Börsipäev 1. detsember

Log in or create an account to leave a comment

-

Aasia indeksid on päeva põhjadest kõrgemale liikunud ning sulgunud valdavalt plusspoolel tänud dollari nõrkusele, mis toetab toorainesektorit ning ridamisi avaldatud PMI näitajatele, mis indikeerivad majandusaktiivsuse jätkuvat kasvu mitmel pool Aasias. Vastupidiselt kardetule kerkis Hiina töötleva tööstuse novembrikuu PMI 54,7 pealt 55,2 peale, Lõuna-Korea oma 46,8 pealt 50,2 peale, Taiwanis 48,6 pealt 51,6 peale ning Indias 57,2 punktilt 58,4 punktile.

Ka eurotsoon avaldab täna oma lõpliku PMI (kell 11.00), mis ei tohiks esialgse hinnanguga võrreldes väga suurt üllatust pakkuda. Suurbritannia novembri PMI avaldatakse seevastu esimest korda (kell 11.30). USA-s jälgitakse suurema huviga ADP tööjõuraportit (kell 15.15) ja novembri ISM indeksit (kl 17.00).

Euroopa indeksite futuurid indikeerivad hetkel avanemist 0,6-0,7% kõrgemal, USA futuurid liiguvad aga 0,3-0,4% plusspoolel.

-

Saksamaa jaemüük kasvas oktoobris 2,3% vs oodatud 1,2%. Aastasel baasil langes jaemüük 0,7%, kuigi oodati 1,3% kasvu.

Saksamaa PMI tootmisindeks tuli 58,1 vs oodatud 58,9 punkti.

Eurotsooni PMI tootmisindeks tuli 55,3 vs oodatud 55,5 punkti.

EUR/USD +0,73% ja kaupleb hetkel 1,3076 juures. -

Tänane Wall Street Journal kirjutab, et Google (GOOG) on ülevõtu teemal läbirääkimisi pidamas firmaga Groupon, mis pakub oma veebilehel igapäevaselt erinevate firmade sooduspakkumisi.

Grouponi tehing võib toimuda suurusjärgus $5 + miljardit ja tähistaks Google`i jaoks suurimat ülevõttu üldse.

Ainult paar aastat tegutsenud ettevõtte on juba tõmmanud endale nii võimalike kosilaste kui ka kloonijate tähelepanu. Firma ülevõtuga saaks Google kaasa ka ca 12 miljoni kliendi andmed ning võimaluse saada jalg kohaliku reklaamituru ukse vahele.

-

Finacial Times'i eilne artikkel räägib sellest, et Euroopa keskpanga juht Jean-Claude Trichet sõnul võib keskpank jätkata Euroopa riikide võlakirjade ostmist. Trichet "hoiatas" turge, et nad ei alahindaks Euroopa pühendumust eskaleeruva võlakriisi lahendamisel. Programmiga tehti algust selle aasta maikuus ja siiani on keskpank ostnud €67 miljardi eest valitsuste võlakirjasid.

Saksamaa keskpanga juht Axel Weber on avalikult selle programmi vastu sõna võtnud.

-

Suurbritannia PMI tootmisindeks ületas tugevalt ootusi: 58,0 vs oodatud 54,7 punkti. Naelsterling sai kena tõuke ja kaupleb dollari suhtes 0,4% kõrgemal $1,5620 juures.

-

Euro on täna korralikult taastumas: EUR/USD +0,98% (1,3109), EUR/AUD +0,40% (1,3592), EUR/CHF +1,06% (1,3164), EUR/JPY 1,05% (109,78).

-

Portugal müüs oksjonil €500 miljoni eest 12-kuulisi võlakirjasid tulususmääraga 5,28% vs novembrikuu oksjoni 4,81%. Nõudlus samas kasvas: nõudlus ületas pakkumist 2,5 korda vs eelmise oksjoni 1,8.

