Börsipäev 15. september

Kommentaari jätmiseks loo konto või logi sisse

-

Päev algav taas sõnumitega Jaapanist, kus riigi keskpank on viimaks pannud oma sõna maksma ning hakanud müüma jeeni esimest korda pea kuue aasta jooksul, et vähendada valuuta viimase aja kallinemisest tingitud negatiivset survet riigi eksportijatele ning majanduskasvule.

USD/JPY

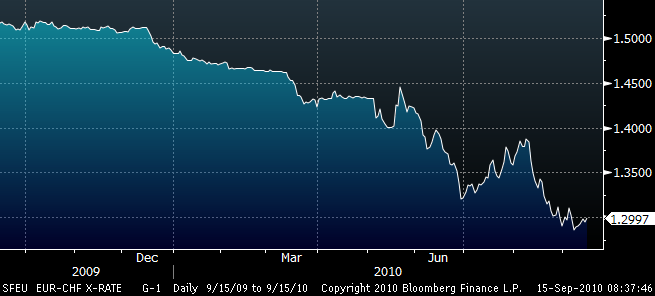

Sarnast võitlust tuuleveskitega on aasta algusest aga teatavasti pidanud Šveitsi keskpank, kes on kulutanud üüratuid summasid, et üritada takistada kapitali massiivset sissevoolu ning koduvaluuta kallinemist selle tagajärjel. Lõpptulemusena tuli esimesel poolaastal leppida 14 miljardi frangi suuruse kahjumiga ja nüüd vist on sellest plaanist üldse loobutud, mistõttu on küsitav kui efektiivseks osutub ka Jaapani keskpanga tegevus, kui maailmamajanduse kasv aeglustub ja investorid eelistavad edasi riskantsematest varaklassidest eemale hoida.

EUR/CHF

-

Makrokalendrit vaadates Euroopast olulist infot oodata pole (eurotsooni augustikuu lõplik inflatsiooninäit tõenäoliselt kinnitab esialgset 1,6%list YoY hindade kallinemist), USA-s aga avaldatakse kell 15.30 septembrikuu Empire State manufacturing index, kell 16.15 augustikuu tööstustoodangunumbrid ja tööstusvõimsuse määr. Kell 17.30 tuleb iganädalane toornaftavarude raport.

-

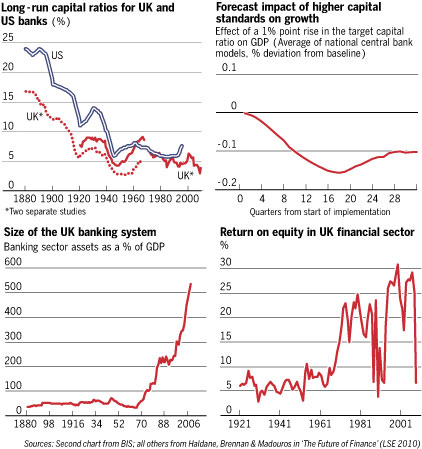

FT kolumnist Martin Wolf annab oma nägemuse Basel III nõuetest (Basel: the mouse that did not roar), mis tema meelest ei vii meid eesmärgini luua turvalisemat ja väiksemat finantssüsteemi ning enne kui ettenähtud kapitalinõuded kehtima jõuavad hakata, on maailm tõenäoliselt läbinud veel ühe või kaks finantskriisi.

Am I being too harsh? “Global banking regulators ... sealed a deal to ... triple the size of the capital reserves that the world’s banks must hold against losses,” says FT. This sounds tough, but only if one fails to realise that tripling almost nothing does not give one very much.

-

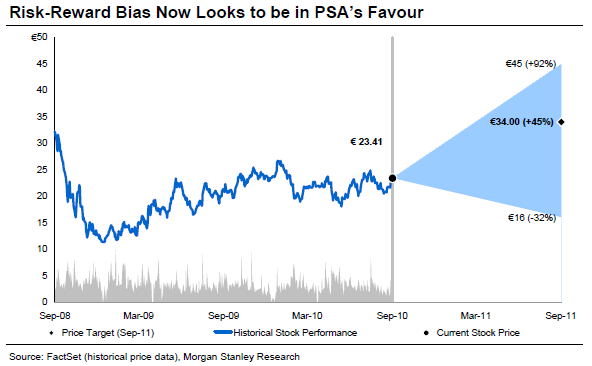

Morgan Stanley on eile tõstnud Peugeoti soovituse tasemelt "underweight" tasemele "overweight" ning kinnitanud autotootja hinnasihiks 34 eurot (varasema 27 euro asemel). Eelkõige usutakse, et kui 2010. aastal on domineerinud nõudlus luksbrändide järgi, aidates Saksa autotootjatel saavutada rekordilist kasumlikkust, siis edaspidi antud segmendi upside pigem hääbub ning tähelepanu liigub underperforminud masstootjatele. Morgani arvates on mure raha-romu-eest programmide raames tekkinud hinnasõja pärast üleliialdatud, kuna soodustused on jäänud selle aasta sees suhteliselt stabiilseks. Sestap kergitatakse Peugeoti 2011.a EPS-i üsna märkimisväärselt 2,5 eurolt 4,3 eurole (mis on nüüd ühel pulgal konsensusega). Seega antud prognoosi põhjal kaupleb aktsia hetkel 5,6x 2011 kasumil ning ca 40% undervalued võrreldes Morgan Stanley õiglase hinnaga.

-

Eurotsooni tarbijahinnaindeks tuli vastavalt ootustele nii aastases (1,6%) kui kuulises lõikes (0,2%).

-

Šveitsi ZEW ootusteindeks kukkus eelmise kuu 9,1 pealt -5,1 punktini. Frank kaupleb dollari vastu 0,85% madalamal 1,0041 taseme juures.

-

Suurbritannia ILO töötusmäär jäi ootuste kohaselt püsima 7,8% peale. Töötuabiraha taotlejate arv aga tõusis 2300 inimese võrra, kuigi oodati vähenemist 3000 inimese võrra. Naelsterling kaupleb dollari vastu $1,5500 taseme juures.

-

RWI majandusinstituut tõstis Saksamaa käesoleva aasta majanduskasvu prognoosi juunis oodatud 1.9% pealt 3.4% peale. 2011. aasta majanduskasvu ootus kergitati 1.7% pealt 2.2% peale.

-

Saksamaa kindlustuskompanii Allianz tegi uurimuse globaalse jõukuse jaotumise kohta, mille kohaselt on vaesed lõpuks ometi saamas jõukamaks kiiremini kui rikkad.

Raportis tuuakse välja, et 39% kogu maailma jõukusest on ameeriklaste kätes (€101 762 väärtuses aktsiaid, hoiuseid ja kindlustust per capita). Lääne-Euroopas asub 31% kogu varadest. Siiski on ameeriklaste jõukus vähenemas. Nimelt 2007. aastast on nende varade väärtus tänu aktsiaturgude langusele vähenenud 12%. Kreeklaste jõukus on vähenenud veelgi rohkem -- 14%. Teiste suuremate kukkujate seas on Hispaania, Jaapan ja Šveits. Šveits on samas maailma jõukaim maa, kus on inimese kohta varasid €167 731 väärtuses. Raporti kohaselt kasvas 50 jälgitud riigi jõukus eelmisel aastal 7,5%, kuid kriisieelse tasemega võrreldes ollakse veel 4% miinuses.

Lisaks tuuakse raportis välja, et maailma vaesemad piirkonnad on alates dot-com mulli lõhkemisest kasvatanud varasid kiiremini kui rikkamad piirkonnad. Ida-Euroopa jõukus on viimase kümnendi jooksul kasvanud keskmiselt 16% aastas. Aasia (v.a Jaapan) ja Ladina-Ameerika jõukus on kasvanud samal perioodil keskmiselt rohkem kui 12%. USA ja Euroopa kasv on olnud 3% või alla selle. Vaadeldud 50 riigi puhul oli 4,7 miljardist inimesest üle ühe miljardi jagu inimesi, kelle varade suurus oli suurem kui €5300 (siia hulka ei arvestatud kinnisvara).

Erinevus vaeste ja rikaste riikide vahel on endiselt suur. Samas ei pea paika väited nagu see vahe on pidevalt suurenemas. Allianzi raporti kohaselt on rikastel riikidel inimese kohta 45 korda rohkem varasid kui vaestel riikidel, kuid kümne aasta eest oli erinevus 135-kordne.

