Börsipäev 4. jaanuar

Kommentaari jätmiseks loo konto või logi sisse

-

Tänaste makronäitajate osas on tähelepanu suunatud Saksamaa töötururaportile ja ootuste kohaselt näeme töötute arvu vähenemist 15 tuhande inimese võrra, samas kui töötusmäär peaks jääma püsima 7,5% peale. Lisaks avaldatakse ka eurotsooni tarbijahinnaindeks, millelt oodatakse novembrikuu 1,9% pealt tõusu 2,0% peale detsembris.

Suurbritannias avaldatakse heakskiidetud kinnisvaralaenude andmed ja PMI tootmisindeks.

USA sessioonil ilmuvad tehaste tellimimuste andmed ja kell 21.00 avaldatakse Föderaalreservi detsembrikuu kohtumise protokollid.

Aasia turud lõpetasid valdavalt kõik plussis ning ülespoole avanemisele viitavad hetkel ka USA indeksite futuurid.

-

VIGA: Order changes are not available at the moment - autoprocess request pending.

-

LHV - kui kaua selle vea kõrvaldamine aega võtab?

-

Viga on kõrvaldatud.

-

Tänud, õnnestub jälle ordereid sisestada.

-

Saksamaa töötusmäär jäi püsima 7,5% peale, kuid töötute arv hoopis kasvas 3 tuhande võrra, kuigi oodati vähenemist 15 tuhande võrra. Euro ei ole veel tulemuste peale suuremat reaktsiooni veel näidanud, kaubeldes 0,05% madalamal $1,3350 tasemel.

-

Suurbritannia detsembrikuu PMI tootmisindeks tõusis novembrikuu 58,0 pealt 58,2 punkti peale, ületades oodatud 57,2 punkti. Aktsepteeritud kinnisvaralaenude arv näitas samuti paranemise märke, tõustes novembrikuu 47,3K pealt 48K peale, samas kui oodati näidu langemist 46,5K peale.

Naelsterling on reageerimas väga jõuliselt, kaubeldes hetkel dollari vastu 0,92% kõrgemal $1,5628 tasemel. -

Tänane New York Post kirjutab, et 2010. aastal saavutas USA tarbijate pankrotilaine taseme, mis on viimase viie aasta kõrgeim. On väga tõenäoline,et uus aasta toob selles osas lisa, sest võlakoorem on endiselt üsna kõrge.

-

Täna on J.P. Morgani analüütikud väljas positiivse reitingumuutusega Orient-Express Hotels (OEH) kohta.

JPM tõstab OEH reitingu „hoia“ pealt „osta“ peale ja hinnasihi $11 pealt $17 peale.

Our upgrade is based on the following: 1) OEH’s exposure to the luxury segment, which should outperform non-luxury and grow approximately 10% in 2011E; 2) OEH’s relative share price underperformance to peers in 2010; 3) a much improved balance sheet, given a number of balance sheet transactions and events in 2010, which make OEH less dependent on asset and residential sales to reduce its leverage ratios; and 5) a lack of positive sell-side ratings (an almost “who cares” sentiment on the sell side, in our view), which we think changes in 2011 as OEH’s operating results improve.

Analüütikud põhjendavad oma reitingumuutust järgnevalt: 1) OEH on laienemas luksussegmenti, mis võib omakorda ületada ka nö tavasegmendi ning kasvada 2011. Ca 10% 2) OEH on võrreldes konkurentidega möödunud aastal kehvemini esinenud 3) bilansileht on paranenud, mis omakorda teeb firma vähem sõltuvaks varade müügist 4) konsensus on firma suhtes peaaegu ükskõiksel seisukohal ning JPM analüütikute arvates see suhtumine käesoleval aastal muutub, kuna OEH on näitamas paremaid tulemusi.

See call jäigi eelkõige silma mulle sellega, et analüüsimajad pole firma kohta mõnda aega enam midagi positiivset öelnud. Lisaks sellele on $17 hinnasihi näol ka tegemist street high`ga ( siiani oli selleks $12). Teisest küljest on aktsia alates suvest läbi täinud ka korraliku ralli ning on võimalus,et ootused on ka juba aktsiahinda sisse arvatud. Samas, kui turg ka toetab, siis võiks aktsia täna ka kauplemisvõimaluse pakkuda.

Hetkel eelturul aktsiaga veel tehinguid tehtud pole.

