

Keegi on INTC aktsiate müümisega eelturul väikse vea teinud ja hinna $5.12 madalamale müünud, mis on 26.39% langust. Tõenäoliselt need tehingud tühistatakse, kui tehingut ei ole sisestatud manuaalselt teisele börsile peale Nasdaqi.

-

Panen siia lingi pikemale videole, kus Paul Krugman, endine Reagani nõunik ja NBERi president Martin Feldstein ning Goldmani Jan Hatzius esinevad USA majanduse teemal ja kellelgi pole kuigi palju positiivset öelda.

-

USA tööjõuturu septembrikuu muutuseks oli esialgsetel hinnangutel -95 000 vs oodatud -5 000 (erasektoris oli see +64 000 vs oodatud +75 000). Augustikuu tööjõuturu näit revideeriti -54 000 pealt ümber -57 000 peale. Töötusmääraks 9.6% vs oodatud 9.7%.

-

Kehv seis tööjõuturul tähendab seda, et märkimisväärse kvantitatiivse lõdvendamise programmi teatamise tõenäosus novembri alguse Föderaalreservi miitingul on ülimalt tõenäoline.

Printing time... -

USA töötururaport pakkus eurole tuge ja kaupleb hetkel $1,3970 juures. Jeen tegi dollari vastu jällegi uue 15 aasta tipu Y81,99 juures.

-

Aga tugi ei kestnud üleliia kaua, nüüd juba 1,3870 juures

-

Kui valuutadest veel rääkida, siis USA dollar langes pärast tänast tõõjõuraportit jeeni suhtes viimase 15 aasta madalaimale tasemele ehk päevasiseselt kauples valuutapaar hetkeks ka alla 82 jeeni dollari kohta.

-

Gapping down

In reaction to disappointing earnings/guidance: KLIC -15.3% (Dec qtr revs to be significantly below September qtr revs vs consensus is for a ~2% sequential drop).

Select financial related names showing weakness: NBG -2.3%, IBN -1.3%, CS -1.2%, STD -1.2%, PUK -1.2%, LYG -0.6%, UBS -0.6%.

Other news: CYTX -12.5% (priced a 4 mln share common stock offering at $4.50/share ), NMM -6.9% (announces public offering of 5,500,000 common units), ONXX -6.5% (announced that it will delay its New Drug Application filing for carfilzomib), ASMI -4.4% (still checking), ADBE -2.4% (announces definitive interim results of public tender offer for shares of Day Software; ADBE popped yesterday following MSFT takeover rumor).

Analyst comments: FFIV -3.8% (downgraded to Sell from Neutral at Goldman), JKS -3.0% (downgraded at Oppenheimer), KLAC -2.9% (downgraded to Sell from Hold at Deutsche Bank), EXPE -2.8% (downgraded to Neutral from Buy at Goldman), FMCN -2.6% (downgraded to Neutral from Positive at Susquehanna , LRCX -2.0% (downgraded to Sell from Hold at Deutsche Bank), OI -1.9% (downgraded to Neutral from Outperform at Credit Suisse), ZUMZ -1.9% (downgraded to Neutral from Overweight at Piper Jaffray ), MOT -1.5% (downgraded to Hold from Buy at Citigroup), BTU -1.2% (downgraded to Market Perform from Outperform at BMO Capital), AMZN -1.1% (removed from Conviction Buy List at Goldman), NVLS -0.8% (downgraded to Sell from Hold at Deutsche Bank), SOLF -0.7% (downgraded to Hold at Auriga), FDO -0.6% (ticking lower; downgraded to Market Perform from Outperform at Wells Fargo),

Gapping up

In reaction to strong earnings/guidance: TTO +8.1%, SCSC +7.9% (also upgraded to Buy at Stifel following raised guidance), DRWI +6.6%, AA +2.8%.

M&A news: GENZ +0.9% (unanimously rejects Sanofi-Aventis $69.00 per share tender offer; says price is inadequate).

Select metals/aluminum stocks trading higher following AA earnings/guidance/commentary: MT +1.5%, RS +1.3%, KALU +1.2%, TIE +1.0%, CENX +1.0%.

Other news: ATNI +8.3% (will replace Dril-Quip in the S&P SmallCap 600), MIPI +5.3% (ticking higher; received two letters regarding deficiencies relating to NASDAQ Rules; has a grace period of 180 calendar days to regain compliance), ALXA +4.8% (still checking), RSTI +4.7% (will replace Cogent in the S&P SmallCap 600), CCME +4.4% (still checking), TSYS +3.5% (receives $9.3 mln world-wide satellite systems order from U.S. Army through August 2011), DRQ +1.2% (will replace Burger King Holdings in the S&P MidCap 400), RIMM +0.6% (UAE confirms announces that all Blackberry services in the UAE will continue to operate as normal and no suspension of service will occur on October 11), ALK +0.5% (modestly rebounding after the stock was under pressure in late trade on reports of SEC CEO investigation; co has issuedstatement on Bloomberg news report).

Analyst comments: OSK +2.6% (upgraded to Buy from Neutral at Goldman), TUP +1.5% (upgraded to Buy from Neutral at Goldman), KO +0.6% (reinstated with a Buy at Goldman), PG +0.5% (upgraded to Outperform from Market Perform at BMO Capital).

-

Euro Pacific Capital võtab Bloombergis sõna

Analüüsimaja prognoosib, et kulla hind tõuseb aastaga veel 50% ehk ca $2,000 untsi kohta. Alloleval graafikul on kujutatud Föderaalreservi bilansis kajastuvad väärtpaberid, mille väärtus on üle $2 triljoni, ning kulla hind. Sisuliselt tugineb öeldu Goldman Sachsi prognoosidel. Goldman Sachs prognoosib, et QE2 käigus “prindib” Föderaalreserv ca $500 miljardit.

-

USA indeksite futuurid jõudnud hetkel -0,1% punasesse

Euroopa turud:

Saksamaa DAX -0,30%

Prantsusmaa CAC 40 -0,63%

Suurbritannia FTSE100 -0,61%

Hispaania IBEX 35 -0,72%

Rootsi OMX 30 -0,17%

Venemaa MICEX -0,58%

Poola WIG -0,13%Aasia turud:

Jaapani Nikkei 225 -0,99%

Hong Kongi Hang Seng +0,26%

Hiina Shanghai A (kodumaine) +3,13%

Hiina Shanghai B (välismaine) +2,02%

Lõuna-Korea Kosdaq +0,19%

Austraalia S&P/ASX 200 -0,21%

Tai Set 50 -0,87%

India Sensex 30 -0,32% -

Rev Shark: Wait and See

10/08/2010 7:25 AM"Not only our future economic soundness but the very soundness of our democratic institutions depends on the determination of our government to give employment to idle men."

-- Franklin D. Roosevelt

For the last three weeks, we have had very choppy albeit positive market action. We struggled mightily to make it through 1,150 for quite a while, and then just when everyone was leaning the wrong way, we pulled off a classic break out on Tuesday. Since then, we haven't been able to follow through, and, in fact, we had some particularly negative action in big-cap momentum names, but the technical picture is still positive as we head into the jobs numbers this morning.

The consensus estate for nonfarm payrolls is a gain of zero jobs, while the more important private payroll numbers is expected to be a gain of 75,000 or so. The unemployment rate should tick up slightly to 9.7%

As I discussed yesterday, the tricky thing about economic news right now is that there is intense focus on quantitative easing. The Fed has made it quite clear that they are ready to start buying up debt, and after the straight-up move in 2009, everyone is very aware of what that influx of cash can do to the market.

The problem is that we have been very intently pricing in QE 2 for a month now. Fear of a double-dip recession was rampant in August, but since then, it has been all about how we don't want to fight the Fed and its bazooka full of cash.

The jobs report this morning is going to give us some insight into the markets view of QE 2. There has been increasing discussion about how it many not be the panacea that many seem to think it is. It is also so well anticipated this time that it's impact is being priced in already.

If the job numbers is weak this morning I expect buyers to jump in as they will be more confident that QE will roll out in the next 6 weeks or so. If the number is strong there will be some celebration that maybe the economy isn't the complete disaster so many believe it is. It is going to take more than just some minor beats to really excite this market especially when many are hoping that continued bad economic news will help to ensure political gridlock in Washington after the November election.

I have no inclination to make bets on the numbers, so let's wait and see what they are and then we can work on our positioning.

-

Allied Irish Banks: S&P lowers Long-Term Rating to 'BBB+' from 'A-' with negative outlook on weakened prospects; seems probable that AIB will likely become majority owned by the state

-

Bank of America to stop foreclosure in all 50 states- CNBC

-

AlariÜ - kuidas ja kas see uudis Bank of America aktsiakursile mõjuma peaks?

-

DOW-l 11000 punni tehtud. Sellise makro peale uued tipud?

-

Jah, sest selline macro tähendab kindlamat QE2 tulekut.

-

Isegi kui QE2 tuleb, siis selle likviidsuse najal saavad pigem toorained uued tipud ja lõpuks lastakse ikkagi aur välja. EUR/USD liikumine kahtlemata väga paeluv ja turgu suunav. Kust ja millisel moel, see saab olema huvitav.

Austus turu trendile, kuid siit turuga kaasa minna on üsna riskantne tegevus. Kindlasti on ukse taga koputamas lähiajal terav kasumivõtt, mis võib saada katalüsaatori tulemushooajal.

Täna ootaks turul päeva lõpuks kerget müüki, kuigi hetkel turg väga tugev. Tänasest hakkab IMF-i ja Maailmapanga igaaastane konverents 8-10. okt, mida ei tohiks alahinnata. Sellist eksporti soosivat valuuta lõhkumist tõenäoliselt kauaks ei jätku. -

Peabody Energy (BTU): Downgrade details

As mentioned earlier BMO Capital Markets downgraded BTU to Market Perform from Outperform and raises their tgt to $56 from $49 following the recent share price appreciation, BTU shares trade at a premium to the group on a forward EV/EBITDA multiple, which is in line with the historic premium to the group.

Päris hea reitingu langetus, kus tõstetakse hinnasihti üle 10%.

Aktsia +1.89% tõusus $51.81 tasemel -

Finants veidi järgi andmas, KBE 0.72% languses vs SPY 0.40% tõusu.

-

Turul nii käive, kui müügihuvi peale 17:30 täielikult puudub ja vähehaaval liigutakse üha uutesse päeva tippudesse.

-

Viimase 5 minutiga toodi turg siiski kergelt madalamale.