-

LA Timesi andmetel lükkub Boeingu (BA) esimese 787 Dreamlineri kättetoimetamistähtaeg veelgi edasi. Ettevõtte kommertslennukite divisjoni juht Jim Albaugh ütles, et Boeingul läheb veel aega, et välja selgitada põhjused ja paranda viga lennuki elektripaneelis, mis eelmisel kuul toimunud testlennu ajal põhjustas tulekahju.

Jim Albaugh said Boeing would take more time to fully understand and fix a fault in an electrical panel that triggered a fire during a test flight last month, grounding Dreamliner trials. "There will be an impact with the first delivery," Albaugh said when asked whether the 2011 first-quarter target would slip. "I think it will be after that."

-

MBA hüpoteeklaenude taotlused (26. november) -16,5%.

-

Novembri ADP oluliselt parem, lisaks pakutakse positiivset üllatust eelmise kuu numbrites

November ADP Employment Report 93K vs 58K Briefing.com consensus

October ADP Employment revised to 82K from 43K -

Gapping up

In reaction to strong earnings/guidance: LTON +7.1% (thinly traded), OVTI +6.0%.

M&A news: MIGP +46.9% and UFCS +11.1% (Mercer Insurance Group to be acquired by UFCS for 28.25 per share; transaction expected to add to United Fire earnings by 2012), EURX (halted; Eurand to be acquired by Axcan for $12/share in cash ).

Select financial related names showing strength: BBVA +6.4%, NBG +6.0%, ING +5.2%, RBS +4.7%, PUK +4.5%, AEG +4.0%, STD +4.0%, LYG +3.7%, BCS +3.2%, RF +2.4%, BAC +2.4% (trading ex dividend), RDN +2.3%, DB +2.3%, GFA +1.7%, CS +1.6%, UBS +1.5%, HBC +0.7%.

Select metals/mining stocks trading higher: SLW +4.4%, BBL +3.5%, EXK +3.4%, GGB +3.4%, SWC +3.1%, HL +2.5%, RIO +2.5%, NGD +2.3% (sold its 115 mln shares in Beadell Resources at AUD0.53 per share for total net proceeds of AUD60 mln), GDX +1.2%, GLD +0.7%.

Select oil/gas related names showing strength: LNG +5.7%, ACGY +4.6%, SDRL +4.4%, LLEN +4.1%, REP +3.6%, PUDA +3.0%, STO +2.3%, PBR +2.1%.

Select solar names trading higher: LDK +2.9%, SOLF +2.9%, JASO +2.2%, TSL +2.2%.

Other news: BIOC +14.6% (light volume; announced a strategic partnership with Kaizen Clinical Services), OPTT +8.8% (will be announcing its results for the second quarter on December 10, 2010), TTM +3.5% (traded higher overseas after India reported vehicle sales), OINK +2.7% (provided an update on its operations and provided insight regarding policies recently announced by China's State Council to stabilize pork prices), LGF +1.2% (Icahn amends tender offer for Lions Gate common shares ), PVH +1.0% (Cramer makes positive comments on MadMoney), GM +0.6% (repays additional $1.0 bln of debt).

Analyst comments: FDX +1.5% (added to U.S. Key Calls list at UBS), IGTE +1.5% (Patni acquisition rumor derails stock - selloff overdone - Signal Hill).

-

Täna on J.P. Morgani analüütikud väljas positiivse reitingumuutusega Magna International (MGA) kohta.

J.P. Morgan tõstab MGA reitingut „hoia“ pealt „ostA „ peale ja hinnasihi $53,50 pealt $66 peale.

Magna International on üks suurimaid ning mitmekesisema tootevalikuga autoosade tootjaid maailmas. Kui enamus keskendub ühele kindlale valdkonnale, MGA tootevalik on lai ning sisaldab muu hulgas autoistmeid, elektroonikaseadmeid, peegleid jne.

MGA on seotud nii General Motors (GM), Fordi (F) kui ka Chrysleriga ja sealt tuleb ka suur osa käibest vastavalt 18%, 15% ja 11%.