-

Vahepeal on ka eurotsooni detsembrikuu tarbijahinnaindeksi esmane hinnang tulnud, mis tõusis novembrikuu 1,9% pealt 2,2% peale, ületades oodatud 2,0%. Euro kaupleb hetkel 0,33% kõrgemal $1,3405 taseme juures.

-

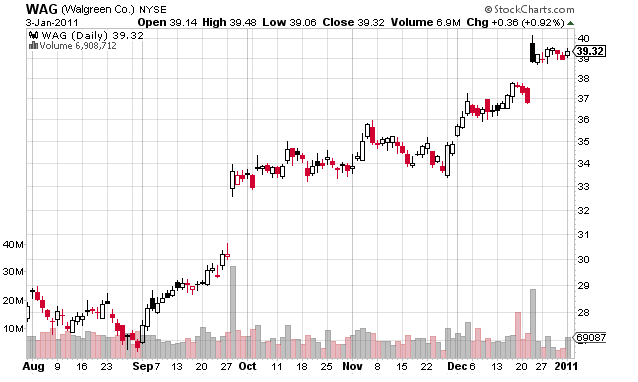

Goldman Sachsi analüütikud on täna väljas positiivse reitingumuutusega Walgreen Company (WAG) kohta.

Goldman Sachs tõstab WAG „hoia“ pealt „osta“ peale ja lisab aktsia ka oma Conviction Buy nimekirja. Uus hinnasiht on $46.

We are incrementally confident in the firm’s life cycle story, as focus on existing assets is yielding stronger margin and expense control outcomes. Moreover, sector drivers are still poised to kick in, including better front-end sales, easier flu compares, and the impact of generics on margins in 2011-12. Despite a 1Q beat and a favorable share price reaction, we do not believe WAG’s earnings outlook is reflected in Street estimates or in the stock; our forecasts are high on the Street for the Feb quarter and FY11.

Analüütikud on veendunud, et firma tõusutsükkel on nüüd algamas ja vaatamata tugevale esimesele kvartalile ning aktsiahinna positiivsele reageeringule, ei usu analüütikud, et firma kasumiteenimisvõime peegeldub konsensuse ootustes.

* The critical catalyst is likely to be earnings, notably 2Q results (3/22). * We expect improving sales trends beginning in the February quarter. The firm reports monthly sales, with December due Jan. 5. We have no edge on the month, per se, but expect improving sales over the quarter. * WAG will hold its annual shareholders meeting on January 12, and will host a meeting for analysts / investors the same day. This is not a full- scale analyst meeting, but it should help amplify those elements of the story that are working so well in our view.

Ees ootavatest katalüsaatoritest on kõige olulisem teise kvartali tulemuste teatamine ning müügitrendi tõusu ootavad analüütikud veebruari alguses.

Nii nagu Goldman Sachsi analüütikud ka ise ütlevad, siis nende prognoosid võivad valeks osutuda juhul, kui inimesed haigestuvad grippi vähem kui tavaliselt. Samas on algamas gripihooaeg ning arvestades tänavust külma talve, siis on ka mitmesugused külmetushaigused kerged tekkima. Alles mõned aastad tagasi tähendas Goldman Sachsi Conviction Buy koos upgradega aktsiahinnas vähemalt 5% rallit. Kahjuks see trend enam turul ei kehti, aga sellegipoolest usun, et aktsia võib täna mõningast ostuhuvi näha ,aga ilmselt mitte sel määral nagu vanasti. Kindlasti on selle idee toimimiseks vajalik ka turu toetus

Hetkel kaupleb WAG eelturul $39,90 tasemel, ca 1,5% plusspoolel.

-

WAG imeb, võib juba ette ära öelda.

-

to Nelli: Mis sa arvad? MetroPCS target raised to $20 from $15 at Deutsche Bank

Võib liikuda? -

Gapping up

M&A news: FSCI +19.4% (receives unsolicited proposal from Huntingdon Real Estate Investment Trust; concludes not in best interest of shareholders), BP +1.9% and RDS.A +1.0% (UK Mail report that RDS.A considered takeover and may still have interest in the company), RDS.A +0.9%.Select financial related names showing strength: ING +2.8%, DB +2.7%, HBAN +2.4%, BCS +1.9%, STD +1.8%, CS +1.6%, LYG +1.5%, RBS +1.8% (upgraded to Outperform from Neutral at Exane), PUK +1.2%, BBVA +1.1%.

