Börsipäev 13. detsember

Kommentaari jätmiseks loo konto või logi sisse

-

Aeg on jõudnud sinnani, kus investeerimispangad hakkavad oma neljanda kvartali majandustulemusi teatavaks tegema. Goldman Sachs (GS), Bear Stearns (BSC) ja Morgan Stanley (MS) on pildil järgmine nädal, esimesena teeb täna otsad lahti Lehman Brothers (LEH).

Kui kolmanda kvartali järel oodati, et augustiga jäid suuremad probleemid selja taha, siis november tundub veelgi hullem. Kusagilt jäi silma, et tänaseks on maha kirjutatud juba $100 miljardi väärtuses laene ning Lehman Brothers ise kandis eelmise kvartali jooksul maha $1.3 miljardi väärtuses laene.

Novembris suurenes hapuks läinud hüpoteeklaenude osakaal rekordtasemeni, mis tähendab, et Lehman ei pääse ka seekord kinnisvaralaenudega tagatud võlakirjade hindamisest turu järgi madalamaks. Lisaks varade vähenemisele on Fixed Income segmendis oodata olulist kauplemistulude vähenemist, mis teiselt poolt survet avaldab. Samas on ennustusi keeruline teha, sest erinevalt teistest pankadest ei anna LEH investoritele hoiatusi. Näiteks BSC ja MS on öelnud, et probleemid on vahepeal süvenenud ning uusi laene tuleb kuludesse kanda, GSi seevastu mahakirjutamiste suurenemist ei oota.

Lehman teatab oma tulemused enne turgude avanemist ja $4.27 miljardi tulu juures oodatakse ettevõttelt aktsiapõhist kasumit $1.43. Kuigi mõnel pool arvatakse, et põhi on tehtud ja probleemid juba sisse arvestatud, siis loogilisem tundub, et vaikelu turul kestab edasi, mis tähendab riskantsemate portfellide puhul jätkuvaid allahindamisi ka järgmisel aastal. Kinnisvaraturg on nõrk ja defaultide arv alles kasvab, mis optimismi just ei sisenda.

-

Lehmanni (LEH) konverentsikõne algab kell 10.00 ET ehk siis pool tundi pärast börsi avanemist. Kuulata saab seda siit.

-

Morgan Stanley näeb 2008. aastal arenemas järgnevaid trende:

1) prognoosivad –5% kuni –10% kasumikasvu finantssektoris ning 0% kasumikasvu S&P 500 ettevõtetele.

2) aeglustumist arenenud riikides väljaspool USAd – Eurotsooni prognoositav kasv 1.6% ja Jaapanis vähem kui 1%

3) lõdvem globaalne rahapoliitika – FED funds target 3.5% tasemel suveks , BOE langetab intressimäärasid veelgi ning ECB langetab määrasid 2008. aasta esimeses pooles

4) ralli dollaris, mida toetab nõrgenev kasv väljaspool USAd ning soov võtta vähem riski

5) ajutine toorainehindade kerkimise aeglustumine kuna globaalne kasv aeglustub, USD tugevneb ja spekulatiivsed rahavood aeglustuvad

Üldiselt on tegu commodity pullidega: Our top picks for 2008 include soybeans, cotton, aluminum, gold, long-dated sugar and long-dated natural gas. -

08:10 LEH prelim $1.54 vs $1.42 First Call consensus; revs $4.4 bln vs $4.26 bln First Call consensus - Bloomberg

aga kõiki huvitab vist rohkem write down summa -

Fixed Income Capital Markets reported a decrease in revs of 60%, due to the very challenging markets experienced during the period

See on päris suur langus. LEH teatas book valuest aktsia kohta $39.45, mis teeks P/BV ca 1.55. Eeldades, et asjad niipea paranemas ei ole, siis see väga odav ei olegi. -

Capital Markets net revenues decreased 10%, Fixed Income Capital Markets reported a decrease in revs of 60%, due to the very challenging markets experienced during the period. Equities Capital Markets reported record net revenues of $1.9 bln, more than double the $900 mln reported in 4Q06.