-

September NY Empire Manufacturing 4.10 vs 6.40 Briefing.com consensus; August 7.10

ES võttis selle peale suuna alla ning kaupleb ca 0,4% punases

-

Gapping down

In reaction to disappointing guidance: AKS -3.0%, STLD -2.3% .Select financial related names showing weakness: DFS -1.9% (reported card metrics), DB -1.8%, WFC -1.3%, BCS -1.3%, HBAN -1.3% (trading ex dividend), MS -1.0%.

Select oil/gas related names trading lower: HAL -1.9%, BP -1.3%, TOT -1.2%, MEE -1.2%, SD -1.0%, STO -1.0%, CHK -0.9%.

Other news: NBIX -10.4% (announces top-line results of corticotropin releasing factor antagonist GSK561679 for treatment of major depressive disorder; Study did not demonstrate a treatment effect compared to placebo), TEAM -10.1% (amended stock purchase agreement with Jacobs Engineering Group lowers price of co's Government Solutions to $43 mln from $59 mln), AU -4.5% (prices equity offering and mandatory subordinated convertible bonds offering), EPB -4.0% (announces public offering of common units), BZH -3.6% (updates expectations for certain FY 2010 operating data ), ARI -3.4% (announces proposed common stock offering of 6 mln shares of common stock), ARMH -1.5% (still checking), KRA -1.2% (light volume; files to sell 8 mln shares of common stock through selling shareholders), X -1.1% (trading lower following STLD and AKS guidance), NEE -0.9% (ticking lower; announced today that it intends to sell $350 million of equity units).

Analyst comments: MU -3.7% (downgraded to Neutral from Buy at Goldman), MXIM -2.9% (downgraded to Sell from Neutral at Goldman), TYC -2.5% (downgraded Market Perform from Outperform at Bernstein), AIV -2.2% (downgraded to Neutral from Outperform at Macquarie; tgt $12), NOK -1.4% (downgraded to Sell from Hold at Citigroup), IR -1.3% (initiated with Sell at Citigroup).

Gapping up

In reaction to strong earnings/guidance: PLL +5.2%, KOOL +4.3% (thinly traded; currently reades under KOOLD), LIWA +3.6% (ticking higher on light volume), MPWR +2.5% (updates guidance; also Standard & Poor's confirms MPWR will be added to the S&P 500).M&A news: CYPB +25.4% (Ramius Commences cash tender offer for Cypress Bioscience at $4.25/Share).

Other news: HRBR +61.7% (reports Apoptone for prostate cancer shows a partial overall response; drug was well tolerated at all doses with no overt dose-limiting toxicities observed), SVNT +22.0% (U.S. Food and Drug Administration approved Krystexxa), UTSI +7.3% (wins contract from Sichuan Radio and TV to build its integrated network broadcasting control platform ), GTXI +4.8% (light volume; GTx-758 being developed to treat advanced prostate cancer, induced medical castration in a Phase II PK/PD Clinical Trial), LVLT +3.2% (Prices offering of $175 mln of convertible senior notes), MASI +3.1% (announces Japanese Ministry of Health, Labor and Welfare regulatory clearance of its noninvasive and continuous hemoglobin measurement), NOVL +2.9% (ticking higher on article that suggests the co may be planning to sell itself in two part sale), TM +1.9% (traded higher overseas), MA +1.1% (Directors approves $1.0 bln Class A share repurchase).

Analyst comments: NETL +4.9% (upgraded to Buy from Neutral at UBS), LEAP +2.3% (Poison pill preempts potential hostile action - Auriga ), FRO +2.2% (initiated with an Outperform at Wells Fargo), RDC +1.0% (upgraded to Buy from Neutral at UBS).

-

Kuidas Wall Streetil asju aetakse - link (nägin ise seda juba nädalaid tagasi, kuid meenus täna uuesti).

: )

-

USA futuurid on enne tööstutoodangu numbrit hoidmas kerget miinust. ES -0,36%, YN -0,33%, NQ -0,23%%. Nafta kaupleb -2,36%% @ 75,0 USD ja kuld -0,2% @1269 USD.