Select rare earth related names trading higher: MCP + 6.3%, AVL + 6.0%, REE + 2.9%,

Select oil/gas related names showing strength: LNG +2.8%, CBEH +2.7% (announces 25% increase in petroleum contract with existing wholesale distribution customer; expected to Add $36 mln in revenue for 2011), E +1.7%, RIG +1.5%, REP +1.1%, SWN +1.0%, DO +1.0%.

Other news: VGZ +14.0% (Vista Gold announces results of a new preliminary feasibility study at the Batman Deposit; doubles estimated proven and probable reserves to 4.1 million contained gold ounces), AMRI +11.5% (announces research and licensing agreement with Genentech ), ATPG +5.2% (higher following reports out prior to close that the Dept of the Interior will allow for 10 cos to resume deepwater drilling in the Gulf of Mexico without an additional environmental review), XOMA +4.9% (light volume; hosting a conference call at 8:30am ET to provide a business update), AA +3.8% (Cramer makes positive comments on MadMoney), DRYS +3.1% (takes delivery of its first newbuilding drillship and signs two drilling contracts for the Ocean Rig Corcovado and the Leiv Eiriksson totalling $237 mln), RCL +1.6% (up in sympathy with CCL following upgrade), NFLX +1.0% (announces development effort to place Netflix-branded one-click buttons on remotes that operate Internet connected TVs, Blu-ray disc players and other devices).

Analyst comments: WAG +2.1% (upgraded to Buy from Neutral at Goldman; also added to Conviction Buy List), CCL +2.0% (upgraded to Buy from Hold at Deutsche Bank), POT +1.0% (initiated with a Outperform at Boenning & Scattergood), AMZN +1.0% (upgraded to Buy from Hold at Th Benchmark Company), MON +0.9% (upgraded to Buy from Hold at Soleil), AAPL +0.7% (added to short-term buy list at Deutsche Bank).

-

Gapping down

Select metals/mining stocks trading lower: DROOY -5.3%, URZ -3.8%, PZG -3.3%, NG -3.2%, EXK -3.0%, GRS -2.5%, HL -2.1%, SLW -1.8%, GSS -1.7%, IAG -1.7%, CDE -1.6%, GG -1.6%, AU -1.6%, AEM -1.5%, NEM -1.5%, URRE -1.4%, ABX -1.4%, MT -1.4%.Select drug names seeing early weakness: NVS -1.1%, RHHBY -0.9%.

Other news: KERX -5.0% (filed for a $100 mln common stock and warrants shelf offering), SVU -4.2% (weakness attributed to tier 1 firm downgrade), GMXR -3.4% (files $500 mln mixed securities shelf offering), NLY -2.6% (announces 75 mln share offering of common stock), TTM -1.9% (trading lower; reports out overnight that Tata Autocomp Systems is planning IPO), CRH -1.4% (still checking), CHRW -0.7% (light volume; hearing downgraded at tier 1 firm).

Analyst comments: PIP -6.3% (downgraded to Mkt Underperform at Rodman & Renshaw), ERIC -1.5% (downgraded to Neutral from Outperform at Credit Suisse), SWY -1.4% (downgraded to Market Perform from Outperform at BMO Capital), WFMI -1.3% (downgraded to Market Perform from Outperform at BMO Capital), SJM -1.1% (downgraded to Underperform from Market Perform at Bernstein), IR -0.9% (downgraded Market Perform from Outperform at Wells Fargo), MOS -0.5% (downgraded to Neutral from Buy at Gleacher), NKE -0.3% (removed from Conviction Buy List at Goldman).

-

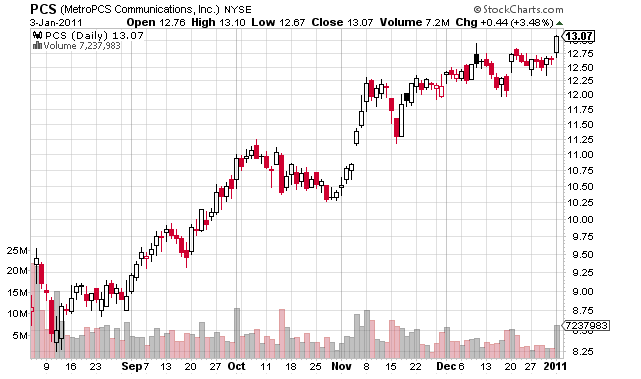

Deutsche Banki analüütikud on täna väljas positiivsete kommentaaridega MetroPCS (PCS) kohta.