Investors are likely to become much more confident on European margin recovery potential in the next 3-6 months because of (1) announcement of detailed European restructuring plans by management, potentially on Q4 call or at Jan Detroit Auto Show; (2) surging auto sales in Russia partly due to extended scrappage programs (+50% y/y each month since June), a market where higher than expected revenue would clearly be welcomed given significant new MGA capacity being installed currently; (3) accelerating volumes at the Steyr vehicle assembly business (Stery production will firmly turn a corner in Q4.10, with production, as per CSM, +9% q/q and +74% in FY2011 as phased out vehicles like BMW X3 are fully replaced by new high volume vehicles like the Mini Countrymen by Q4.2010).

Analüütikud usuvad, et investorid on muutumas kindlamaks firma Euroopa marginaalide paranemise potentsiaali osas järgneva 3-6 kuu jooksul. Esiteks on oodata varsti täpsemat restruktureerimisplaani, teiseks on müük Venemaal tõusutrendis ( osaliselt küll tänu riiklikule toetusprogrammile) ja kolmandaks näitab häid tulemusi ka MGA tütarfirma Steyr.

Mitte väiksema tähtsusega pole analüütikute arvates ka firma hiljutine viide sellele, et kavatseb hakata tulevikus investoritele detailsemaid prognoose andma ja kindlasti rohkem kui nad seni seda teinud on. Analüütikud usuvad, et see võiks juhtuda juba 4. kvartali tulemuste teatamisel ning selline muutus võib olla positiive katalüsaator kuna siiani on paljud investorid firmat pigem ignoreerinud just vähese info tõttu.

Guidance release may be a catalyst. Magna recently signaled that it will be providing investors more granular financial guidance, much more than it has historically. We think this will likely occur on the Q4 call or at the Detroit Auto Show in Jan. We suspect the company will, for the first time, be prepared to provide next-year revenue and margin range, a multi-year backlog, and guidance on long-term margins (at least for Europe). While the devil will be in the details, we believe this level of transparency can only aid valuation in the long term, and it may even serve as a near-term catalyst depending on the guidance details. MGA has for years been ignored by a large swathe of the investment community for corporate governance reasons and partly also because it happens to be one of the largest and most diversified suppliers globally, yet it provided little beyond annual revenue guidance historically.

Autosektor on hetkel üks kuumemaid ning tänase tugeva turu taustal usun, et MGA call tekitab täna kindlasti ostuhuvi.

-

Gapping down

In reaction to disappointing earnings/guidance: APWR -24.5%, JOSB -9.5%.

Other news: COCO -4.6% (Board of Directors names Jack Massimino Chief Executive Officer), HCN -3.1% (announces proposed offering of 9 mln shares of common stock ), EPD -2.2% (commences a public offering of 10,500,000 common units representing limited partner interests ), STON -2.1% (filed for a $300 mln common units shelf offering; as well as a ~2.11 mln common unit offering by selling unitholders), YMI -2.0% (files for $115 mln mixed securities shelf offering), TICC -1.9% (announces pricing of public offering of common stock at $10.25), NGG -1.2% (trading ex dividend).

Analyst comments: SAFM -1.2% (downgraded to Sell from Neutral at Goldman), VIP -0.8% (downgraded to Neutral from Buy at Goldman).

-

Stay Flexible in this Ping-Pong Game

12/01/2010 8:36 AMI would rather be an opportunist and float than go to the bottom with my principles around my neck.

--Stanley Baldwin

The recent pattern that the market has established -- opening in the opposite direction of way it closed the prior day -- is continuing. After a negative day yesterday, the major indices are gapping up strongly this morning on some better-than-expected economic reports from overseas. The main driver is the China Purchasing Managers Index report, which has indicated that recent inflation-fighting efforts aren't killing that hot economy.

We have seen quite a battle lately: Concerns about European sovereign debt have kept pressure on the market, while better-than-expected economic reports have provided support. The market has been rotating back and forth each day between which issue matters the most, and today the economic data is coming out on top. However, the Europe issues are not nearly resolved, and they are going to continue to generate a headwind for the bulls.