Euroopa turud:

Saksamaa DAX -0,67%

Pantsusmaa CAC 40 -0,89%

Suurbritannia FTSE100 -0,51%

Hispaania IBEX 35 -1,20%

Rootsi OMX 30 -0,46%

Venemaa MICEX -0,39%

Poola WIG -0,21%Aasia turud:

Jaapani Nikkei 225 +2,34%

Hong Kongi Hang Seng +0,14%

Hiina Shanghai A (kodumaine) -1,34%

Hiina Shanghai B (välismaine) -0,68%

Lõuna-Korea Kosdaq -0,11%

Tai Set 50 -0,19%

India Sensex 30 +0,80% -

Rev Shark: Still in Good Shape

09/15/2010 7:43 AMA government that robs Peter to pay Paul can always depend on the support of Paul.

-- George Bernard ShawMarket momentum cooled slightly on Tuesday as the S&P 500 confronted major overhead resistance at the August highs. If we can push through 1130 or so, the S&P 500 will be at the highest levels since May, but we have gone up almost in a straight line since 1050 and are looking a bit tired.

Overall the market is not in bad shape at all. We are a bit extended and need some consolidation, but there has been sustained momentum that has helped to push us through some key resistance levels like the 200-day simple moving average. If we can rest a little and digest recent gains, we'll be in good shape for an assault on those August highs.

The economic news has generally been better than expected, with the retail sales report yesterday being the latest positive data point. However what is probably helping to drive this rally most is the expectation that the Federal Reserve will engage in further quantitative easing. The Fed has been sending signals it is open to the idea of ramping up its purchase of bonds in one way or another, and the market is very aware of what that flood of liquidity did for equities in 2009 and early 2010.

There is an old saying that one shouldn't fight the Fed, and 2009 was a great example of why that's the case. Even though there never has been any tremendous economic improvement since the bottom in March 2009, the market went straight up for over a year, primarily because of the easy-money policy of the Fed. When there is flood of cheap money sloshing around, a great amount of it is going to be parked in the stock market simply because there aren't a whole lot of other choices.

Ultimately running the government printing press constantly will carry a cost, but that longer-term concern is outweighed by the force of cash looking for a place to go. We may pay a price down the road, but that has not been a good reason to battle against liquidity in the short term.

So if you are wondering what the driving force is behind this recent move, look to the Fed. More important, keep in mind the lesson we learned -- when the Fed is running the printing press, the market can easily do things we don't expect technically, like go up in "V"-shaped fashion on diminishing volume.

I don't want to dwell too much on macroeconomic considerations, because in the end we always need to focus on the action in individual stocks -- and lately that action has been quite good. There have been some impressive pockets of momentum, individual stock-picking has worked well and the bears just haven't been able to make much progress lately.

At this point, we are extended and could use some rest, but we can easily afford a few soft days. In fact, it would be quite healthy if we churned and built up some bearishness. I have seen a number of comments lately about how market players are too negative, but I'm not seeing that reflected in the high level of speculative action in the market. If there is a lot of bearishness, it is mostly coming from pundits in the media rather than traders who are trying to make a buck.

The big picture looks pretty good, but with some major overhead resistance nearby and overbought conditions, we shouldn't be at all surprised to see a bit of softness in the near term.

We have some slight weakness in the early going. Japan was up big on a move to weaken the yen, but Europe is red and we are set to open slightly negative

-

August Industrial Production +0.2% vs +0.3% Briefing.com consensus, prior revised to +0.6% from +1.0%;

Capacity Utilization 74.7% vs 75.0% Briefing.com consensus, prior 74.6%

-

nafta kaupleb pisut kõrgemal pärast datat -1,5% @ 75,63

Dept of Energy reports that:

- Crude oil inventories had a draw of 2489K (consensus is a draw of 2,500K)

- Gasoline inventories had a draw of 694K (consensus is a draw of 500K)

- Distillate inventories had a draw of 340K (consensus is a build of 600K)

- The change in refinery utilization was -0.60% (consensus was -0.78%)