Deutsche Bank kinnitab oma „osta“ soovitust aktsiale ning tõstab hinnasihti $15 pealt $20 peale, mis on ka uus street high.

Channel checks point to further share gains and ARPU stability We have 2 positive takeaways from our 4Q channel checks for MetroPCS (PCS), which covered over 80 stores across the company's 14 major markets. (1) Demand remains strong for PCS' prepaid services and we are increasing our 4Q net add estimate to 425k (consensus 393k) from 350k. (2) Rate plan mix continues to improve, which implies that our 2011 ARPU and EBITDA estimates may be conservative. We are increasing our price target from $15 to $20 (53% potential upside) and reiterating our Buy rating on the stock, which is a Top Pick for 2011.

Analüütikute turu-uuringud näitavad, et firma on jätkuvalt suurendamas turuosa ja ning nõudlus PCS ettemakstud teenuste järele on endiselt tugev. Sellest tulenevalt tõstavad analüütikud nii hinnasihti kui ka neljanda kvartali prognoose 350 tuhandelt 425 tuhandeni ( konsensus 393 tuhat). PCS on ühtlasi ka DB Top Pick 2011. aastaks.

Key findings from our 4Q10 channel checks for MetroPCS Our improved outlook is based on 3 key findings from our checks. (1) Demand is increasing for 3G and 4G smartphones despite higher price points for the devices (up to $300). (2) PCS’ strategy of advertising its $40 plan and then upselling to $45 and $50 plans continues to work (we estimate 95% of sales are at $45 or higher).

Olulisemad näitajad turu-uuringutest olid järgnevad: 1) Jätkuvalt tugev nõudlus 3G ja 4G telefonide järele, vaatamata kallimale hinnatasemele 2) PCS upselling strateegia töötab hästi ning analüütikud eeldavad, et 95% müüki toimub $45 või kõrgema hinna eest.

Kuigi tegemist pole upgradega, siis selle calli puhul on tähelepanuväärne asjaolu, et Deutsche Banki analüütikud on seda aktsiat väga hästi siiani katnud. Näiteks käesoleva aasta mais andsid nad PSC-le „osta“ reitingu koos $14 hinnasihiga. Olgu öeldud, et tookord kauples aktsia $8 kandis. Toona väga kõrgena tundunud hinnasiht on tänaseks sisuliselt realiseerunud ehk annab põhjust oletada, et Deutsche Banki analüütikud teavad, millest nad PCS puhul räägivad. Aktsia võiks täna liikuda täna $13,40-$13,50 kanti.

Hetkel kaupleb PCS eelturul $13,20 kandis, ca 1% plusspoolel

-

to daniel1: mu ülalolev postitus ilmselt vastas ka su küsimusele.

-

to Nelli: tänud.

-

Väike mõttelõng Sharkilt ka siia:

Play What's in Front of You

By Rev Shark

RealMoney.com Contributor

1/4/2011 9:11 AM EST

Better three hours too soon than a minute too late.

-- Ford, The Merry Wives of Windsor, William Shakespeare

William Shakespeare probably wouldn't have been a very good trader with that attitude. The folks who keep trying to time the top in this market have missed out on substantial gains, and it is happening again this morning.

We are kicking off the second day of the new year with yet another strong open. This market has had amazing momentum since the first of December, with the S&P 500 up 19 of 23 days; the biggest pullback during that run has been less than 0.5%. The uptrend isn't all the remarkable, but the lack of any downside during that period has been.

After today the market starts to lose its positive seasonality, but continually looking for this market to reverse has been a losing strategy. I'm getting a bit tired of writing about it, but the way to deal with this market is to not be overly anticipatory -- stay with the trend as long as you can. It would have been very easy to exit weeks ago as you awaited a top, but you would have missed out on substantial gains by doing so.

Many market players fail to understand that trying to nail an exact turning point in the market carries a heavy price. It is almost impossible to do with any degree of precision, so either you call the turn too early or you react after conditions have already started to change.

People who try to call turning points will almost always do so early. They almost always will underestimate the power of momentum, and they constantly make the mistake of thinking that the market is going to act in a manner they deem to be reasonable. The market doesn't care how logical and compelling your arguments against it may be -- it acts when it wants to act and doesn't care if you think it is ignoring important considerations.