Oliver, mulle lausa meeldib Su oskus tekstist ikka Sinu karust vaadet toetavad lõigud välja noppida :)

Equities Capital Markets reported record net revenues of $1.9 bln, more than double the $900 mln reported in 4Q06.

tulud 2 korda üles ei ole muidugi midagi -60% langusega võrreldes? -

Siiani on panganduse osas see karusema poole noppimine sihile viinud :)

Fixed income oli see, mis varasemalt tugevat kasvu näitas ning nüüd ollakse mõneks ajaks sellest kasvust ilma, mistõttu seda ka jäglin. Mis puutub Equities Capital Markets segmenti, siis customer flow activities on tulnud ka volatiilsest turust ja private eq diilidest, mille hoogustumist ma praegustelt tasemetelt väga ei näe. -

tänane makro on küll esmapilgul raskelt tõlgendatav

novembri jaemüük oodatust parem, kuid PPI ka oluliselt kõrgem

negatiivse poole pealt siis inflatsioonihirm ja positiivse poole pealt tarbija suhteline tugevus kõigele vaatamata -

Inflatsioonihirm võiks ikkagi retaili üle kaaluda, eriti viimast Fedi sõnastust vaadates, kus inflatsioonile ka taaskord vihjati

-

Punane värv selgelt domineerimas...

Saksamaa DAX -1.17%

Prantsusmaa CAC 40 -2.14%

Inglismaa FTSE 100 -2.05%

Hispaania IBEX -1.93%

Venemaa MICEX -2.02%

Poola WIG -1.85%

Aasia turud:

Jaapani Nikkei 225 -2.48%

Hong Kongi Hang Seng -2.72%

Hiina Shanghai A (kodumaine) -2.70%

Hiina Shanghai B (välismaine) -2.06%

Lõuna-Korea Kosdaq +0.57%

Tai Set +0.03%

India Sensex -1.33%

-

Long-Term Optimism,

Short-Term Caution

By Rev Shark

RealMoney.com Contributor

12/13/2007 8:08 AM EST

The pessimist complains about the wind; the optimist expects it to change; the realist adjusts the sails.

-- William Arthur Ward

The market's failure to embrace the Fed's scheme to increase liquidity in the banking system casts a gloomy pall as we enter the last few weeks of the year. If the mighty Fed, with all its tools and power, can't contain fears over subprime debt problems and shore up investor confidence, what's going to reassure this market?

There is no shortage of armchair pundits who are willing to offer advice to Ben Bernanke and his staff, but what you really have to wonder is whether the economic cycle is destined to play out like it always does, no matter how much we flail about for solutions. Trying to stop an economic contraction as real estate loses trillions in values and billions in debt is written off is like trying to prevent the seasons from changing. The economic system is going to purge itself of its problems one way or another, and not even all the central banks in the world can stop it.

That sounds rather depressing, but the key is how you look at it. In the long run, the cycle will turn up again like it always does, and that should keep us optimistic. The economic cycle will create opportunities if we are patient and aren't blinded by the short-term gloom and despair.

In the shorter term, we need to adjust to a more difficult environment. That means staying vigilant and protecting capital.

There are going to be plenty of market pundits anxious to tell us how terrible things are going to get before they get better. We are going to hear predictions that we will undergo the worst economic crisis we have ever seen. That's possible, but it seldom works that way. Some people glory in that sort of pessimism, but for most people, it drains them of motivation and makes them forget about the opportunities that will eventually arise.

The healthiest approach to the market for most investors is to be a long-term optimist while being short-term vigilant. As long as you are confident that things will eventually get better -- as I am -- you will have the motivation and drive to navigate the angry market seas we presently face.

And angry they are at the moment. The mood is sour, the technical conditions are poor and few positive catalysts exist. Market players are lacking confidence and that tends to feed on itself.

We have a poor open shaping up as overseas markets rejected the Fed liquidity move and increased their worries over the subprime issues. The market is flailing around as it looks for some real solution to the bad-debt mess, and it isn't finding one. Stay vigilant and defensive and let this play out.