-

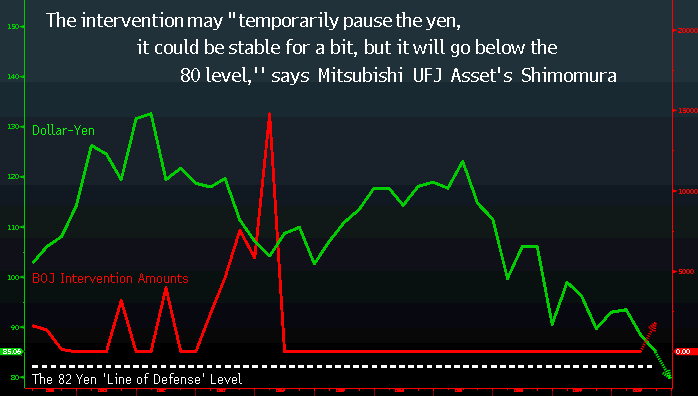

Kui jätkata teemaga, millega Erko hommikul algust tegi, siis Mitsubishi UFJ Asset Management Co. prognoosib, et keskpanga poolne otsus müüa jeeni „peatab valuuta kallinemise dollari suhtes vaid mõneks ajaks“. Selline tees põhineb alloleval graafikul, kus on ära toodud BOJ jeeni müük/ost ning jeeni kursi liikumine dollari suhtes. Mäletatavasti müüs BOJ 2003. aastal 20.4 triljoni jeeni ($240 miljardit) ning veel 14.8 miljardit jeeni 2004. aasta esimeses kvartalis (alloleval graafikul on seda hästi näha), kuid tulemuseks oli jeeni kursi stabiliseerumine, mitte odavnemine. Mitsubishi UFJ Asset Management 2010. aasta lõpu USD/JPY prognoosiks on $78.

-

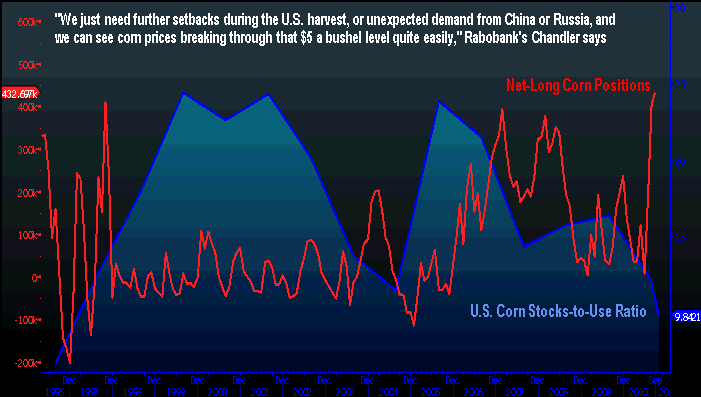

Meedias on palju räägitud nisust, mille hind augusti alguses üle $800 tõusis. Kallinenud ei ole aga ainuüksi nisu hind. All on 30 päeva maisi hinnagraafik (detsembrikuu futuur), mis on selgelt positiivse trendiga.

Sisuliselt on tõusu taga olnud riskifondid ning spekuleerijad, kes on tähelepanelikult jäginud varude ning maisi tarbimise suhet. USA põllumajandusministeeriumi sõnul on maisi varude ja tarbimise suhe langenud käesoleval aastal 15 aasta madalamale tasemele ehk 9.8% peale. Hea ülevaate annab öeldust allolev graafik, millel on ära toodud ka pikkade-lühikeste positsioonide suhe (net-long positions). Rabobank International’i sõnul on vaja vaid mõnda USA madalat saaki ning Hiina või Venemaa kasvavat nõudlust puudutavat uudist ning mais kaupleb üle $500. Olgu siinkohal öeldud, et USA moodustab ca 50% maailma maisi ekspordist.

-

Mäletan, et viimane selline toiduainete kallinemine lõppes finantskollapsiga. Ja alles paar aastat tagasi.

Mitte, et tahaksin näha siin seoseid. -

"Mitsubishi UFJ Asset Management 2010. aasta lõpu USD/JPY prognoosiks on $78."

Whooooooooooooooooooooooooooooooaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaa!

:-DDD -

Paistab, et kellelgi pole enam usku keskpankade tegevusse, sest alla 79 targetitega on väljas ka Goldman ja BofA

-

Järgmistel majadel on telepilti pääsemisega juba keerulisem- tuleb pakkuda alla 70 :-)

-

jah...siinkohal peaks tegelikult uurima Saxo panga prognoose :)

-

Eks üheksandal kuul on kõik targemad kui esimesel kuul....aga siin on väike meenutus Saxo mullu detsembris tehtud 2010. a prognoosidest.

5) USDJPY to reach 110

Although the downturn in the USD is rooted in irresponsible fiscal and monetary policies, we believe that the USD could snap back at some point in 2010 because the USD carry trade has been too easy and too obvious for too long. At the same time, the JPY is not reflecting economic reality in Japan, which is struggling with a huge debt burden and ageing population.