If this gap-up open holds, the S&P 500 will be pushed back up into the upper half of the recent trading range, with the resistance at 1200 within reach. The S&P has been flirting with support around 1175 for quite a while -- and, as I have indicated, I'm concerned that if the index keeps testing that level, it will fail. That won't be an issue this morning, and we can now think more about whether the bulls have the juice to push the S&P back through 1200 and turn the trend back to the upside.

In this sort of trading-range market, in which stocks ping-pong back and forth between two obvious levels, there is often a very sharp move in which the market finally break one way or the other. Opportunistic traders want to trade with the trend, so they will move aggressively once it looks as though the major indices finally have the traction to break the range.

However, traders will often help to keep the market stuck as they short the rips and buy the dips. If you look at the intraday action over the last 10 days, you'll see that the market has tended to move back toward the middle of the trading range each day after gapping one way or the other. If that pattern holds, then the gap-up open this morning will fade.

When the market is in a trading range, as always, I try to maintain an agnostic view of the overall market. I just want to focus on finding and exploiting good trading opportunities. Of course, the media are full of people making predictions about which way the market will ultimately go; however, I find that if we focus too much on that, we miss out on the opportunities that arise each day. If you have been a dogmatic bear or bull, you have been whipsawed lately as this market has changed direction on a daily basis. If you have stayed flexible, on the other hand, each day has presented good trading opportunities.

In short, it really isn't important that you have a market bias and identify yourself either as a bear or as a bull. There is often way too much focus on that, and you miss out on a tremendous number of opportunities if you don't maintain an open mind.

I don't know in which direction the current trading range will be resolved, and I'm not worried about it. My focus is to simply be prepared to react as the battle plays out. This morning the bulls are in charge, and we'll see quickly how much resolve they have, but I'll be ready to sell them some of inventory and lock in gains if I can.

The roller coaster ride continues, so buckle up and be ready to trade

-

USA indeksite futuurid indikeerimas avanemist 1,4% plusspoolel

Euroopa turud:

Saksamaa DAX +2,15%

Prantsusmaa CAC 40 +1,30%

Suurbritannia FTSE100 +1,83%

Hispaania IBEX 35 +4,43%

Rootsi OMX 30 +2,00%

Venemaa MICEX +1,91%

Poola WIG +1,49%Aasia turud:

Jaapani Nikkei 225 +0,51%

Hong Kongi Hang Seng +1,05%

Hiina Shanghai A (kodumaine) +0,12%

Hiina Shanghai B (välismaine) -0,47%

Lõuna-Korea Kosdaq +0,82%

Austraalia S&P/ASX 200 +0,05%

Tai Set 50 +1,48%

India Sensex 30 +1,68% -

ADP tööjõutururaporti kohaselt lõid kõige rohkem töökohti väikeettevõtted. Rohkem kui 499 töötajaga ettevõtted suurendasid töökohtade arvu 2000 võrra, 50-499 töötajaga ettevõtted lisasid 37 000 uut töökohta ning väikeettevõtted lõid 54 000 töökohta. Tootmissektoris lisandus 14 000 töökohta ning teenustesektoris 79 000 töökohta. Ehitussektoris vähenes töötajate arv 3000 võrra, mis on väikseim kukkumine alates 2007. aasta juunist. Tehaste töökohtade arv suurenes 16 000 võrra.

-

Föderaalreserv peaks täna avalikustama pankade ja välismaiste keskpankade nimed, kellele väljastati finantskriisi ajal laenusid umbes $2 triljoni ulatuses.

-

The Fed purchased $8.17 bln of 2016/2017 maturities through Permanent Open Market Operations as dealers looked to put back $30.14 bln

-

NASA leidis UFOd

http://www.nasa.gov/home/hqnews/2010/nov/HQ_M10-167_Astrobiology.html -

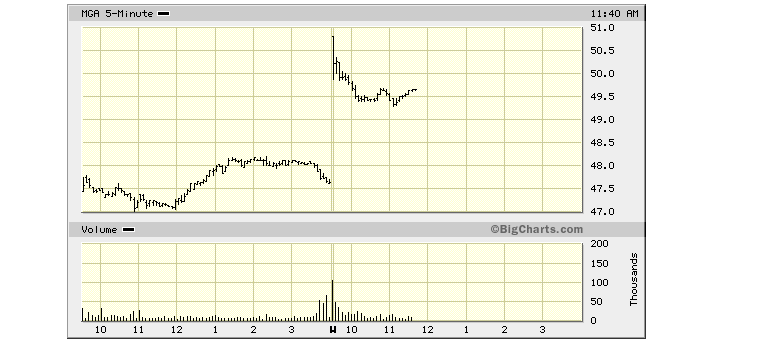

Kahjuks osutus tänane MGA call täiesti mitte kaubeldavaks. Eelturul tehti väga vähe tehinguid ja aktsia aeti liigselt üles. MGA avanes $50,80 kandis ja oli selleks hetkeks juba ca 6% plussis ehk sellelt tasemelt seda osta muidugi enam ei kannatanud.

-

U.S. WOULD BE READY TO BACK LARGER EUROPEAN FINANCIAL STABILITY FUND VIA INCREASED IMF COMMITMENTS - U.S. OFFICIAL

-

samas ka

GREECE'S NET BUDGET REVENUES UP 5 PCT Y/Y IN JAN-NOV VS ANNUAL TARGET OF 6 PCT- FINMIN SOURCE -

EURUSD igatahes 1,3% kõrgemal $1,3151 juures.

Fed avaldas nüüd ka kõik detailid oma kriisiaegsetest programmidest, materjale päris palju... -

CNBC is now reporting that the U.S. is not discussing a larger IMF contribution to EU rescue fund, according to the WSJ, who is citing a U.S. official

-

U.S. TREASURY OFFICIAL SAYS NOT DISCUSSING AN EXTRA COMMITMENT TO IMF FOR EUROPE STABILITY FUND RIGHT NOW

-

Beige Book indicates that the economy continued to improve, on balance, during the reporting period from early/mid-October to mid-November

-

Goldman Sachs raises 2011 real GDP growth to avg 2.7%, up from 2% previous est - CNBC

-

Täna avaldas USA suurim laenu tagatise katteks äravõetud (foreclosure) kinnisvaraobjektide müügile pühendunud ettevõte RealtyTrack vägagi huvitavat informatiooni riigi kinnisvarasektori kohta. Paraku tuleb taaskord tunnistada, et turu taastumisest on veel liialt vara rääkida.

Selleks, et allolevatest numbritest paremini aru saada, on tähtis välja tuua paar fakti. Nimelt moodustas kolmandas kvartalis laenu katteks äravõetud elamute müük koguni 25% elamute kogumüügist. Vaatamata sellele, et selliste elamute hinnad on ca 32% madalamad, kui samaväärsed elamud, mida ei saa seostada makseraskustega, on USA kinnisvaraturul endiselt pakkuda ca 200,000 elamut, mille omanikud ei ole tulnud toime laenu tagasimaksmisega. Kui nüüd rääkida tegelikest numbritest, siis RealTraci poolt avaldatud raporti kohaselt langes laenu katteks äravõetud elamute müük kolmandas kvartalis 2. kvartaliga võrreldes 25% ning möödunud aasta sama kvartaliga võrreldes koguni 31%. Samas on aga nõudluse vähesuse tõttu tavaliste elamute ning laenu katteks äravõetud elamute hinnavahe moodustanud viimase 5 aasta tipu.

Sellest tulenevalt on ka laenu katteks äravõetud elamute hinnad kannatanud. 2. kvartaliga võrreldes langes "foreclosure" elamute hinnad 2.46% ning möödunud aasta sama perioodiga võrreldes registreeriti 0.44%line hinnalangus.