The good news is that a disciplined momentum strategy is likely to leave you pretty well positioned when a market top finally does come. As the market becomes increasingly extended, you will find fewer good entries and you will be harvesting more and more profits. Ideally, when the eventual top does come, you will be holding a very high level of cash -- not because you are bearish, but because disciplined trading has kept you from making bad buys.

Since the bottom in March 2009, it has been extremely easy to find reasons why this market can't keep running. The economic problems we read about every day are still out there, and you would think it would matter more to the stock market ... but it hasn't. If you try to use a macroeconomic approach to this market, you've probably been on the wrong side of most of the gains for a very long time.

I'm going to continue to look for long-side action to trade and am going to do my best not to be drawn into the market-timing battle. It is tough not to believe that some sort of correction is coming soon, but I'm going to wait until I see weakness in this market before acting on it. Right now the bulls continue to party like it's 1999, and I'm going to try to enjoy it as long as possible. -

November Factory Orders +0.7% vs -0.3% Briefing.com consensus; prior revised to -0.7% from -0.9%

-

Tänaste ideede kommentaariks peab kohe alguses ütlema,et mul õnnestus neid kõiki igas mõttes alahinnata.

Üldiselt võib täna kõige paremaks ideeks pidada OEH-i. Aktsias oli võimalus positsioon soetada ca $13,40 kandist ehk 3% kõrgemalt. Kuna ma ei uskunud, et OEH nii suurejoonelise liikumise kavatseb teha, siis pidasin ise seda hinnataset juba kalliks. Kes riskis sealt aga positiooni soetada, ei pea ilmselt kahetsema, sest aktsia liikus peale avanemist sirgjoones üles, käies ära ka üle $14 taseme. Hetkel kaupleb OEH $13,80 kandis, 6% plusspoolel.

Ka PCS pakkus täna kauplejatele head kasumiteenimise võimalust. Aktsiat sai avanemisel soetada vägagi mõistliku hinnaga ehk siis ca 1,3% kõrgemalt, $13,25 kandist. Liikumasaamine võttis aktsial küll natuke aega, kuid 10 minutit peale avanemist sai hoo sisse ja on päeva peale ära käinud ka $14 all. Igal juhul sõitis PCS minu prognoosidest üle. Hetkel kaupleb PCS $13,80 kandis, 5,3% plusspoolel.

WAG-i idee kommenteerimiseks tõenäoliselt ongi kõige paslikum LHV foorumikülastaja ymeramehe kommentaar. Sain tõestust veel kord selle kohta, et Goldmani Sachsi reitingumuutuste mõju on muutunud tänaseks päevaks ikkagi üsna marginaalseks.

-

Kel on plaanis panustada Hiina turule, siis vaadaku enne kindlasti läbi Credit Suisse analüütikute poolt koostatud presentatsioon sellest, milline näeb välja Hiina 2015. aastal.

Presentatsioon ise nähtav Business Insideri veebilehel.

-

Kas keegi võib seletada või vihjet anda, miks täna kõik väärismetallide ETF on nii punased?

-

Kui papp läheb aktsiasse ära, siis kuld ja hõbe ei sära. /Häädemeeste/

-

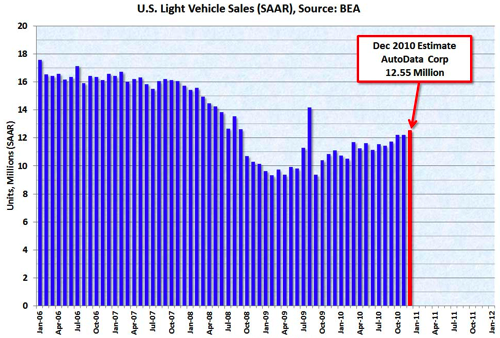

Autodata Corp sõnul müüdi möödunud aasta detsembris sesoonselt kohandatuna 12.55 miljonit kergesõidukit (sõiduautod, kaubikud, väikebussid). Ehk 2009. aasta tulemust ületati 13.1% võrra ning novembrikuu müüki ületas number 2.7% võrra. Allolev graafik näitab ajaloolist kergesõidukite müüki (SAAR) ning Autodata Corp prognoosi. Olgu öeldud, et kui prognoosid paika peavad, siis detsembris müüdi rekordarv kergesõidukeid 2008. aasta septembrist saati (kui välja arvata Cash-for-Clunkers 2009. aasta augustis).