--------------------------

Ülespoole avanevad:

In reaction to strong earnings/guidance: MATK +13.2%, ADCT +8.7% (also upgraded to Buy at Merriman), JOSB +6.6%, GXDX +6.2% (also initiated with Outperform at Cowen), KMGB +3.6%, HAYN +3.3%, CIEN +2.6%, MDZ +1.1%, LII +1.1%, HON +1.0%... M&A news: MGI +27.5% (to be acquired by EEFT for $20/share)... Other news: RIGL +75.0% (demonstrates significant improvement in rheumatoid arthritis in Phase 2 clinical study), SVNT +45.2% (meets pre-specified primary efficacy endpoint in two replicate Phase 3 studies ), DEPO +21.2% (says Court grants motion for Summary Judgement of patent infringement against IVAX), DOW +7.8% (DOW and Petrochemical Industries announce plans to form a 50/50 joint venture in global petrochemicals co) PSPT +7.5% (Board rejects IPVG and AO Capital Partners unsolicited proposal of $15/share), VNDA +4.0% (presents Phase 3 iloperidone efficacy data), XMSR +3.7% (members of US House Antitrust Panel express concern over merger - Reuters), UMBF +3.2% (will replace EDO in S&P SmallCap 600), RATE +2.4% (initiated with Neutral at BofA), CPSL +2.0% (announces that it has new independent registered public accounting firm). Analyst upgrades: ESLR +4.1% (initiated with Buy at UBS), JRCC +3.9% (initiated with Buy at UBS), RATE +2.4% (initiated with Neutral and $55 tgt at BofA), CYNO +2.2% (upgraded to Buy at Citigroup), GA +2.0% (initiated with Buy at UBS).

Allapoole avanevad:

In reaction to weak earnings/guidance: ASYS -17.8% SCSS -15.7% (Discloses in its 8-K that sales profits will fall short of previous guidance), COST -6.3%, VITL -6.2%, CKR -4.7%, LEH -2.1%, CPII -1.3%, NSPH -1.1%... Other news: NBIX -46.3% (receives approvable letter for indiplon capsules with additional safety and efficacy data required by FDA), BIIB -27.5% (completes review of strategic alternatives; did not receive any definitive offers), ADPI -23.3% (provides update on lawsuit -- jury found PDHC or ADPI liable for breach of the service agreement and awarded compensatory damages of $9.4 mln; this follows yesterday's 27% sell-off in the stock), WSTL -8.5% (receives notice of SEC investigation), SCA -8.3% (Fitch reviewing its AAA ratings), ELN -6.2% (in response to BIIB announcement, co reaffirms commitment to Tysabri), ACH -5.3% (still checking), LIHR -5.1% (cuts production forecast by 7% to 700k oz - DJ), POT -4.3% (files for a $2 bln debt securities shelf offering), BIDZ -4.3% (presented at Wedbush conference after the close, issues guidance), QCOM -2.4% (judge issues ruling saying NOK does not infringe QCOM in patent infringement complaint, also downgraded to Neutral at Merrill), MT -1.3% (to increase stake in China Oriental), AGU -1.0% (prices secondary offering at $58)... Analyst downgrades: RIO -3.6% (hearing downgraded to Neutral at tier-1 firm), WM -3.1% (downgraded to Sell at BofA), COF -2.6% (downgraded to Hold at Jefferies), RHT -2.2% (downgraded to Sell at BofA), PMCS -1.4% (initiated with Sell at BofA), CME -1.0% (hearing removed from Conviction Buy list at tier-1 firm). -

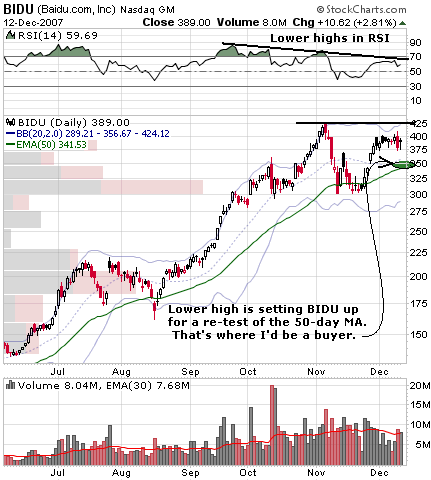

Ma panen RM'ist siia ühe graafiku BIDU kohta: